Hoarding The New Gold: Early History About Structured Finance

Structured finance is best known for taking real world assets, or debt backed by assets, and pushing them off the balance sheet of the banks. Alan Greenspan and others looked for ways to keep banks lending in the face of the need to carry loans on the books. But debt backed by assets was only part of the scheme to pass risk on to counterparties. Treasury debt backed by only faith in the United States allowed counterparties to collateralize risk with a new valuable tool, bonds as collateral. This new gold was hoarded early as you will see.

Alan Greenspan was obsessed with pushing risk off of the banks and placing it into the hands of someone else. He worked in the S&L industry and saw the S&L's get crushed. He said in a speech in 2005:

Derivatives have permitted the unbundling of financial risks. Because risks can be unbundled, individual financial instruments now can be analyzed in terms of their common underlying risk factors, and risks can be managed on a portfolio basis. Partly because of the proposed Basel II capital requirements, the sophisticated risk-management approaches that derivatives have facilitated are being employed more widely and systematically in the banking and financial services industries.

To be sure, the benefits of derivatives, both to individual institutions and to the financial system and the economy as a whole, could be diminished, and financial instability could result, if the risks associated with their use are not managed effectively. Of particular importance is the management of counterparty credit risks. Risk transfer through derivatives is effective only if the parties to whom risk is transferred can perform their contractual obligations. These parties include both derivatives dealers that act as intermediaries in these markets and hedge funds and other nonbank financial entities that increasingly are the ultimate bearers of risk. [emphasis mine]

Securitization of asset backed securities was the preferred way that banks passed the risk to investors, gaining the power to loan again and again.

Securitization failed when the housing bubble in 4 states crashed, when the Fed tightened the money supply after the housing price crash, and when the investors would no longer take the mispriced CDOs and other structured financial products secured by declining real estate values, off the backs of the banks. The banks were forced to keep many bad loans, take loans once off of the balance sheet in SIVs, and taxpayers bailed them out.

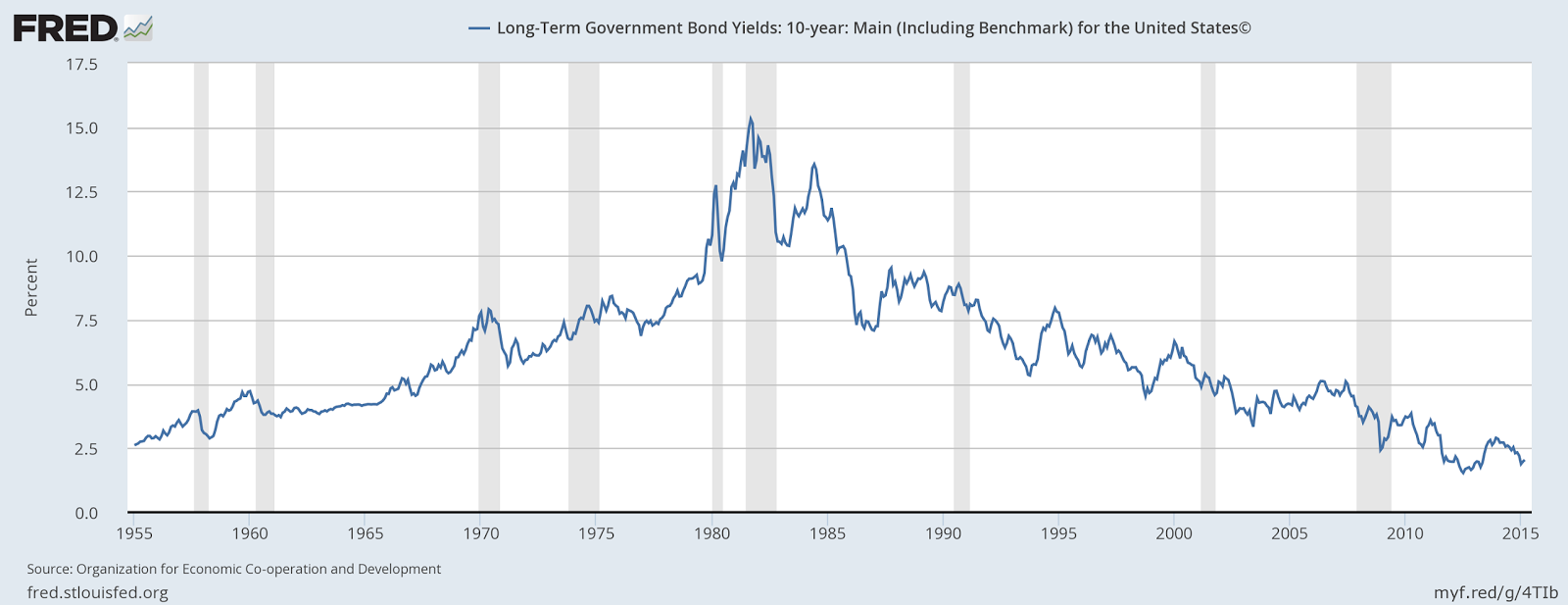

It turns out that treasury bonds were in big demand prior to the explosion of the interest rate swaps markets. They were in demand long before QE, and the demand started in the 1980's, corresponding somewhat to the appointment of Alan Greenspan to the Fed, as he took office in August, 1987. I will cover the shocking tale of Salomon Brothers as this article continues. While all debt assets began to be hoarded near the beginning of Greenspan's tenure, treasury bonds, debt now considered an asset in itself, were also hoarded.

|

|

|

Alan Greenspan presided over much of the relentless march towards zero yield that is continuing to this day. |

Strangely, there could have been noble aspect to this process of banks shedding risk. It keeps the GDP growing, unless the risk is mispriced, as CDOs were mispriced by Basel 2. Big issues with LIBOR and other problems have made this potentially noble effort, removal of risk, into a less noble game that takes advantage of counterparties relentlessly. Even banks complain about it! Structured finance that doesn't alleviate risk, just postponed the day of reckoning and the Fed seemed to freeze up under Bernanke, making the situation much worse.

So, why did the use of interest rate swaps and bond collateral become so important when we had debt backed by real assets? Well, clearly, securitization was hampered by the Great Recession. Securitization was no longer the means by which the banks could alleviate their risk. Interest rate derivatives or swaps became the primary means of protecting banks in the loan making process, as they hedged their bets against the loans they made. But since they worried about their counterparties, think AIG, they wanted clearinghouses to be the center of those hedges, insuring that the system would be fair and that counterparties could be trusted, or come up with collateral if their pledged collateral diminished in value.

As we see in the PIMCO article, vanilla swaps are the most common. Even they have been at the center of dispute, with LIBOR, but they are used extensively. These swaps have existed since the 1980's, according to the PIMCO article. As we see by the behavior of Salomon Brothers, taking on risk as a counterparty required new tools and a hoarding of the new gold.

Salomon Brothers and others did set up collateral management roughly corresponding to the installment of Greenspan in the summer of 1987, as Fed chairman. And in 1990-91, this startling action took place showing that people needed bonds, and were willing to hoard lots of them:

In 1991, US Treasury Deputy Assistant Secretary Mike Basham learned that Salomon trader Paul Mozer had been submitting false bids in an attempt to purchase more treasury bonds than permitted by one buyer during the period between December 1990 and May 1991. Salomon was fined $290 million for this infraction, the largest fine ever levied on an investment bank at the time. The firm was weakened by the scandal, which led to its acquisition by Travelers Group. CEO Gutfreund left the company in August 1991 and a U.S. Securities and Exchange Commission (SEC) settlement resulted in a fine of $100,000 and his being barred from serving as a chief executive of a brokerage firm.[10] The scandal was then documented in the 1993 book Nightmare on Wall Street.

Business insiders wanted the new gold in a big way even before the modern interest rate swap market we now see took off. The conspiracy to buy bonds was surely fostered by Alan Greenspan as he certainly encouraged "sophisticated risk management approaches" from the beginning of his term as Fed chairman, because you could collateralize them to limit bank risk.

The relentless slide toward zero rates and even toward negative, is proven to be a function of bank risk aversion, and of the central bank's willingness to accommodate that risk aversion no matter what happens to the real economy.

Big bond demand pushes derivatives risk off of bank balance sheets, unless the new clearing houses go bust, and you know what would happen after that. So far, the Fed has been able to keep a little growth going forward, and stability has been achieved. But if the real economy starts to fail, would the Fed ban bonds as an asset class? Or would the Fed get base money into the hands of the people?

Greenspan succeeded in creating a system that achieves what could be long term stability for the banks. But this system has caused America to be hollowed out, with prosperity eluding many in the real economy. Worse yet, it causes the march towards negative yields to be relentless in its nature. Lack of sufficient new gold in the system could prove to be its undoing.

For Further Reading:

Disclosure: I am not an investment counselor nor am I an attorney so my views are not to be considered investment advice.