In the old vaudeville days of theatre, the comedian would often start his sketch with the familiar phrase, “a funny thing happen on the way to the theatre”. Adapting that line to the Federal Reserve’s policy stance, a funny thing is happening as short-term interest rates head back to the so-called normal range.

I have written in previous blogs about the deflationary forces that prevent the monetary authorities from reaching their inflation target of 2%[1] [2]. So, the first“funny thing that happened “ is that rate of inflation, not only did not pick up but actually decelerated in the past year. The low level of inflation, once considered to be transitory, seems to have a much greater hold on the economy.

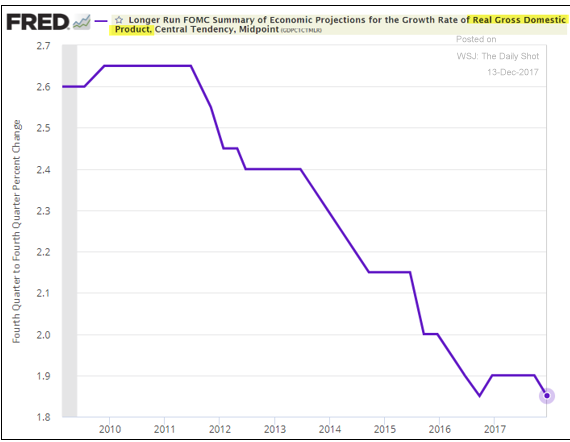

The second “funny thing” is economic growth projections declined as rate increases were introduced. Growth and inflation are correlated. Inflation can be a by-product of rapid growth, just as deflation can be a by-product of a growth slowdown.

The Fed has had to recalibrate its growth projections yearly. In 2010, the Fed projected that economic growth in the longer run (no specific time period was set) would return to 2.6%. Ever since that year, successive projections have consistently declined to the point where the rate projected in the most recent meeting this December was set at 1.85 %. The central bank does not foresee a permanent boost to growth either from monetary or fiscal policy changes.

As the Fed funds rate moves towards “normalization”, the growth projections are ratcheted down. The Fed’s dot plan anticipates that rates will continue to move up steadily into 2019. The members, as a whole, expect to raise rates another 4 times in 2018. The consensus is that implied Fed funds rate in 2018will be 2.50%, moving up to 3.0% in 2019. Yet, all the while, their growth forecasts move in exactly the opposite direction. Interest rates move up and economic growth rates are scaled back. It is as if growth has no influence on setting monetary policy.

[1] The Digital World Challenges Central Bankers

[2] More On Why Central Bankers Find It So Hard To Reach Their Inflation Targets

Comments

Log in or sign up to join the conversation.