“The market is reacting in a way which does not comport with the strength, the unbelievable strength in President Trump’s economy. I mean, everything in this economy is hitting on all cylinders because of President Trump’s economic policies. We’ve cut taxes. That’s stimulating investment in a way which will be noninflationary. That’s going to drive up productivity and wages. That’s all good.” -Peter Navarro

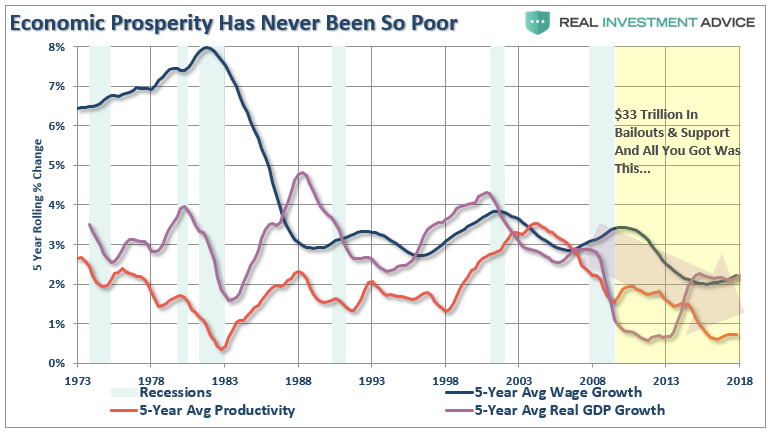

Unfortunately, as much as we would like to believe that Navarro’s comment is a reality, it simply isn’t the case. The chart below shows the 5-year average of wages, real economic growth, and productivity.

Notice that yellow shaded area on the right.As I wrote previously:

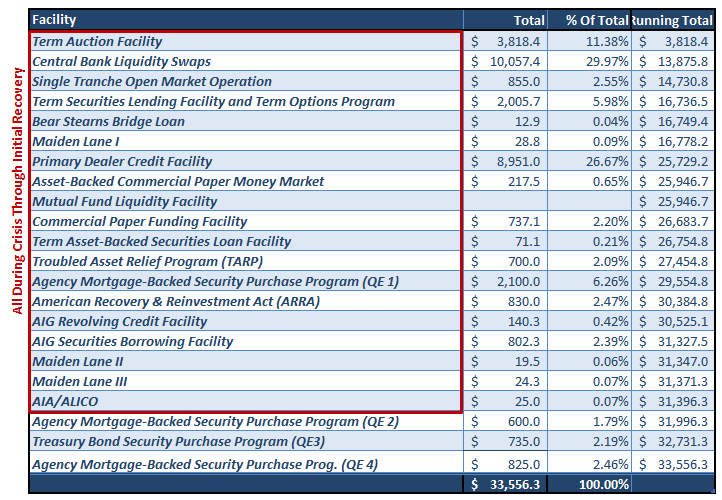

“Following the financial crisis, the Government and the Federal Reserve decided it was prudent to inject more than $33 Trillion in debt-laden injections into the economy believing such would stimulate an economic resurgence. Here is a listing of all the programs.”

If $33 trillion dollars didn’t “unleash” the U.S. economy, or even change the trends of the prior years, there should be serious doubt that just reducing some outdated regulations, giving corporations a tax cut, and engaging in a “trade war” with China is going to be the fix. But nonetheless, here goes Navarro:

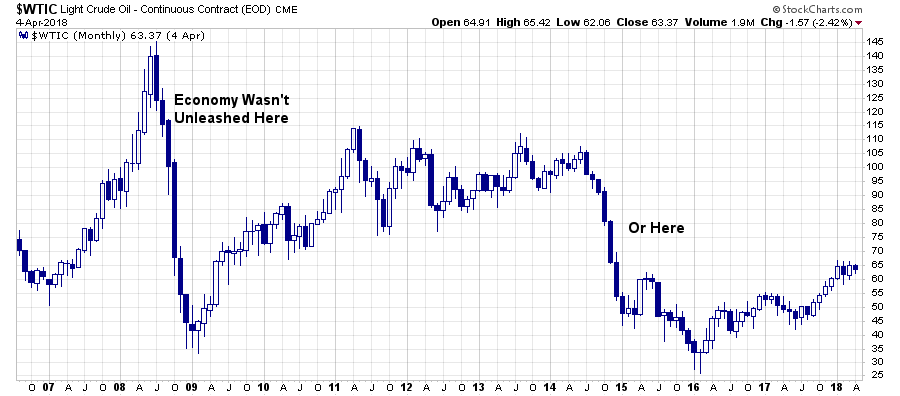

“We’ve got an unleashing, historically, of the energy sector, which is going to drive down costs to the American manufacturers–make them competitive even as it drives down costs to consumers, and allows them to spend more and get more out of their dollar.”

Wait a second.

Read carefully what Navarro said. By unleashing the energy sector the supply of oil will increase, lowering the price of oil, which is an input into manufacturing thereby lowering their costs.

This is a good thing?

Let’s dissect his statement. The decline in energy costs may be beneficial to parts of the economy, but we must remember it is offset because of the drag from the energy sector which loses revenue on each barrel of oil. As we have discussed many times previously, the energy patch is a huge CapEx contributor and also provides some of the highest wage paying jobs. As we found out previously, energy is a much bigger contributor to the health of the economy than not.

However, according to Navarro, the decline in oil alone will make manufacturing more competitive in the global marketplace. If that were true, wouldn’t the U.S. already be a leading competitive manufacturer considering oil has plunged over the last few years from over $100/bbl to the low $30’s? Furthermore, following Navarro’s logic, wages should have skyrocketed.

None of those things happened.

Navarro isn’t done yet.

“In terms of trade policy, by reducing the trade deficit, which is the intent of the president’s fair and reciprocal trade policies, that will add thousands of jobs to this economy; and bring in foreign investment. I mean, when we put the tariffs on solar and washing machines in January, that brought in a flood of new investment.”

We do indeed have a trade deficit because there are 300+ million American’s demanding cheaper foreign goods and services than there are foreigners demanding our exports.

While people rail about the amount of goods that we import, the simple reality is that we “export” our deflation and import “deflation". We do this so we can buy flat screen televisions for $299 versus $2999 if they were made in America. The simple problem is that American workers demand higher wages, vacation, health care, benefits, leave, etc. all of which increase the costs of goods made in America. Not to mention the additional costs born by goods and services producers to comply with the myriad of regulations from EPA to OSHA. A previous interview of Greg Hayes, CEO of Carrier Industries, made this point very clearly.

“So what’s good about Mexico? We have a very talented workforce in Mexico. Wages are obviously significantly lower. About 80% lower on average. But absenteeism runs about 1%. Turnover runs about 2%. Very, very dedicated workforce.

Which is much higher versus America.And I think that’s just part of these — the jobs, again, are not jobs on an assembly line that people really find all that attractive over the long term.“

This leads to the “American Conundrum.” While we believe our “labor” is worth “MORE” than anywhere else in the world, we also want to “buy” cheap products.

In order for that equation to work companies must “export” our “inflation.” This is accomplished by off-shoring labor at substantially lower rates which allows products and services to be provided more cheaply (deflation) to fill American demand. As I wrote yesterday, there is little ability for Americans to absorb the higher costs of goods and services brought about through “tariffs” or other inflationary goals of “balancing trade.”

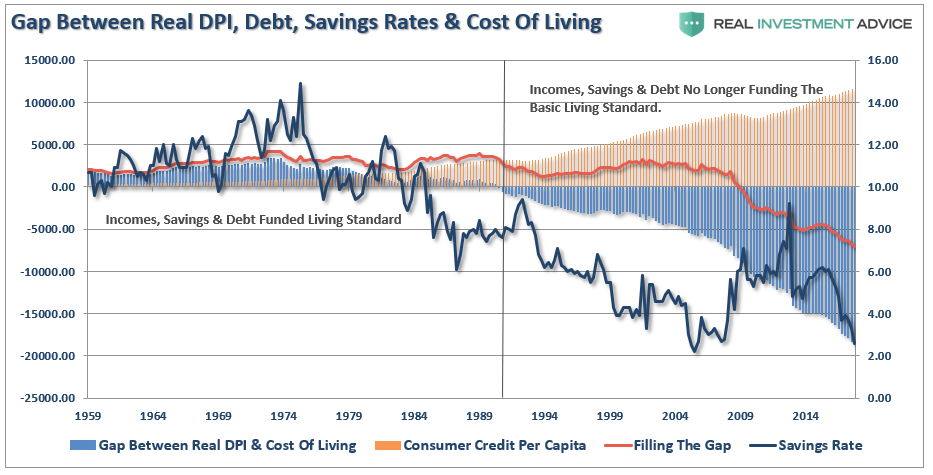

“The chart below shows is the differential between the standard of living for a family of four adjusted for inflation over time. Beginning in 1990, the combined sources of savings, credit, and incomes were no longer sufficient to fund the widening gap between the sources of money and the cost of living. With surging health care, rent, food, and energy costs, that gap has continued to widen to an unsustainable level which will continue to impede economic rates of growth.”

Of course, while Navarro is optimistic that Trump policies will generate a net creation of a few thousand jobs, such aspirations will fall far short of what is needed to balance the economy.

But honestly, you can’t make up his last statement.

So you wonder–and if I put my old hat on as a financial market analyst, I’m looking at that – this market and the economy and thinking, the smart money will buy on the dips here because the economy is as strong as an ox.”

One chart dispels that notion.

So, be careful taking financial advice from Peter Navarro as well.

But, let me defer to my friend Doug Kass:

“To me, the views that animate Navarro’s policy prescriptions demonstrate his economic illiteracy.

There is no inverse relationship between imports and GDP as Navarro asserts.

In fact, there is a strong positive relationship between changes in trade deficits and changes in GDP.

Both Navarro and Ross are proponents of steel tariffs. As I have mentioned, such tariffs hurt producers that utilize steel products much more than they benefit a smaller population of steel producers. The byproduct of which could be rising steel costs which may ripple throughout the economy.

In reality, the US depends on China – we are in a flat, networked and interconnected global economy:

- The Chinese export market is important to the U.S.

- China produces low cost goods that benefit American consumers.

- China funds our budget deficit, their surplus of savings is imported to the US – squaring the circle. If China stops buying our Treasuries, where do we get funding?“

Misguided Policies Continue

For the last 30 years, each Administration, along with the Federal Reserve, have continued to operate under Keynesian monetary and fiscal policies believing the model works. The reality, however, has been that most of the aggregate growth in the economy has been financed by deficit spending, credit expansion and a reduction in savings. In turn, this reduced productive investment in the economy and the output of the economy slowed. As the economy slowed and wages fell the consumer was forced to take on more leverage which also decreased savings. As a result of the increased leverage more of their income was needed to service the debt.

Secondly, most of the government spending programs redistribute income from workers to the unemployed. This, Keynesians argue, increases the welfare of many hurt by the recession. What their models ignore, however, is the reduced productivity that follows a shift of resources toward redistribution and away from productive investment.

All of these issues have weighed on the overall prosperity of the economy and it citizens. What is most telling is the inability for people like Navarro, and many others, who create monetary and fiscal policies, to realize the problem of trying to “cure a debt problem with more debt.”

This is why the policies that have been enacted previously have all failed, be it “cash for clunkers” to “Quantitative Easing”, because each intervention either dragged future consumption forward or stimulated asset markets. Dragging future consumption forward leaves a “void” in the future that has to be continually filled, and creating an artificial wealth effect decreases savings which could, and should have been, used for productive investment.

The Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the end result, has been clearly wrong. It hasn’t happened in 30 years.

The Keynesian model died in 1980. It’s time for those driving both monetary and fiscal policy to wake up and smell the burning of the dollar and glance at the massive pile of debts that have accumulated.

We are at war with ourselves, not China, and the games being played out by Washington to maintain the status quo is slowing creating the next crisis that won’t be fixed with another monetary bailout.

Comments

Log in or sign up to join the conversation.