7 Attractive Equity Options For Income Investors

Income investors are frustrated with artificially low interest rates. For your consideration, we have highlighted seven opportunities to increase your income by selling options on attractive big-dividend stocks. (Note: this article is part two of our recent article titled: Cisco Covered Calls? Here Are 4 Better Options for Income Investors. The top five options recommendations are reserved for members).

Energy ETF (XLE): Writing Covered Call Options

If you are an income investor uncomfortable with energy sector volatility but still want to maintain exposure to the sector, then writing covered calls on the energy sector ETF (XLE) may be an attractive option for you. Selling XLE covered calls allows you to pick up some attractive income (from the premium) now. And as the following table shows, if the ETF gets called then you will have picked up 6.1% income in less than two months. Further, if you believe new energy extraction technologies have made cheap oil the new normal, then there is less opportunity cost risk in this strategy because energy prices are unlikely to rebound back to the very high levels last seen in the first half of 2014.

EPR Properties (EPR): Selling EPR Puts

EPR Properties is a big-dividend (4.8%) monthly-paying REIT, and we believe writing EPR put options is more attractive than writing covered calls on Cisco. EPR’s dividend is safe and growing, but the stock price has risen sharply over the last year. We’d prefer to own EPR at a lower price, and that is exactly what will happen if the shares get put to us. And if they don’t get put to us then we will have generated income by collected a healthy premium for selling the puts in the first place. For perspective, this chart shows the relatively attractive premium for selling EPR puts versus the premium for selling covered CSCO calls.

You can read our recent full write-up on EPR here:

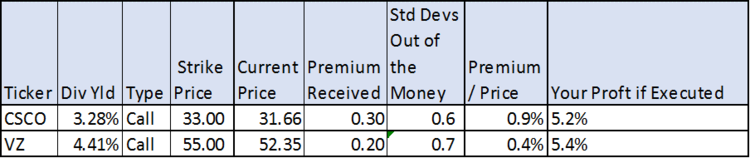

Verizon (VZ): Writing Covered Call Options

We consider Verizon covered call options more attractive than Cisco covered call options for a variety of reasons. For starters, we’d rather own Verizon instead of Cisco. Not only is Verizon’s dividend bigger (4.4% dividend yield), but its business is more stable, predictable, and less likely to deliver negative surprises. Yes, Cisco has wider margins and high returns on capital, but we believe those may shrink causing the stock to potentially lose more value than you’d make by writing the calls. And even though the premium on Verizon calls is smaller than the premium on Cisco covered calls, we believe the combination of dividend, plus call premium, plus price safety makes Verizon a more attractive covered call stock than Cisco. We like the November 18, 2016 calls with a $55 strike price because even if the shares get called you’ve still picked up 5.4% gains (premium plus price appreciation) in less than two months, and that doesn’t even included the $0.5775 dividend to be paid on November 1st.

You can read our write-up on Verizon here:

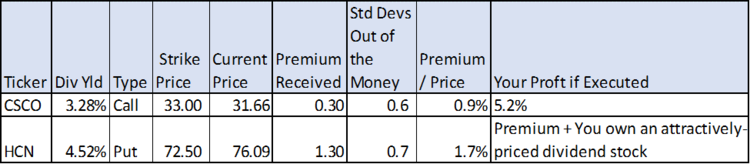

Welltower (HCN): Selling Put Options

We consider selling Welltower put options more attractive than selling Cisco call options. Selling put options gives someone else the right to sell a stock to you at a predetermined price. Welltower is a stock we’d like to own (because of the relative safety of its big dividend), but we’re not anxious to buy at the current price (it has significantly outperformed the S&P 500 on a total returns basis this year). The puts allow us to collect a premium now and it may result in us buying the stock later at a more attractive price. And not only are many put price premiums significantly larger than similarly out-of-the money call premiums, but we particularly like the November 18th, 2016 puts as shown in the following table because the put premium is nearly double the call premium for options that are a similar (but more conservative) number of standard deviations out of the money.

You can read our recent full write-up on Welltower here:

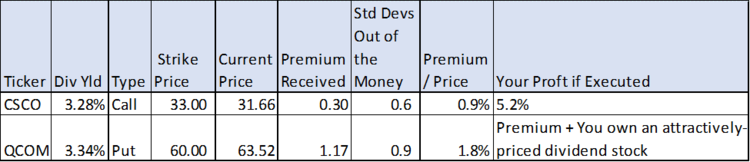

Qualcomm (QCOM): Selling Put Options

We believe selling puts on Qualcomm is a more attractive option than selling Cisco covered call options. Not only is the premium bigger (i.e. more income) but the chances of the option getting executed are lower (as measured by standard deviations out of the money), and if Qualcomm shares do get put to you then you own a better value stock with a higher-dividend, lower-volatility, and at a better price.

Plus, we’d simply rather own shares of Qualcomm than Cisco because we believe it has better long-term prospects. Specifically, we believe Qualcomm’s royalty income is safer and is more likely to grow than is Cisco’s business. Further, Qualcomm is the head-and-shoulders market share leader in wireless chips, a status that is unlikely to change for many years to come (whereas the competition is steadily chipping away at Cisco’s position). Additionally, on a price-to-earnings basis, Qualcomm is relatively attractive, as shown in the following chart.

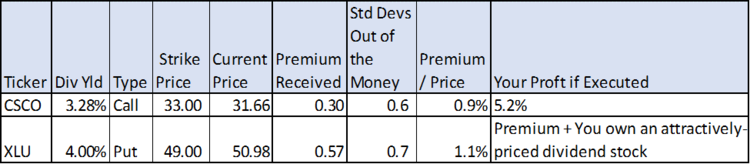

Utilities Sector (XLU): Selling Put Options

The utilities sector ETF has been on a tear this year, and now is a good time to consider selling puts on it. There is some concern that (because of the recent run) utilities are due for a pullback, and for this reason put buyers are willing to pay a healthy premium. For example, the following table shows you can collect a healthy premium for selling puts on safe boring utility stocks.

And if the shares do get put to you then you own a big dividend paying (4.0%), lower risk ETF, at a more attractive price. We consider selling XLU puts more attractive than writing CSCO calls.

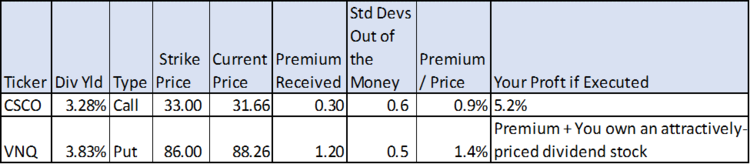

REIT ETF (VNQ): Selling Put Options

The Vanguard REIT ETF (VNQ) is an attractive way to pick up some extra income (it yields 3.8%) but we’re uncomfortable buying it after its very strong one-year rally. However, by writing puts on this ETF we can pick up some attractive income now, and we may end up owning it in the future at a more attractive price. The following table shows VNQ’s premium relative to volatility compared to CSCO covered call options, and we believe selling VNQ puts is the more attractive option for income investors

Disclosure: None.