3-ways Millennials Can Learn To Trust The Markets

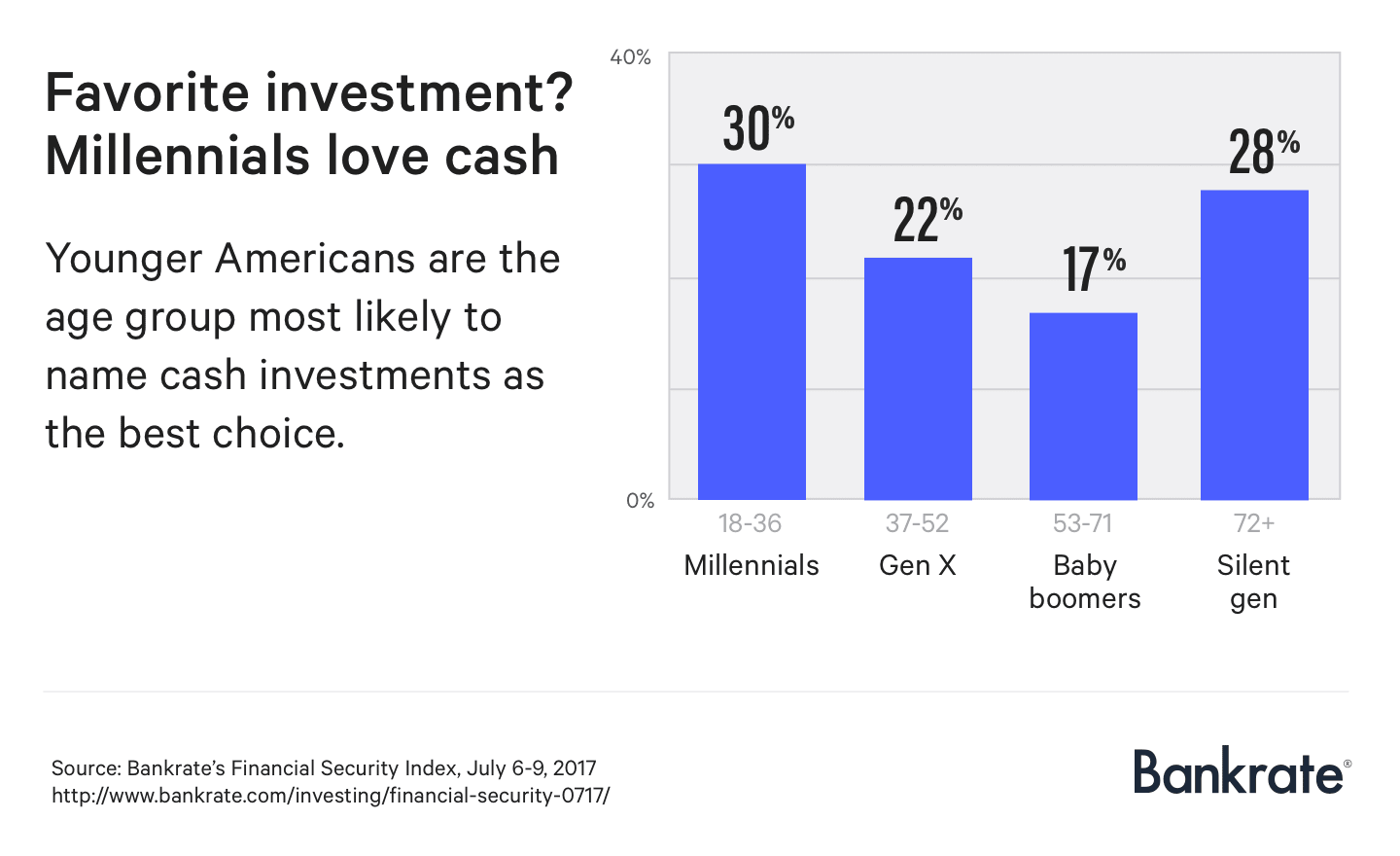

According to a recent study by Bankrate.com, only 13% of millennials said they’d invest in the stock market. Cash is king.

Naturally, this phenomenon has the majority of Wall Street experts besides themselves as stocks seemingly are the only game in town.

Millennials (those born 1977-1995), have so much precious time to weather losses. The cohort is ripe for brainwashing. Wall Street boasts defiantly:

“You need us more than we need you!”

Yet, many in this group shrug and ignore.

Main Street millennials appear to know something Wall Street professionals don’t.

I hate to break it to the experts. The skepticism is spreading.

Generation Z (born in mid-90s to mid-2000s), isn’t enamored with the stale story that stocks only grow to the sky.

I know. I regularly partner with and coach this demographic cohort including my own daughter.

The majority are indeed risk averse; perhaps even more so than millennials.

Obviously, there are a myriad of motivations for this aversion to stocks – lack of knowledge, student loan over indebtedness, a touch of Great Recession mindset as ground-level witnesses to household economic collapse, personal financial fragility, and let’s not forget: outright distrust (which I believe to a degree, is a formidable concern).

Now, for someone like me who has been a student of the market and individual stocks since age 16, I am disheartened by these studies. I still believe the stock market should be a portion of a young adult’s wealth-building plan. It’s just not a panacea as relentlessly touted. If the pros didn’t make stock investing sound so definitely positive and objectively exposed the risks too, perhaps we’d see a healthier stock market participation rate.

My first year in the financial services industry was 1988, in the midst of a great bull market. However, I expected the industry, those who preached stale theories and ostensibly set investor portfolios up for the kill, to change their tunes about allocations and risk after the tech bubble burst in 2000. I had encouraged investors to shift portfolios to more balanced, less aggressive allocations, as early as 1998. Markets cycle data has been out there for what feels like an eternity, yet now more than ever, it’s rarely discussed.

However, the facts are the facts. Markets shift; they’re more than just bull as the public is led to erroneously understand. Although bull markets occur historically with greater frequency, people are surprised to discover that since 1877, bear markets have accounted for 40 percent of market cycles.

Yet, the narrative doesn’t budge. In the media and in front-line closed-door prospect and client meetings at brokerage firms, the stock market fantasy bull is the financial Energizer Bunny. The bullish flipcharts keep flipping; visuals are designed to foster regret if one “misses out,” on the endless bliss of stock returns. Those that outline risk of loss are nowhere to be found.

I believe it to be blatantly irresponsible. Retail big-box investment factories are steadfast “set it and forget it,” peddlers. I’m amazed at their tenacity.

The spiel is rarely altered. Minds never change.

Respected academics do change their minds.

Objective students of market history do.

What has changed is how millennials and generations which follow, are on to the biased rhetoric. Sadly, chronic skepticism and trepidation is hurting younger generations as they should participate in stock investing. They just don’t know who to trust.

Candidly, articles like this – You probably have the wrong idea when it comes to investments. Let’s fix that, don’t fix anything. They showcase the willful arrogance of financial pros and motivates millennials to stay away.

It’s replete with narratives taken out of context like –

“putting your money into safe investments can actually cost you money, if you consider inflation.”

Well, that’s stretching the truth a bit. It depends on the valuations of stocks.

I may assume after reading this piece that stocks always possess less risk than cash, when in fact depending on when they’re purchased, stocks are not the wisest choice. Hoarding excess cash (above that required for emergency reserves and short-term goals that require liquidity), and never seeking to invest in risk assets, I’ll relent is not a smart long-term decision. However, generalizations do nothing to bolster confidence of younger generations. If anything, it turns them off.

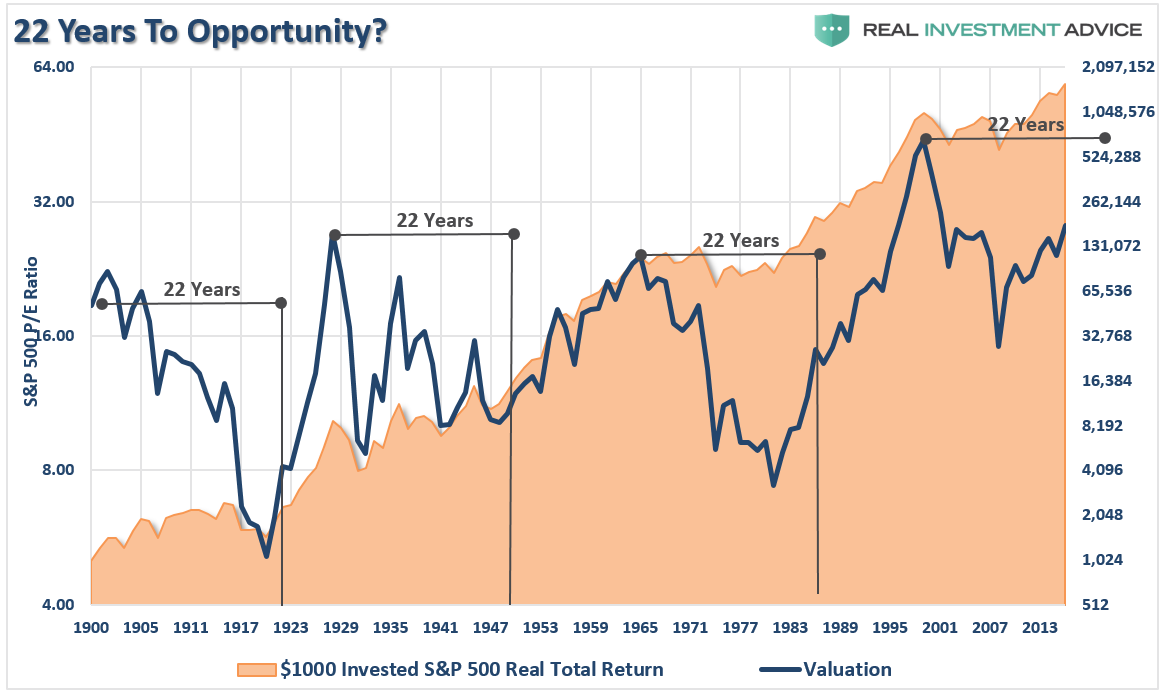

Take note of the point made in the above chart. When investing money when markets are above 20x earnings, it was 22-years before it grew more than money stuffed in a mattress. Why 22 years?

Historically, it has generally taken roughly 22-years to resolve a period of over-valuation. Given the last major over-valuation period started in 1999, history suggests another major market downturn will mean revert valuations by 2021.

So, let’s give millennials some credit for being overly cautious at this juncture.

Oh, and another thing.

I’m convinced capitalism has lost a bit of its luster. The corporate structure, the CEO as paternalistic hero, the one who does right by employees. Well, that individual died during the financial crisis and isn’t making a return anytime soon. A millennial recently lamented – “I don’t trust corporate executives to make the right decisions for my career. They only care about shareholders.”

I reluctantly needed to agree with this rather mature observation.

I’ll explain:

When I was studying markets and stocks at a young age, I observed that the executive-suite made primarily long-term decisions for the good of the organization and those who work, invest and spend on their products and services. That perspective was blown away post-financial crisis.

I’m not naïve enough to believe that corporate leadership is always concerned about the long term. That would be foolish. Quarterly company reporting and jumping of guidance hurdles have been around for an eternity. However, I never would have assumed that financial alchemy or corporations cooking the books would lead to such outstanding stock performance for so long.

Young, potential investors can’t figure out where to get the real story about risk and reward. They feel that the key driver to any corporate decision and associated stock moves are nothing but personal greed. Vapor. It’s all not real. So why would they be excited to invest? Greed eventually turns to fear. They witnessed how the overall financial system was close to toppling in 2008. They haven’t forgotten. They shouldn’t.

Michael Dell, the founder of Dell Computers deserves laudable credit for taking his company private in 2013 along with his partners at Silver Lake Management.

“Privatization has unleashed the passion of our team members who have the freedom to focus first on innovating for customers in a way that was not always possible when striving to meet the quarterly demands of Wall Street.” – Michael Dell in commentary personally written for The Wall Street Journal.

Investors regardless of age are facing a stock market that continues to shrink. Less companies are seeking to go public; there are a rising number of companies looking to be privatized again.

Overall, these structural changes to the market are creating monopolistic structures where a handful of the largest companies overwhelm indexes and opportunities. Younger generations that have an interest in becoming students of market like I did, are feeling the effort isn’t worth it. There’s an overarching thought that the “system is rigged.”Ostensibly, a solution to this dilemma is the “robo advisor.”

Photo illustration by Justin Metz for Fortune Magazine – May 2016.

Indeed, a roboadvisor does offer several benefits – low operating costs, a passive (index) investment portfolio mix that is periodically rebalanced.

Robos have good intentions. Unfortunately, their buy and hold methodologies are missing a crucial component that skeptical millennials want. That is – a rebalancing strategy coupled with a risk management discipline to protect capital as market cycles change.

The pros bellow –

“That’s market timing and NOBODY can time the market!”

Market timing is an all-or-none decision. I’ve yet to witness anybody who can accomplish this task, at least consistently.

So, no – that’s a cop out.

Risk management is a rules-based process designed to minimize time and capital erosion. It can be accomplished.

Millennials and Gen Z shouldn’t be deprived of the long-term benefits of investing, especially in stocks.

Trust is the foundation for action.

Here are several ways millennials can learn to trust the stock market.

First, for gosh sake’s, those who work in financial services, please give full-circle guidance.

Validate what millennials already know. The stock market is risky regardless of time frame. Losses can place wealth in jeopardy, put plans on hold. Listen, you can’t fool them – They’ve seen the math of loss in action through the Great Recession with parents, grandparents, family of friends. So, do some reading away from the biased research your employers’ strategists regurgitate and you suck up like baby birds.

Don’t beat around the bush about risk. Don’t minimize the impact. Evasiveness and incomplete information will only serve to keep this group frozen in cash indefinitely, and that would be an injustice.

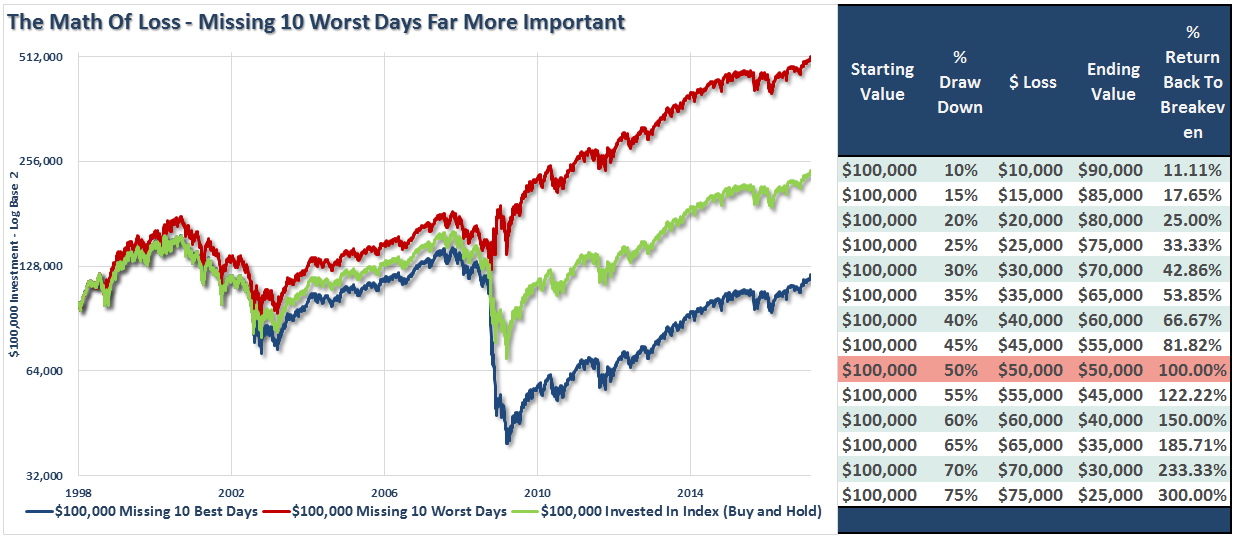

Instead of showcasing the chart that outlines how missing the best 10 market days diminishes returns, also expose them to how missing the 10 worst days can create great wealth devastation.

Just tell the damn truth. Share the pros and cons of stock investing, cut out the sales-oriented biases and maybe, just maybe, we as financial professionals can salvage this thing for millennials.

Financial professionals: Help millennials understand how healthy, holistic financial habits, including risk-adjusted investing is crucial to a lifetime of fiscal well-being.

Investing is never an isolated activity. It’s a segment of an overall plan to achieve financial satisfaction. Explain how several disciplines of personal finance remain steadfast and true – teach them to pay themselves first, make saving a part of how they live and breathe, discuss the risks they must strive to mitigate like disability and catastrophic illness.

Help them to redefine investing (it isn’t all about the stock market). Capital should be allocated to learning or enhancing personal skill sets to bolster lifetime earnings, passive real estate, funding business ventures, pursuing dreams that create the wealth that may continue to grow with stocks as part of the overall framework.

Sadly, sales goals may be feeding your myopia, blinding you to other points of view. Step back and consider making a true impact with younger generations, including your own children. “Stocks for the long run,” frankly is a flimsy message that will crack easily when the next bear market arrives (and it will).

Millennials and Gen X: Go ahead and invest in target-date funds, but add a rule.

Once the goal of six months of living expenses socked away in an emergency reserve is met, it’s time to focus on payroll deductions in to your employer-provided retirement plan. Go ahead and ‘pay yourself first’ and funnel 15% of gross income into the plan. I know. It sounds ominous.

But go for it.

Go for the payroll deduction FIRST, then adjust the budget to meet it. I call this a ‘cold-water discipline.’ In other words, like the initial shock of diving into cold water that ostensibly fades to delightful, even warm bliss, establishing the saving initiative upfront and taking the plunge will compel you to adapt and subsequently adjust. Eventually, you’ll raise the deduction bar higher. I’ve witnessed this positive change work repeatedly.

Now for the ugly part. Hear me out.

In 2007, the Department of Labor placed a stamp of approval on target-date fund choices in 401(k) plans; naturally, plan providers have been quick to embrace them.

A target date fund is a mix of asset classes – large, small, international company stocks and fixed income that is adjusted over time or allocated conservatively the closer an employee is to the ‘target date’ identified.

For example, the Vanguard Target Retirement 2020 Fund is designed to increase its exposure to bonds the closer it gets to 2020. Let’s be clear – this is NOT a maturity date, which is part of the confusion of a target-date fund. The target is never reached. The fund doesn’t go away. It’s always out there.

Also, as a rational human, in 2020, the so-called retirement or target year, wouldn’t you intuitively think this fund should be a conservative allocation? Perhaps 30% equities and 70% fixed income? Well, it all depends on a target date fund’s ‘glide path,’ or method of how the allocation is reshuffled the closer the time to the target date. Every fund group differs in philosophy so you must read the fine print.

Hey, we need to work with what you have available; let’s make the best of it now that you know the facts.

Here’s the first rule (if you choose to accept it): The years identified in your selections of employer-provided target date funds should be redefined. Consider the years as benchmarks to expand or contract your risk burden. Switch target-date funds based on current stock valuations. This should be easy to accomplish in a company retirement plan like a 401(k).

Second tenet: Once average inflation-adjusted earnings are or the Cyclically Adjusted PE Ratio exceeds 23X (like today), consider it a motivation to reduce risk (the target date).

Here’s an example:

You’re 22 years old in 2017 with an estimated retirement age of 67. Welcome to 2062!

Your new employer plan has the Vanguard Target Retirement 2065 Fund and the Vanguard Target Retirement 2020 Fund among investment choices. The 2065 fund has 90% domestic and international stock market exposure. The 2020 option is comprised of roughly 56% in global stock markets with the remainder in global bonds. Generally, bonds should be a flight to safety when stock markets are in correction or in bear cycles.

Today, with the CAPE at a shade light of 30x, direct 15% payroll deduction into the 2020 option and be willing to transfer and contribute to the 2065 fund when the valuation rule is triggered. The 2020 fund is a blended selection. It’s a ‘cake and eat it’ option, right? You’ll participate in a risk-adjusted manner in the market when stocks are expensive; risk may be increased as valuations become attractive (2065 alternative).

Is this method perfect? No.

Will you miss out on a few percentage points of return if stocks roar higher? Absolutely.

However, over long periods your returns will be consistent thus minimizing the precious time required to break even from losses.

Will many brokers abhor this rule? I’m certain of it. As stocks are a form of financial panacea (in their minds), the default or irresponsible tale spun must be the younger you are, the greater risks you must take.

Stock risk is risk. The market has sweet spot designated by age. Regardless, just starting out or about to retire, if risk-adjusted return estimates are favorable you take advantage of them. Is this so difficult?

Millennials and Gen Z, I’m sorry. We’ve failed you.

As an industry, we can do better. However, we probably won’t.

Our concept of ‘doing good’ is to create new products that can be marketed effectively for ongoing revenue generation, like roboadvisors.

Fortunately, many of you are on to us.

However, I don’t want you to use it as an excuse to miss out on stock investing.

I will continue to influence younger generations; I’m armed with the truth. They participate in markets armed with healthy, realistic attitudes. These young partners study and own individual stocks, exchange-traded and mutual funds.

Millennials I counsel understand the benefits of life insurance and lifetime income options.

They have a passion to improve their human capital contributions, strengthen skill sets and grow to be valuable contributors, thought leaders in the workplace. They attain consistent wage increases; some become successful entrepreneurs.

All wisely manage debt and are not chained to big mortgages and fancy automobiles.

I’m doing my part to make a difference. So, other financial pros. Let me ask. What are you up to?