High Yield Bond Index Stumbles At Its Peak

ZeroHedge reports, “There were numerous interesting, informative and mostly bearish speakers during the latest Strategic Investment Conference held at the end of May. Among them were Lacy Hunt, David Rosenberg, Neil Howe, Jim Grant, Mark Yusko, Gary Shilling, andJohn Mauldin (readers can watch video interviews with these speakers on Mauldin Economics’ Youtube channel and their full presentations can be found at the following page) all of whom painted a very pessimistic picture for the stock market but, as Tony Sagami points out, the most alarming comment came from Richard Fisher.

… Fisher’s most telling comment came during the Q&A session when he was asked how his personal portfolio was positioned. Fisher’s response: “In the fetal position.” Moreover, he also said that “all my very rich friends are hoarding cash.”

What position are you in???

VIX rallied off the final low of a Broadening Bottom formation that is marked by successive higher highs and lower lows. Aggressive traders often use a close above the mean value of this index to begin placing bearish trades in equities.. A daily close above the prior high at 17.65 confirms the VIX buy/Equities sell signal. The Cycle low came on Tuesday. Broadening formations (tops and bottoms) are often known as reversal patterns.

(ZeroHedge) Americans' confidence in the U.S. economy averaged -14 in May according to Gallup, equaling the lowest in two years and considerably lower than the -7 print a year ago...

In May, the current conditions score registered -5, one point higher than in April. This was the result of 25% of U.S. adults rating the current economy as "excellent" or "good," and 30% rating it as "poor." Meanwhile, the economic outlook score went down one point to -22. This was the result of 37% of U.S. adults saying the economy was "getting better" and 59% saying it was "getting worse."

SPX probes higher, but closes beneath round number resistance

SPX was finally able to make a new 2016 high, but closed beneath last week’s closing level. Round number resistance at 2100.00 appears to be playing a big role in the SPX advance. While no major support has been violated, this week’s activity indicates the probability of weakness ahead. The critical Pivot day appears to have occurred on Thursday, a week later than indicated in previous reports

(WSJ) U.S. stocks fell for a second straight session Friday, with the S&P 500 index erasing its gains for the week.

The steep drop in bond yields around the world continued to trigger moves across markets. Yields on government debt in Germany, Japan and the U.K. hit all-time lows Friday, boosting the allure of investments with better returns such as U.S. Treasurys and stocks that pay out high dividends.

NDX closes lower

NDX consolidated this week, unable to advance higher. The NDX Pivot high may have also came in on Thursday. Should the NDX turn down without advancing to a higher level, the Head and Shoulders formation may be in play once NDX declines through its mid-Cycle support at 4248.65.

(ZeroHedge) The fund flow paradox continues: US stocks trade just shy of all time highs as global outflows from equity funds continue with another $2.6 billion yanked in the past week; this represents 10 weekly outflows in the past 12 weeks. More confusing is that just in the US, $2 billion was withdrawn leading to outflows in 5 of the past 6 weeks.

So who is buying?

High Yield Bond Index stumbles at its peak

The High Yield Index peaked late Wednesday afternoon at 157.20. Note that it reacts to the same pivots as equities, making its high on the same day as the SPX. Investors should be on the alert for a decline beneath its Cycle Top support/resistance at 152.50 for a probable sell signal.

(ZeroHedge) As a reminder, according to the latest BEA revision, nominal Q1 GDP was $18.23 trillion, an increase of just $65 billion from the previous quarter or an annualized 0.7% rate, the question is how much credit had to be created to generate this growth. Well, according to the Z.1, total credit rose to a new record high $64.1 trillion. This was an increase of $645 billion from the previous quarter. It means that in the first quarter, it "cost" $10 in new debt to generate just $1 in new economic growth!

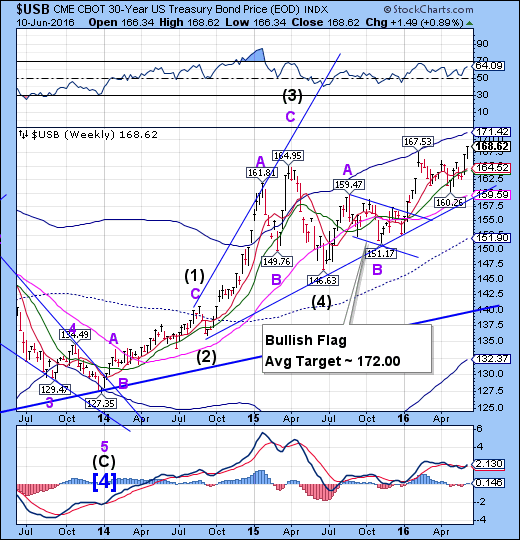

USB at all-time highs

The Long Bond closed at an all-time high this week. Its minimum target appears to be its Cycle Top resistance currently at 171.42, but the Bullish Flag target is still anticipated. The rally is leaving Bond Bears Bewildered..

(ZeroHedge) After yesterday's barnburner of a 10Y reopening auction, the only cloud on the horizon for today's 30Y reopening auction of Cusip RS9 was that the paper had traded non-special in repo; in fact according to SMRA it was a stable 0.35%.

And, again, like yesterday all concerns about potential auction weakness promptly melted away when the resulted printed just after 1pm Eastern, when the High Yield was revealed at 2.475%, stopping through the When Issued by 0.7 bps (the May auction tailed by 0.8 bps), and the lowest 30Y auction yield since January 2015, which was just 0.5bps lower.

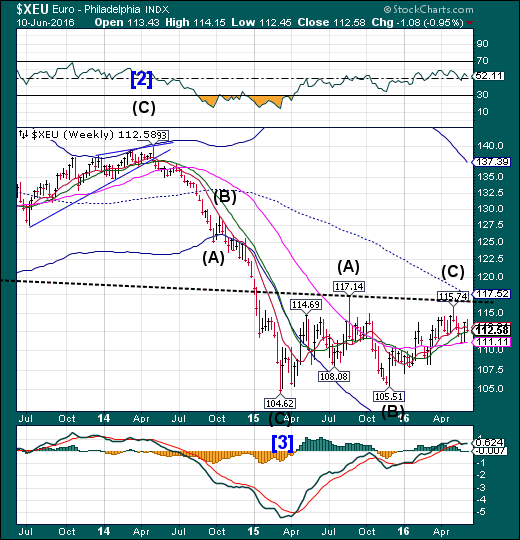

The Euro declines to Intermediate-term support

After rallying until Wednesday, the Euro declined to Intermediate-term support at 112.39. The reversal, although early, coordinated with the turn of several asset classes. A continued decline beneath support puts the euro back into a bear market.

(ZeroHedge) A few days after the ECB unexpectedly announced its CSPP, or corporate bond buying program which based on its definition was limited to investment grade, non-financial debt, we explained "Why The ECB Will Be Forced To Buy Junk Bonds", saying that "the reasons to believe Draghi will take the plunge into non-IG corporate credit go beyond the “MOAR is always better” line. As BofAML’s Barnaby Martin explains, the EU corporate sector’s penchant for bond buybacks may ultimately force Draghi further down the ratings ladder lest the ECB should end up entangled tender offers or else end up without enough debt to monetize."

This was confirmed on the very first day of the ECB's bond purchases.

EuroStoxx plunges beneath support

The EuroStoxx 50 Index declined beneath Intermediate-term support at 2993.50, reinstating the sell signal. A significant low may be due by the end of June. A massive Head & Shoulders formation may become active should EuroStoxx decline beneath the neckline at 2630.00.

(Bloomberg) The campaign for Britain to leave the European Union took a 10 percentage-point lead in a poll published late Friday, less than two weeks before the country votes in a referendum.

The survey of 2,000 people by ORB for the Independent newspaper found 55 percent in favor of a so-called Brexit, up 4 points since a previous poll in April, with 45 percent for “Remain,” down 4 points. It’s the biggest “Leave” lead recorded by ORB in polls for the newspaper.

The pound slumped after the poll as doubt creeps into some investors minds that Prime Minister David Cameron will be able to pull off the biggest political gamble in recent British history. While pollsters have cautioned against over-interpreting their findings and another survey this week showed “Remain" in the lead, Cameron himself is showing signs of unease.

The Yen consolidates near its high

The Yen consolidated this week without giving any directional signals. There are indications of cyclical strength lasting another week before a probable correction. The inverted Cup with Handle formation appears to be activated. While the Cup-with-Handle target may seem farfetched, the Cycle Top at 99.51 may be attainable as a minimum target.

(Bloomberg) The yen advanced with the Swiss franc as investors opted for their relative safety as they brace for events next week and discount chances the Federal Reserve will increase interest rates in coming months.

Japan’s currency performed best against the dollar among major currencies, followed by the Swissie. The odds that the Fed raises rates when it meets next week fell to zero after jobs data was released June 3. The report showed the fewest number of workers joined the labor force last month since 2010, undercutting interest in holding assets in dollars.

The Nikkei (barely) holds on to support

The Nikkei continued its decline this week, but was able to close just above its Intermediate-term support at 16596.02. A decline beneath Intermediate-term support may soon develop into a panic as the next support may be the Head & Shoulders neckline near 15000.00, followed by the Cycle Bottom at 13828.28.

(Bloomberg) Stocks in Tokyo fell as commodity producers dropped after oil declined, while investors awaited central bank meetings from the U.S. and Japan next week.

Japanese shares started the week on poor footing following last Friday’s disappointing U.S. jobs report. A mid-week recovery as oil rallied above $50 per barrel didn’t last, as uncertainty took hold ahead of next week’s monetary policy meetings of the Bank of Japan and Federal Reserve.

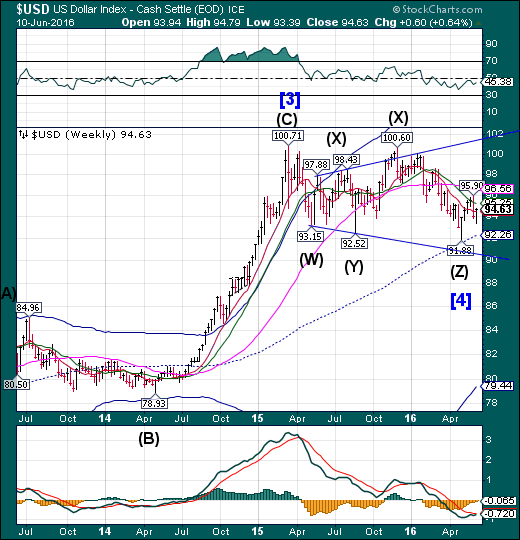

U.S. Dollar bounces to Short-term resistance

USD declined until Wednesday, then made a partial retracement to regain Short-term support at 94.50. What may follow is a decline to retest the mid-Cycle low and possibly the lower trendline near 90.50. The Cycles Model suggests the final low to occur in early July.

(Reuters) Speculators favored the U.S. dollar for a third straight week, with net longs rising to their highest in four months, according to Reuters calculations and data from the Commodity Futures Trading Commission released on Friday.

The value of the dollar's net long position rose to $11.30 billion in the week ended June 7, from $4.86 billion the previous week.

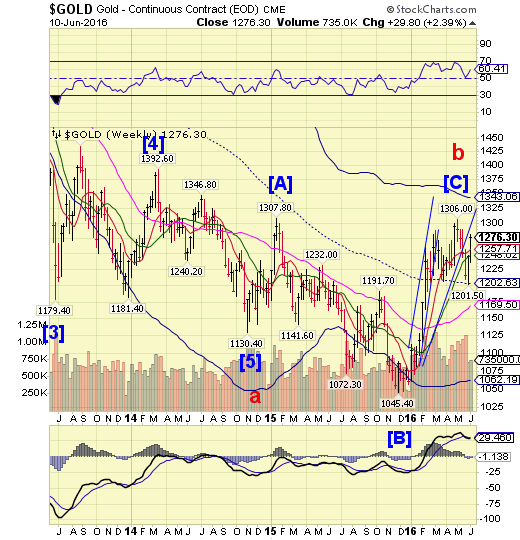

Gold makes a run for the high

Gold continued its rally, as indicated last week, making a 76% retracement. However, the rally is due for a pullback, which may determine whether the uptrend can be sustained. A decline beneath Intermediate-term support at 1248.02 may set a further decline into motion.

(WSJ) Gold prices rose Friday as bets against an imminent interest-rate increase and low bond yields around the world sent investors into the safe-haven metal.

Gold for August delivery settled up 0.3% at $1,275.90 a troy ounce on the Comex division of the New York Mercantile Exchange, marking its third-consecutive day of gains.

With government-bond yields in Germany, Japan and the U.K. tumbling to record lows this week, gold has gained ground as an safe store of value amid economic uncertainty, according to Ira Epstein, a strategist with the Linn Group. “That is scaring the living heck out of people,” he said.

Crude declines to the Pennant trendline, unchanged for the week

Crude rallied to 51.62 on Wednesday, a high not seen since the week of July 8, 2015 on Thursday. Today it abruptly pulled back to the Bearish Pennant trendline. A decline beneath the Ending Diagonal trendline at 47.50 may trigger a sharp decline in crude.

(ZeroHedge) Following last week's unexpected rise in US oil rigs - and the biggest increase in US Crude production since the first week of January – the lagged price of oil suggested that rig counts would continue to rise this week, and it did - up 3 to 328. Oil prices had dropped from over $51.50 to almost $49 - erasing the post-payrolls gains- ahead of the rig count data and were relatively unimpressed by the print.

Shanghai Index closes above Short-term resistance

The Shanghai Index closed above Short-term resistance at 2914.27, resuming its sideways consolidation. The Cycles Model suggests that the period of strength in the Shanghai Index may be about to end. The Model suggests a possible three week decline to new lows.

(OfTwoMinds) This decline is inevitable in fast-expanding economies that depended on export growth and investment booms.

The fundamental context of China's economy is that it has traced out an S-Curve--as did previous fast-developing nations such as Japan and South Korea.

Gordon Long and I discuss why there's no easy fix to the S-Curve in our new video discussion Bull in the China Shop (35:25).

The Banking Index breaks Long-term Support

BKX declined beneath Long-term support at 68.83, but not beneath the Pennant trendline. This puts BKX on an aggressive sell signal. There may be a brief bounce next week. Once the trendline broken, the Cycle Bottom support at 62.71 may not be capable of providing the next bounce.

(ZeroHedge) In early February, in a post titled "A Wounded Deutsche Bank Lashes Out At Central Bankers: Stop Easing, You Are Crushing Us", we showed just how vast the feud between Europe's biggest - and ever more troubled commercial bank - and the ECB had become. As DB's Parag Thatte lamented then, "ECB rhetoric suggests additional easing measures forthcoming in March. While a fundamental tenet of these measures, in particular negative rates, has been to push investors out the risk spectrum, we remind that arguably the impact has been exactly the opposite." And while the DB analyst has been correct, and now NIRP is widely accepted as a major mistake, the ECB proceeded to not only ease even more just one month after this first DB lament, but in what may have been a direct affront to DB, launched the monetization of corporate bonds, something which as we documented earlier today has now led to the complete disconnect between bonds and underlying fundamentals.

It was also led to daily record low yields for government bonds around the globe.

Last but not least, it has pushed the stock price of Deutsche Bank to levels not seen since the financial crisis as DB suddenly finds itself unable to make money in an NIRP environment.

(ZeroHedge) From Deutsche Bank to Credit Suisse and from Barclays to Banco Popolare, the European banking system is getting battered this week with today's plunge the biggest in 4 months...

This is the worst two week drop in European banks since April 2012...

(ZeroHedge) The last five years have been a bumper period for banking scams and scandals in crisis-ridden Spain. From Bankia’s doomed IPO in 2012 to the “misselling” of complex preferentes shares to “unsophisticated” retail bank customers, including children and Alzheimers sufferers, all of the scandals have had one thing in common: the banks have consistently and ruthlessly sacrificed the welfare and wealth of customers, investors, and taxpayers on the altar of short-term survival.

(WSJ) Acknowledging a problem is usually half the solution. For China’s banks, that is where more problems begin.

China’s banking regulator is forcing banks to fess up—and account for—the worst type of credit products buried on- and off-balance sheets under a regulation known as Document 82, released in May. While that is an admirable effort, because the problem has grown so large, regulators may now have to enforce a limp version of the rules. In its current form, Document 82 could leave banks with a more than 1 trillion yuan ($152.4 billion) capital hole.

(BBCNews) Investment in the eurozone remains far below pre-crisis levels, partly due to problems in the banks, the Organisation for Economic Co-operation and Development (OECD) has said.

Bad debts at the banks are making them less willing to lend.

The OECD says many legacies of the area's financial crisis are unresolved and major new problems have emerged.

Nothing in this email or article should be ...

more