Fed Front-Loaded An Enormous Stock Market Rally

Richard W. Fisher served as the President of the Federal Reserve Bank of Dallas for more than a decade (2005-2015). His appearance on CNBC this week offered remarkable insight into why voting members on the Federal Reserve Open Market Committee (FOMC) embraced zero percent rate policy as well as quantitative easing (QE) for so many years.

One of the most controversial statements? Fisher candidly admitted, “What the Fed did, and I was part of it, was front-loaded an enormous market rally in order to create a wealth effect.”

He did not say that the Fed sought to achieve maximum employment. He did not bring up inflation targeting or stable prices either. Rather, one of the world’s most influential people in any room acknowledged that the Fed wanted to push stocks higher to make participants feel wealthier.

How was this wealth effect supposed to benefit workers? Or promote stable rates of inflation? Presumably, when people feel wealthy, they spend more. When they spend more, corporations see more revenue from the goods and services that they provide. When companies achieve better top-line and bottom-line results, executives express greater confidence by adding new employees. When an increasing number of workers find jobs, unemployment falls to lower and lower levels until, eventually, maximum employment spurs wage growth and desirable levels of inflation.

That was the plan.

However, there have been several problems with the Fed’s wealth effect ambitions. For one thing, keeping borrowing costs so low for so long primarily benefited those who were already in decent shape. Wealthier folks have super-sized stakes in the stock market and were able to increase the value of their portfolios substantially; less wealthy folks have seen erosion in real (inflation-adjusted) household income – money that most live month-to-month on. Those in the highest marginal tax brackets were able to add to their real estate holdings. In contrast, very few families in the middle or lower-middle class had the resources to acquire short sales or foreclosures.

Another problem with the Fed’s wealth effect agenda? Corporations leveraged themselves to the hilt. Borrowing money on the “ultra-cheap” allowed them to buy back copious amounts of stock shares. That helped shareholders of those stocks, but it did not bring back labor participation rates to pre-recession levels. The all-important 25-54 year-old demographic is still hemorrhaging workers.

Corporations never really went on the anticipated hiring binge. Instead, they went on a seven-year stock buying spree with the Fed’s easy money. Total debt levels have doubled since 2007. And while the average interest rate paid on corporate debt has declined, interest expense has risen dramatically. Do we even want to ruminate about what will happen if the Fed pushes borrowing costs up appreciably in 2016 and 2017? As it stands, corporations already need to allocate significantly more net income toward servicing the interest on existing loans.

So Richard Fisher acknowledged what many people believed all along. Specifically, the Fed’s primary goal since the banking crisis in 2008 has been to push stock and real estate markets to new heights. In doing so, they hoped that the wealth effect would indirectly achieve its dual mandate of stable prices and maximum employment.

Of course, when you front-load an enormous stock market rally, won’t stock prices reach exorbitant valuation levels? Is there a painful period of reckoning on the back side? Did anyone at the Fed consider what history teaches us about overvalued stock markets and overvalued real estate markets?

Mr. Fisher may not have given the questions much thought during his tenure on the FOMC. However, he revealed his current thinking to CNBC:

“These markets are heavily priced. They are trading at 19.5x earnings without having the top-line growth you would like to have. We are late in the cycle. These [markets] are richly priced. They are not cheap. I could see a significant downside. I could also see a flat market for quite some time, digesting that enormous return the Fed engineered for six years.”

Obviously, the former President of the Dallas Fed cannot predict market direction. Nobody can. And one might argue that a monetary policy wonk does not a valuation guru make. On the other hand, Fisher’s valuation concerns may have merit. For S&P 500 operating earnings of $106.4 (12/31/15) to reach current year-end estimates of $125.6, they would need to grow 18%. At $125.6 and the S&P 500 at 1950, the Forward P/E becomes 15.5.

Yet analysts have been ratcheting down expectations from 10% earnings growth to 7.5%. (And in 2015, growth flat-lined entirely). If one generously accepts the wisdom of analysts at 7.5% operating earnings growth, and the S&P 500 at 1950, the Forward P/E on a year-end estimate of $114.4 becomes 17. The 35-year average Forward P/E is 13.2.

That’s right. Even after January’s stock carnage that has seen the S&P 500 crater 100 points from 2043 to 1943, the stock market is still pricey. Reverting to the average Forward P/E would require operating earnings to reach $114.4 at year-end AND the S&P 500 to sink to roughly 1515. That would be in line with a typical bear market descent of 28.9% from the peak (2130).

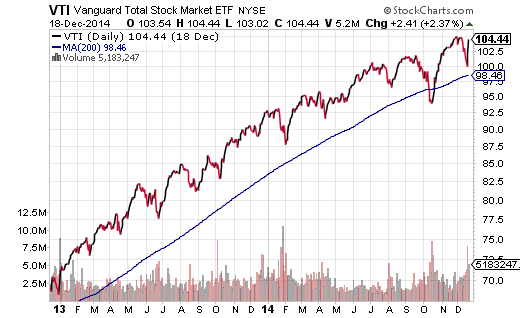

Valuation concerns notwithstanding, there’s little doubt that the Fed did indeed front-load an enormous market rally. Here’s how easy it is to tell. Take a peek at how Vanguard Total Market (VTI) fared as it relates to the Fed’s acquisition of bond assets with electronic dollar credits (a.k.a. “QE”). Specifically, in mid-December of 2012, the U.S. Federal Reserve upped its QE3 program to $85 billion per month in the acquisition of U.S. treasuries and mortgage-backed securities. The program began winding down in 2014 during the “Great Taper,” though the final day of the last asset purchase actually occurred in mid-December of 2014. The 2-year performance for VTI? Approximately 52%.

Now visualize what transpired when the Fed officially removed its QE3 stimulus. Through 1/7/16, there has been a whole lot of risk and volatility. There hasn’t been a whole lot of reward.

Surprising? Not particularly. In fact, “risk-off” treasury bonds via iShares 7-10 Year Treasury (IEF) have outperformed “risk-on”stocks since the end of the Fed’s QE.

Disclosure: ETF Expert is a web log (”blog”) that makes the world of ETFs easier to understand. Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered ...

more