STAG's Big Dividend: A Unique Risk Worth Considering

If you like big dividends and discounted prices, Stag Industrial (STAG) may have recently caught your eye. Its shares have fallen 12% since August 1st, and its dividend yield (paid monthly) has risen to 6.3% (annually). And despite Stag’s unique risk exposures (i.e. secondary/tertiary industrial properties that institutional investors usually avoid), we’ve ranked it #10 on our recent list of 10 Big Dividend REITs Worth Considering because of its diversified approach, reasonable valuation, continued growth opportunities, and big monthly dividend.

STAG’s Unique Investment Strategy

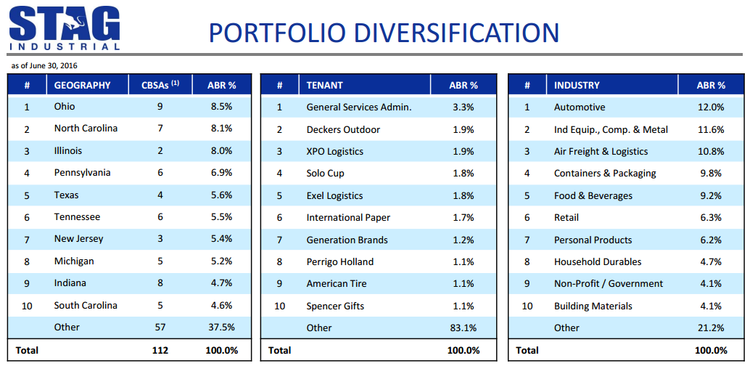

Stag focuses on the acquisition and operation of single-tenant industrial properties across the United States. As the following table shows, the company is diversified across geographies, tenants and industries.

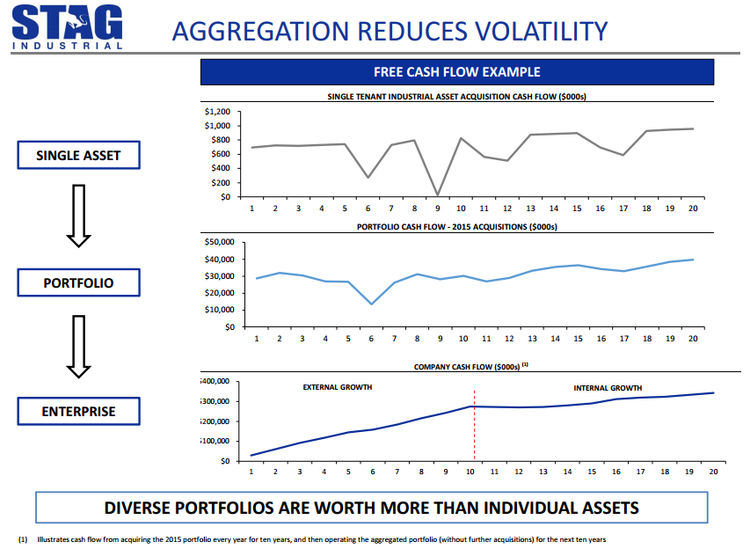

Stag is unique in the sense that it invests in properties perceived to be higher risk, but then reduces the risk through diversification. Specifically, Stag invests in single-tenant, industrial properties, located in non-primary (i.e. secondary and tertiary) locations, posing unique binary cash flow risks. However, as the following graphic shows, Stag believes it can diversify away a significant portion of the risk so as to reduce volatility and keep returns high.

We agree Stag can (and does) diversify away SOME of the risk (more on risk later), and we believe there is significant opportunity for Stag to continue to grow its funds from operations, dividend and share price.

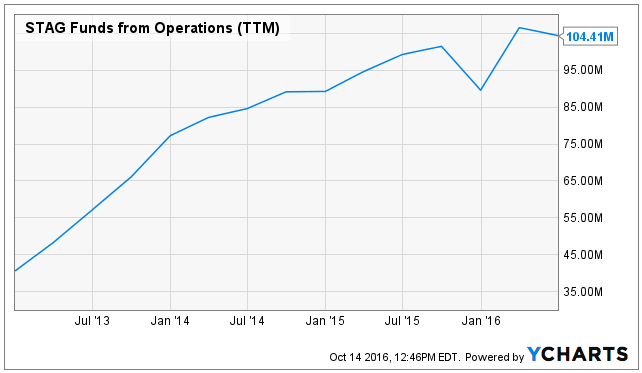

This next chart shows the trajectory of Stag’s growth in FFO (it’s impressive, in our view).

What makes it especially impressive is that there is still a lot of room for more growth. As the following graphic shows, Stag believes it is currently invested in less than 1% of its $250 billion target asset universe.

Another way to think about Stag’s uniqueness is that they bring an institutional approach to a non-institutional market. Stag is investing in a space that other institutional investors traditionally do not invest.

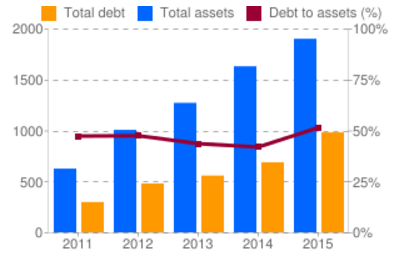

For more perspective on Stag’s growth trajectory, this next chart shows the company’s growing assets.

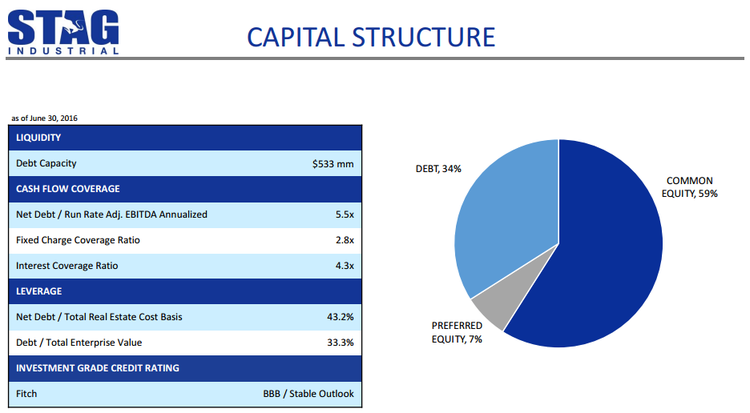

And this graphic gives perspective on Stag’s healthy capital structure and investment grade credit rating.

Stag’s Valuation

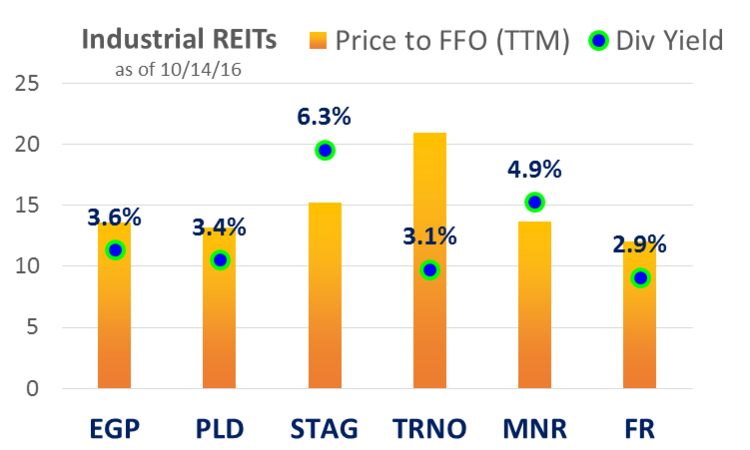

This next graphic gives some flavor for Stag’s valuation relative to peers.

And despite having a relatively big dividend, Stag’s valuation (Price to FFO) remains reasonable. Worth noting, some investors believe Stag should have a relatively cheaper valuation than some of its peers because of its unique risk exposures (e.g. secondary/tertiary properties, traditionally non-institutional markets). However, we believe the valuation is still not unreasonable.

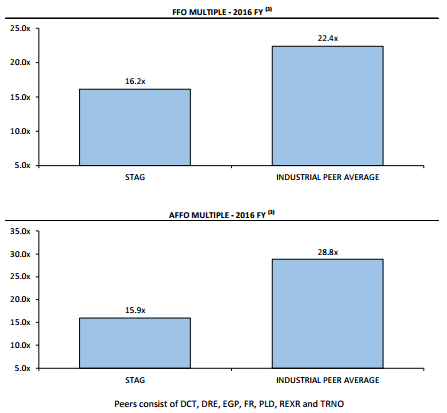

And for additional color, these next charts show Stag’s FFO multiple versus the peer universe as described by Stag’s management.

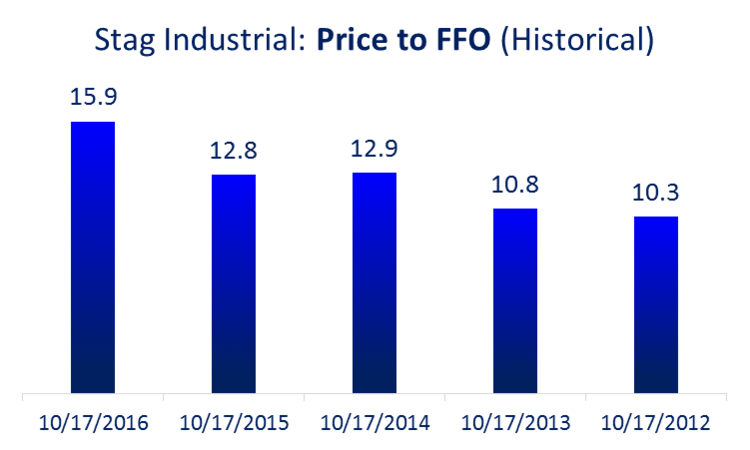

Also worth noting, the following chart shows Stag’s price-to-FFO multiple versus its own historical level.

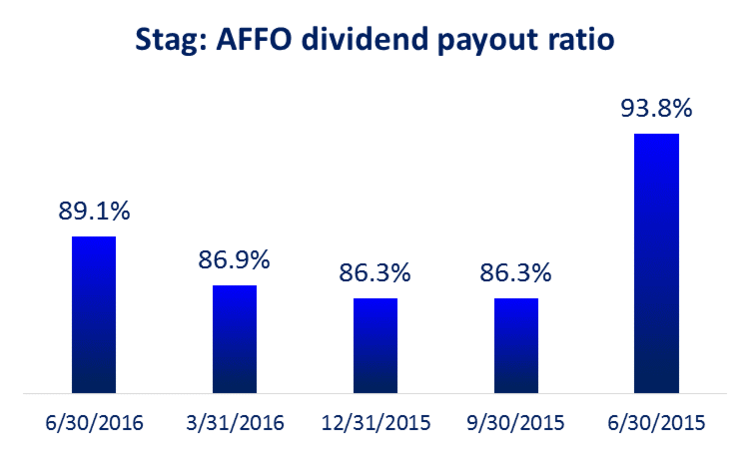

As the above chart shows, Stag is not cheap relative to its own history. However, we believe the valuation is not unreasonable considering the trajectory of its FFO growth, and its ability to pay the dividend. For example, the next chart shows Stag’s AFFO payout ratio, which remains fairly consistent, and currently has more than 10% cushion versus the 100% payout level.

For perspective, Stag’s peer Prologis (PLD) generated $0.48 of AFFO per share during the quarter ended 6/30, and it paid $0.42 in dividends, for a payout ratio of 87.5% (Prologis Q2 Supplement, p.3).

Risks

In our view, the biggest risk to Stag is an economic downturn. We believe that because the company is well diversified (as described previously) the risks posed by individual tenants is not necessarily overwhelming (because they’re well diversified across geographies, tenants and industries). Stag describes this risk in their annual report by saying:

Adverse economic conditions will harm our returns and profitability.

Our operating results may be affected by market and economic challenges and uncertainties, which may result from a continued or exacerbated general economic slowdown experienced by the nation as a whole or by the local economies where our properties may be located or our tenants may conduct business, or by the real estate industry, including the following: poor economic conditions may result in tenant defaults under leases; releasing may require concessions or reduced rental rates under the new leases due to reduced demand; adverse capital and credit market conditions may restrict our operating activities; and constricted access to credit may result in tenant defaults, non-renewals under leases or inability of potential buyers to acquire properties held for sale.

Another risk has to do with lease expiration dates. Stag describes this risk in their annual report as follows: "A significant portion of our properties have leases that expire in the next three years and we may be unable to renew leases, lease vacant space or re-lease space as leases expire."

Another risk is simply the company’s concentration in the industrial real estate sector. For example, Stag describes this risk in the most recent annual report as follows: "Our investments are concentrated in the industrial real estate sector, and we would be adversely affected by an economic downturn in that sector."

However, conditions in the industrial real estate sector are currently strong according to the SIOR Commercial Real Estate Index as shown in the following table.

In the Index, a value of 100 represents a well-balanced market for industrial and office property. Values significantly lower than 100 indicate weak market conditions; values significantly higher than 100 indicate strong market conditions. The current Industrial sub index value is 128.5, indicating strong market conditions.

Conclusion

Stag appears healthy and growing, and its big dividend appears safe. The company is exposed to unique risks in the sense that it invests in single-tenant secondary/tertiary properties that other institutional investors often avoid. However, through diversification, Stag is able to eliminate much of the idiosyncratic risk. Further, the current market outlook for industrial real estate (according to the SIOR Commerical Real Estate Index) is strong. For these reasons, we've ranked Stag #10 on our list of top 10 Big Dividend REITs (Realty Income is ranked #9, read that article here). If you are a long-term income-focused investor, we believe Stag is worth considering.

Disclosure: None.