3 Reasons Why General Electric Is No Match For Dividend King Emerson Electric

General Electric (GE) and Emerson Electric (EMR) are very similar companies. They operate in the industrial sector, and both are experiencing similar challenges right now, namely the strong U.S. dollar and weak commodity prices.

And, both stocks have attractive 3.2% dividend yields.

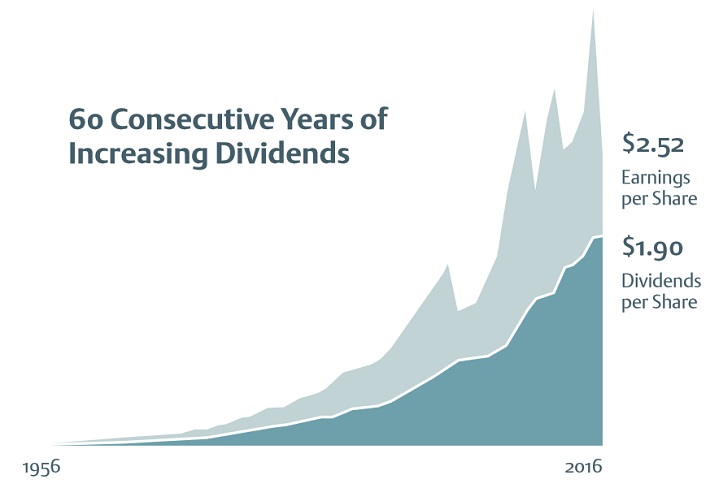

But Emerson Electric has one of the most impressive histories of raising dividends in the entire stock market. It has increased its shareholder payout for 60 years in a row.

As a result, it is a member of the Dividend Aristocrats, a group of companies in the S&P 500 that have raised dividends for 25+ years.

You can see the entire list of Dividend Aristocrats here.

Not only that, but Emerson is also on the Dividend Kings list, which includes companies with 50+ years of consecutive dividend increases.

Emerson is one of just 19 Dividend Kings. You can see the entire list of Dividend Kings here.

This article will discuss three major reasons why I prefer Emerson stock over GE.

Reason #1: Dividend History

First and foremost—dividends.

Emerson has increased its dividend each year for six decades running. Over the course of those 60 years, the company raised its dividend by 11% annually.

Source: 2016 Fact Sheet, page 2

On the other hand, General Electric has had a much more volatile dividend history.

The company cut its dividend by 68% during the financial crisis in 2009, after famously stating it would not have to.

It was GE’s first dividend cut since 1938.

While GE returned to steady dividend increases in the years following the Great Recession, its dividend growth has remained uneven.

For example, the company went two full years—from December 2014 to December 2016—without raising its dividend.

Being a member of the Dividend Kings list is highly impressive. Emerson’s track record speaks volumes about the strength and durability of its business model.

By contrast, GE’s huge dividend cut and ensuing dividend freeze do not inspire a great deal of confidence that it can ride out difficult economic periods and continue to raise its dividend.

This gives Emerson a huge advantage over GE.

Reason #2: Business Overview

The second I prefer Emerson is because of its simpler organizational structure.

This is a period of transition for both companies.

In response to global headwinds, Emerson restructured its business model last year. It divested its network power and motors and electric power businesses last year, for a total of $5.2 billion.

It used the proceeds to invest further in its industrial automation, process management, and heating and air conditioning businesses.

As a result, Emerson now operates in just two segments, which are:

- Automation Solutions (62% of revenue)

- Commercial & Residential Solutions (38% of revenue)

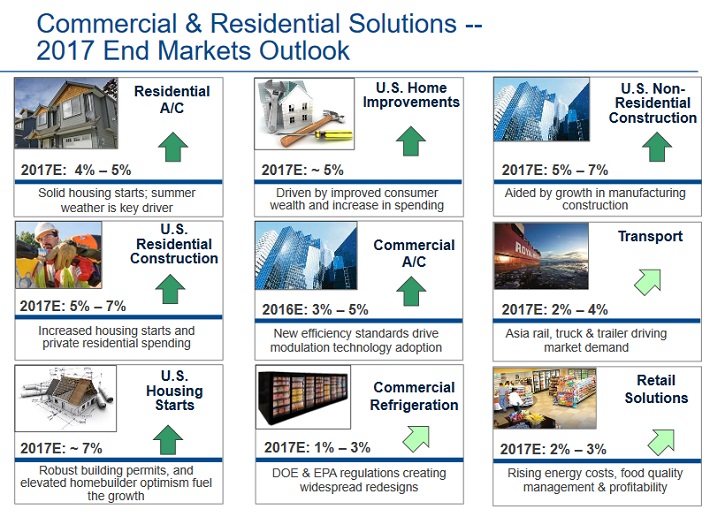

The Commercial & Residential Solutions segment has a positive outlook, as many of its end markets are still strong.

Source: 2017 Investor Conference, page 28

This helps insulate Emerson against weak commodity prices, and the strong U.S. dollar.

The very difficult industrial climate over the last two years necessitated a restructuring. The company believes the benefits of the restructuring will be significant.

Source: 2017 Investor Conference, page 14

Emerson expects to generate at least $350 million in cost savings this year. This will help fuel as much as 7% growth in earnings-per-share this year.

For its part, GE is an industrial conglomerate. Its operating segments are as follows:

- Power (24% of revenue)

- Aviation (23% of revenue)

- Healthcare (16% of revenue)

- Oil & Gas (11% of revenue)

- Renewable Energy (8% of revenue)

- Transportation (6% of revenue)

- Energy Connections & Lighting (12% of revenue)

These businesses performed well last year, by growing revenue. However, operating margins fell 100 basis points in GE’s industrial businesses in the fourth quarter.

Source: 4Q Earnings Presentation, page 5

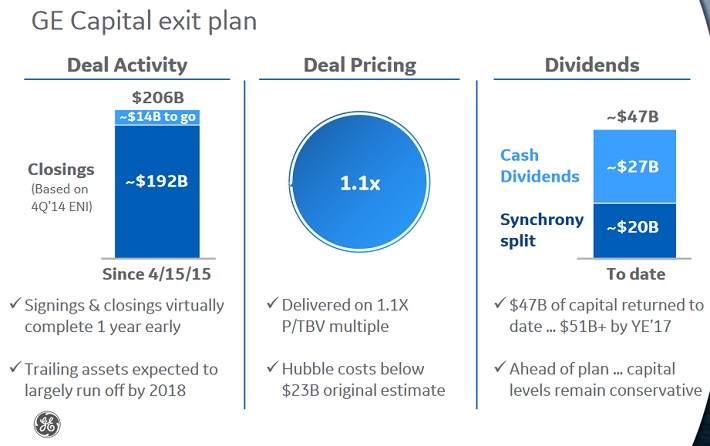

Like Emerson, GE has also restructured its business model. It is in the process of exiting its massive financial segment, GE Capital.

GE has already sealed $192 billion of deals to sell off its financial businesses.

Source: J.P. Morgan Aviation, Transportation, and Industrials Conference, page 3

It expects more progress to be made in the first half of 2017, culminating in what the company refers to as the “new GE Capital”.

According to GE, the new GE Capital will carry much less risk exposure for shareholders than the previous entity.

This is a good move, since GE Capital can be prone to volatile financial performance. For example, GE Capital lost $8 billion in 2015, and another $1.2 billion in 2016.

And, it will allow the majority of GE’s earnings to come from its traditional industrial activities.

Reason #3: Capital Returns Priorities

In both cases, GE and Emerson are likely to see earnings recover in 2017.

GE earned $1.00 per share in 2016, which was flat from the previous year. On an adjusted basis, GE’s earnings-per-share declined 12% in the fourth quarter, but increased 14% for the full year, to $1.49.

Emerson’s adjusted earnings-per-share were $2.98 in 2016, down 6% from the previous year. It expects 1%-7% earnings-per-share growth for 2017.

Their growth should give both companies room to increase dividends again in 2017.

But while Emerson is virtually guaranteed to raise its dividend again, GE is less of a sure thing.

GE often decides to utilize much more of its cash flow for share repurchases.

For example, last year GE returned $30.5 billion to shareholders, $22 billion (72%) of which was in the form of buybacks.

There is nothing wrong with share repurchases in most cases, as they can help grow earnings-per-share. But, for income investors, dividends are preferable.

This year will be more of the same.

Source: 4Q Earnings Presentation, page 5

GE expects to use $11 billion-$13 billion for share repurchases, and $8 billion for dividends.

GE has set a precedent for holding its dividend steady, if it chooses to allocate capital elsewhere. If management decides buying its stock is a better value than raising its dividend, it could choose not to raise its payout.

Emerson has always had dividends at the top of its financial framework.

It expects to return $1.5 billion to investors this year, only $250 million (17%) of which will be through share repurchases. The vast majority will be used for dividends.

And, with 60 years of consecutive annual raises on the line, Emerson is a lock to raise its dividend again in 2017.

Final Thoughts

Both GE and Emerson have above-average dividend yields, which makes them attractive for income investors.

GE is making progress in its turnaround, and is taking the right steps to reduce its risk profile.

But investors looking for a dividend stock with a longer history of uninterrupted increases, should look elsewhere. Even in the highly cyclical industrial sector, there are better options than GE—such as 3M (MMM).

Meanwhile, Emerson holds a dividend track record that is virtually unmatched in the industrial sector.

This makes it a rare find in the industrial sector, which is why Emerson is a better dividend stock to buy than GE.

Disclosure: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities.

However, the ...

more