Building A U.S. Stock Portfolio With Smart Beta Funds

Two articles in the finance press this weekend wondered if value stocks were poised to outperform. In Barron’s, Reshma Kapadia interviewed value managers and recounted how poorly value stocks have done over the past decade. Similarly, in the Wall Street Journal, Jason Zweig noted that value stocks, and the funds dedicated to picking or tracking them, should do better, but cautioned that nobody knows when that will happen. Investors seeking to profit from a value premium likely will have to have patience.

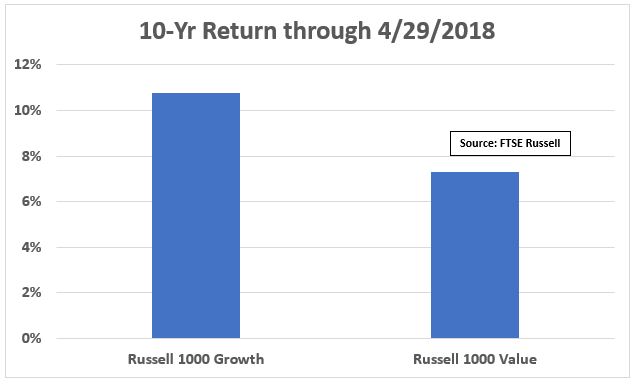

Indeed for a decade now, growth has outperformed value by more than three percentage points annualized. The Russell 1000 Growth Index has returned nearly 11%, while the Russell 1000 Value Index has returned a little more than 7%.

Ever since the publication of an academic paper in 1992 by Eugene Fama and Kenneth French proclaiming a higher expected return from stocks with value metrics, investors have increasingly assumed that value stocks would outperform growth stocks. Fama and French defined value stocks as those with low price/book value ratios, but it has increasingly encompassed stocks with low price/earnings ratios and low price/cash flow ratios. Certain sectors tend to trade with low price/book and price/earnings metrics such as energy, materials, financials, and utilities. Other sectors tend to trade with higher multiples. Those include technology and healthcare. Given the run technology stocks such as Facebook, Amazon, Netflix, and Google have had in recent years, it’s not surprising that growth has done well.

Fama and French thought value stocks returned more because they were more volatile. Risk is volatility, according to modern academic finance, and you get paid – eventually – for accepting and tolerating risk. That, of course, begs the question of whether it’s risk if you always get paid. But Fama and French might point to the last decade and say that it can sometimes take a long time.

Zweig is correct to say that nobody knows exactly when the trend will turn. However, investors have already waited a long time during which growth stocks have outperformed value stocks. It might be a decent bet to assume that if you can wait another decade, value should return to favor. In other words, it’s not necessary to call the exact turn of the trend if you’ve got a long enough time frame.

Six funds to consider for capturing a value premium are the iShares Russell 1000 Value ETF (IWD), iShares MSCI USA Equal Weighted ETF (EUSA), PowerShares FTSE RAFI US 1000 ETF (PRF), PIMCO RAE Fundamental Index Plus fund (PXTIX), iShares Edge MSCI USA Value Factor ETF (VLUE), and the DoubleLine Shiller Enhanced CAPE fund (DSEEX).

“Traditional” Value

The iShares Russell 1000 Value ETF, which tracks the Russell 1000 Value Index, is the most straightforward approach. This fund has 26% of its portfolio in financials and 9% in technology. That’s a marked difference than the iShares Russell 1000 ETF (IWB), which has 24% in technology and less than 15% in financials. And that kind of sector exposure differential is what you’d expect.

The iShares MSCI USA Equal Weighted fund is another well-known approach to capturing a value premium — or of eliminating the “noise”or high ranking of the most loved stocks associated with capitalization weighted indexing. It simply tracks an index of equally weighted stocks, lowering the weighting of the most loved and elevating the weighting of the least loved. Each stock currently occupies around 0.20% of the portfolio. This approach breaks the link between a stock’s market capitalization and its rank in the index.

Equal weighted indexing isn’t perfect though. It has capacity constraints because the 500th biggest stock in the S&P 500, for example, can only take so many dollars chasing it before its price gets pushed up too high. An approach that still captures the value premium, but doesn’t suffer from the capacity constraints of equal weighting, is the PowerShares RAFI US 1000. This fund tracks the Research Affiliates Fundamental Index, which re-ranks the stocks in the Russell 1000 by sales, book value, cash flow, and dividends.

A fourth option is the PIMCO RAE Fundamental Plus (PXTIX), which gains exposure to a modified RAFI Index through a derivative collateralized by a bond portfolio. This fund has two sources of return – the difference in the return of the bond portfolio compared to the price of the derivative and the performance of the modified index. The index is modified by the managers’ active insights to enhance returns. This fund is better suited to tax-advantaged accounts because of the use of derivatives.

Fifth, the iShares Edge MSCI USA Value Factor fund targets the cheapest stocks within each sector of its “parent” index, the MSCI USA Index. It ranks stocks against their sector peers, and chooses the cheapest ones within each sector, creating an “underlying” index that it tracks. The underlying index, therefore, maintains the sector allocation of the parent index. That means the fund avoids the typical sector overweights that one finds in other value funds. But it also means the fund won’t avoid or underweight expensive sectors. It will only own the cheapest stocks in those sectors. Indeed in the fund’s most recent Summary Prospectus, it warns that “a significant portion of the Underlying Index is represented by securities of information technology companies.”

A Value Fund That Likes Technology?

Finally, investors seeking to break the link between market capitalization and index rank and to capture a value premium should also consider the DoubleLine Shiller Enhanced CAPE Fund – especially if Zweig is correct in arguing there’s no telling when “traditional” value stocks will start to outperform again.

Like the iShares Edge MSCI USA Value Factor fund, the DoubleLine fund also approaches the world by looking at market sectors, but in a different way. It evaluates sectors of the S&P 500 Index by the Shiller PE or “CAPE” (current price relative to the past decade’s worth of real, average earnings). Each sector is judged according to its own historical valuation, and the fund consists of four of the five sectors that rank the cheapest relative to their own histories. After identifying the five cheapest sectors on a CAPE basis, the fund rejects the sector with the worst one-year price momentum among the cheapest, leaving it with exposure to four of the five cheapest sectors.

Like the PIMCO fund, this one gains exposure to stock sectors through a derivative collateralized with a bond portfolio. It also, consequently, has two sources of return.

The unique aspect of this fund is that it doesn’t tend to be consistently heavy in energy, materials, utilities, and financials, which usually enjoy significant representation in value-oriented funds. (Of course, it could be exposed to those sectors, if they were the cheapest on a CAPE basis relative to their own histories and none of them triggered the negative price momentum filter.) Surprisingly, according to its most recently published fact sheet, the fund now has exposure to the technology, healthcare, consumer staples and consumer discretionary sectors, which are often associated with better-than-average growth and profitability. This ought to give those waiting for a more traditional value rebound or those who think technology stocks are uniformly expensive pause.

Investors unable to resolve the mixed signals of traditional value sector underperformance and growth sector cheapness on a CAPE basis can pair the DoubleLine fund with one of the other value funds. This combination allows investors to break the link between market capitalization and rank of stocks in their portfolios, but doesn’t necessarily overweight traditional value sectors and stocks. It helps investors benefit from different approaches to value.