Will The World Gold Council Receive The Nobel Prize In Economics?

Demand for gold declined 7 percent in Q1 2018 while gold supply increased. But the price did not fall. What does it all mean for the gold market?

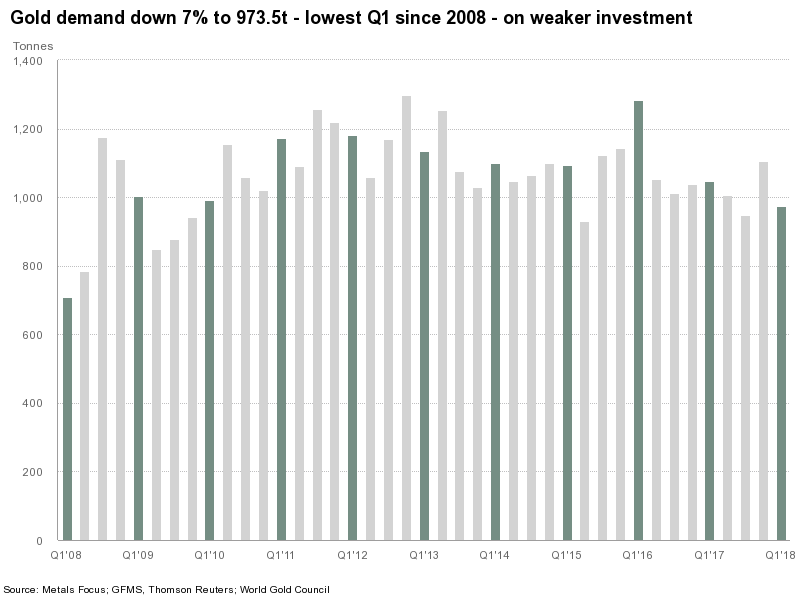

Gold Demand Dwindles in Q1 2018

We are always ahead of other analysts. Last week, the World Gold Council released a new edition of its quarterly report on gold demand. At the same time, we published a summary of the developments in the gold market in the first four months of 2018. But let’s analyze the WGC report.

The crucial finding is that gold demand plunged 12 percent from 1,105.9 tons in the preceding quarter to 973.5 tons in the first quarter of 2018. Compared to Q1 2017, the demand for gold dropped 7 percent, the lowest Q1 since 2008, as one can see in the chart below.

Chart 1: Gold demand over the last ten years (source: WGC).

The decline was mainly caused by a fall in investment demand. Indeed, ETF inflows of 32.4 tons were down 66 percent from Q1 2017. It shouldn’t be surprising given that Q1 2018 was a period of relatively stable gold prices and rising interest rates, while the beginning of 2017 was a time when negative German yields reached a record low.

However, the inflows into gold ETFs gathered some pace compared with the second half of 2017 (13.2 tons in Q3 and 28.9 tons in Q4). It indicates that the geopolitical concerns and the sudden return of volatility to global financial markets encouraged U.S. investors to seek refuge in gold. But investors should be aware that the recent tensions between U.S. and Iran failed to boost the price of gold.

WCG’s Flawed Analysis

You can learn some interesting things from the WGC report. There is no doubt about it. You can find out that global jewelry demand was roughly flat, central bank demand surged 42 percent year-over-year, and technology demand continued to improve (thanks to the increased use of gold in electronics). Fair enough. But the whole analysis is fundamentally flawed. Why? Well, the fatal error is that the WGC treats gold as commodity. It meticulously calculates the quarterly demand and supply, to determine the “balance” and to predict the future price movements.

But the problem is that, as we showed in May, gold behaves like a currency rather than a commodity. Commodities are produced and then they disappear in the process of consumption. Gold does not disappear, it is accumulated. Just look at the numbers: there is more than 180,000 tons of gold above ground. Meanwhile, the annual mining output of bullion is only about 3,300 tons. So it should be clear that the changes in the annual supply – and how it is used – have limited impact on the price of gold.

If you don’t believe us, just analyze WGC’s own numbers. Gold demand fell 7 percent, while the supply increased 3 percent. But the price of gold increased 9 percent, according to the “global authority on gold.” Incredible! The demand decreased and the supply rose – and the price also jumped! The law of demand and supply has to be reformulated! A Nobel Prize in Economics guaranteed.

Implications for Gold

Another weakness of the WGC report is that it does not pay enough attention to true drivers of gold – such as the U.S. dollar or real interest rates – and it does not draw conclusions for the future of the gold market. We do. The significant implication is that if the old relationship comes back again – and it seems that it’s happening right now – the price of gold may go south.

If you enjoyed the above analysis and would you like to know more about the most important macroeconomic factors influencing the U.S. dollar value and the price of gold, we invite you to read the ...

more