VIX Tests Two-Year Trendline

VIX challenged mid-Cycle resistance at 13.90 again before making a new Master Cycle low Wednesday. The low tested the two-year trendline for the VIX, which stayed beneath it the entire time until the VIX shorts were wiped out on February 5. Since then it has found support at the trendline, with the brief exception of the May Options Expiration.

The NYSE Hi-Lo Index closed beneath the mid-Cycle support/resistance at 64.29, putting it on a sell signal. The Cycles Model suggests the potential for a significant low near mid-June.

(ZeroHedge) Goldman's equity trading desk can thank the early February "volocaust" for its surprisingly lucrative Q1 performance, according to CNBC.

The investment bank reaped a $200 million profit on Feb. 5, the day volatility exploded back to life in equity markets as the Dow registered its largest one-day point drop in history. The bank's score can be attributed to long-vol positions that had recently been put on by the flow derivatives group, a group within Goldman's equity desk responsible for trading VIX derivatives. The $200 million in profits is roughly equivalent to what Goldman's derivatives desk takes home for the entire year. For all of 2017, the trading business for the entire bank exceeded $100 million in revenue on just four days.

SPX was repelled by the 2-year trendline Tuesday in what is being identified as a breakout of a Triangle formation. However, if it had been a Triangle formation, there would have been a breakout on rising volume. Instead, it reversed back under trendline, lending itself to a more likely 76% retracement back to the trendline. A break of the 50-day Moving Average at 2675.00 may give the SPX a sell signal with a final confirmation at the lower trendline of the Broadening Wedge.

(Reuters) - The S&P 500 erased losses to trade little changed on Wednesday after minutes from the last Federal Reserve meeting suggested higher inflation may not result in faster interest rate hikes.

Most Fed policymakers thought it likely another interest rate increase would be warranted “soon” if the U.S. economic outlook remains intact, and that many participants saw little evidence of general overheating of the labor market, minutes of the central bank’s last policy meeting showed.

NDX managed to stay above tis 2-year trendline, but could not overcome a third Master Cycle high made on May 14. The Cycles Model called for a Master Cycle High on that date and so far it held in the NDX, while being prolonged in the SPX, the Dow and the Russell 2000 A break of the trendline puts NDX back on an aggressive sell signal. A close beneath the 50-day Moving Average at 6742.00 confirms it.

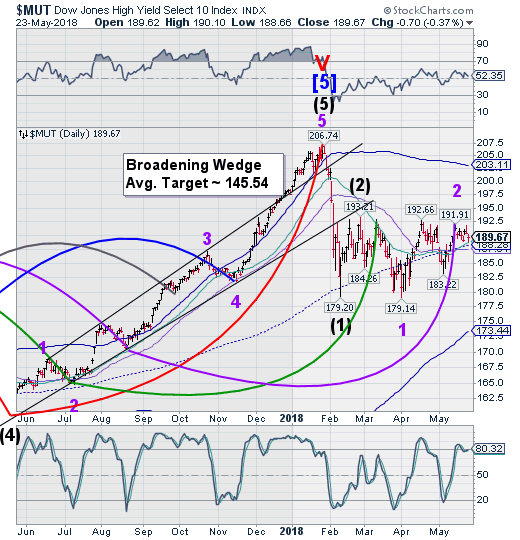

The High Yield Bond Index made its inverted Master Cycle High on May 14 and hasn’t been able to better it since then. Wednesday’s FOMC announcement did nothing to excite bond investors, as it hasn’t been able to make up losses from earlier in the day. Should it decline beneath the cluster of supports currently beneath it, especially the 50-day Moving Average at 187.51, MUT may be on a sell signal.

UST continued its bounce out of its Master Cycle low at 118.27. The turn was logged on May 17th. According to the Commitment of Traders Commercial Traders have somewhat reduced their net longs (616,983 contracts), but still hold the lion’s share. Since this is a zero-sum arrangement, I’d say the Commercials may have the upper hand. The Cycles Model suggests a rally lasting approximately another three weeks.

(ZeroHedge) The big question after the May FOMC statement was "how symmetric is The Fed's reaction function" to inflationary upside, i.e. how much will the Fed allow inflation to overshoot, and how much attention are they really paying to the collapsing yield curve? And as Bloomberg noted, a key focal point of the minutes will be to further distinguish the main thresholds separating the three- and four-hike camps in the 2018 dot plot.

Former fund manager Richard Breslow wrote in his Trader's Notes column earlier:

"I expect there is a decent chance that the FOMC minutes we’re going to see this afternoon read on the hawkish side. What a difference a few weeks make. Way back then Fed-speak was clearly trending to the upbeat side and they were getting even more hopeful on the inflation side of the dual-mandate."

The U.S. Dollar appears to have made a near-perfect 38.2% retracement of its 2017 decline. This suggests the Master Cycle high and “Point 7” may have been achieved today, or nearly so. The window for the reversal may close by the end of the week.

(Quartz) Last year, the US dollar experienced its worst year in more than a decade. But after stumbling through the start of this year, the greenback has finally started to find its feet.

An index of the US currency against a basket of major trading partners is now at its highest level since mid-December, after gaining 4% in the past month, supported by rising US interest rates and a steadily growing economy, and despite the unpredictable policies and statements coming out of the White House.

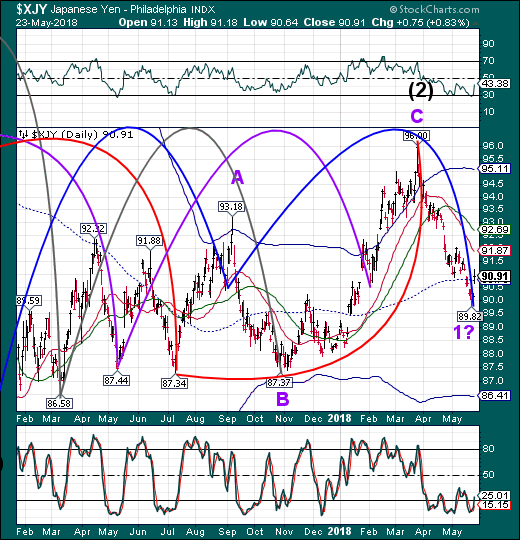

The Yen made a belated Master Cycle low on Tuesday that may have been confirmed by today’s bounce out of the low. The Cycles Model suggests a rally through early June. The 50-day Moving Average would be considered an appropriate target for this bounce.

(MarketWatch) Traditional haven currencies, such as Japan’s yen and, to a lesser extent, the Swiss franc, were on the rise on Wednesday as trade and geopolitical concerns came back into focus and the selloff in high-yielding emerging markets assets intensified.

President Donald Trump on Tuesday said he wasn’t happy with how trade talks between the U.S. and China were progressing, and said the much anticipated U.S.-North Korea summit planned for next month in Singapore might not go ahead as planned, which sent ripples through global financial markets.

The Nikkei appears to have reached an inverted Master Cycle high on Monday at 23050.57. On Wednesday a Panic Cycle may have begun that could find a significant bottom in mid-June. However, the decline may not be complete until the end of July.

(EconomicTimes) Japan's Nikkei share average suffered its biggest fall in two months on Wednesday, as comments from US President Donald Trump rekindled worries about trade friction, hurting steelmakers and shippers among others.

The Nikkei tumbled 1.2 per cent to 22,690, after sliding to 22,650 earlier, the weakest intraday level since May 11.

The Euro continues extending its Master Cycle low today, wiping out the Triangle as a valid formation. Thus far, the drama in the /Euro is in the downside, with the possibility of lasting until the weekend. The ensuing rally in the next two weeks that follow may also be quite dramatic.

(CNBC) The two anti-establishment parties looking to clinch power in Italy will not take the country out of the euro zone and reject the single currency, the co-chief of asset management firm Standard Life Aberdeen told CNBC Wednesday.

The resurgence of the Five Star Movement (M5S) and Lega — two anti-establishment parties putting together the next Italian government — has raised concerns that the third largest euro zone economy could leave the bloc. Both parties have, at different occasions, mentioned plans to depart from the common currency pact, though M5S has softened its stance on the issue over time. Nonetheless, the coalition deal between M5S and Lega does not include any reference to officially leaving the 19-member area.

EuroStoxx 50 Index completed its irregular correction with an (inverted) Master Cycle high on Monday. European stocks may be sitting on the edge of a panic phase in its downtrend that may last up to two months. Crossing mid-cycle support at 3525.01 would leave STOXX on a sell signal.

(MarketWatch) European stocks closed sharply lower on Wednesday, weighed by the return of geopolitical concerns after comments by U.S. President Donald Trump and a round of disappointing eurozone data.

The pound dropped to a 2018 low after U.K. inflation unexpectedly slipped in April.

Gold broke down through its Head & Shoulders neckline, triggering that formation and making a probable Master Cycle low on Monday. The Cycles Model now suggests a bounce lasting into June. However, theHead & Shoulders neckline has already been tested, so anything may happen.

(Reuters) - Gold prices edged higher for a second day on Thursday as the dollar extended losses after minutes of the latest Federal Reserve meeting hinted at a dovish approach to interest rate hikes in the United States.

FUNDAMENTALS

* Spot gold was up 0.1 percent at $1,294.58 per ounce at 0046 GMT, after gaining nearly 0.2 percent in the previous session.

* U.S. gold futures for June delivery were up 0.3 percent at $1,294 per ounce.

* The dollar index, which measures the greenback against a basket of six major currencies, eased 0.1 percent at 93.925.

West Texas Intermediate Crude has been edging along the Cycle Top Resistance, reaching its potential inverted Master Cycle high on Tuesday at72.90. The Cycles Model pinpointed last Wednesday as the reversal date. A however, there’s no telling what a FOMO market can do. A sell signal may be made as it crosses beneath the 50-day Moving Average and trendline at 67.16. Wall Street is still bullish.

(CNBC) Oil prices were mixed on Wednesday after a surprise jump in U.S. crude stockpiles and following a report that OPEC could scale back its deal to limit oil production at its June meeting.

U.S. commercial crude inventories surged by 5.8 million barrels in the week through May 18.That surprised the market, which was expecting a decline based on earlier industry data and a weekly poll of analysts by Reuters.

"That big print on the crude number pretty much sunk the rally for now," said John Kilduff, founding partner at energy hedge fund Again Capital.

The Shanghai Index declined beneath the 50-day Moving Average at 3174.41 today to put it on a sell signal. The downtrend may resume without warning. The Cycles Model suggests a probable panic decline developing through early June.

(ZeroHedge) In an unexpected, but notable, victory for President Trump's aggressive trade agenda and exporters of cars around the globe, China's Ministry of Finance announced Tuesday morning that it would slash passenger car duties to 15%, further opening up the market that’s been a key target of the U.S. in its trade fight with Beijing. This comes less than a month after China decided to ease restrictions on foreign competition in its auto sector and also address some of the US's concerns about intellectual property theft.

The reduction follows a truce that Treasury Secretary Steven Mnuchin announced during a Sunday appearance on "Fox News Sunday". In response, the US has continued to reverse its policy of pressuring telecom giant ZTE, with Trump taking steps to rescue it.

BKX rallied to complete a 65% retracement of its decline and an inverted Master Cycle high as of Tuesday. Gravity may take over the index again as weakness prevails through late May. While Wednesday’s rally gives a brief respite from the decline, BKX remains technically weak.

(CNBC) Small and regional banks are the big beneficiaries of the House-approved bank regulatory relief bill making its way to President Donald Trump's desk for signature this week.

The bill, which passed the House on Tuesday evening by about 100 votes, cuts dozens of large regional lenders off the list of banks considered too big to fail and frees all but the biggest banks from required annual stress testing by regulators.

It is seen as a victory for the banking industry, which has been pushing back at the restrictions since the financial-crisis era Dodd-Frank rules were enacted in 2010.

"I see this as allowing banks to be banks again," said Ed Mills, a policy analyst at Raymond James.

(Reuters) - Wall Street’s dominance over struggling European banks has reached record levels as U.S. firms reap the benefits of booming markets at home, while their transatlantic rivals are trapped in endless restructurings, data showed on Thursday.The top five U.S. banks had 62 percent of revenues among the world’s leading dozen investment banks in the first quarter this year, industry analytics firm CRISIL Coalition said, while the 7 remaining European banks made just 38 percent.

(Bloomberg) Deutsche Bank AG is about to embark on a retreat from a swathe of equities markets across the world, including some on its own doorstep in Europe, according to people familiar with the matter.

Germany’s biggest lender, which is expected to announce a range of restructuring measures to coincide with its annual shareholder meeting Thursday, will sharply reduce its presence in the U.S. market, and has also started cutting activity in the Central Europe, Middle East and Africa region, the people said, asking not to be identified discussing private information.

The decisions spring from a wide-ranging review of the bank’s global equities business. Chief Executive Officer Christian Sewing has indicated that the bank will scale back the business that services hedge funds and the trading of stocks will also be affected, according to people with knowledge of the discussions.

Disclaimer: Nothing in this article should be construed as a personal recommendation to buy, hold or sell short any security. The Practical Investor, LLC (TPI) may provide a status report of ...

more