You Are Different This Time

You don’t always see a respected member of the financial commentariat argue that it’s different this time. But that’s almost what Morningstar’s Christine Benz has done in an excellent recent article.

What Benz means is that you’re different now than you were during past market cycles. More specifically, you’re older now than you were during the last market debacle, so you have less time to recover from another one if it should occur. That might not mean much if you were 10 in 2008 and 20 now. But it means a lot if you were, say, 50 in 2008 and 60 now or even 45 in 2008 and 55 now. If you’re five to 10 years from retirement, the risk of encountering a period when bonds outperform stocks is high enough – and dangerous enough to your retirement plans — so that you should reduce stock exposure.

The Math Is Different in Distribution

And, if you’re retired and withdrawing from your portfolio, the “sequence-of-return” risk – the problem of the early years of withdrawals coinciding with a declining portfolio – can upend your entire retirement. That’s because a portfolio in distribution that experiences severe declines at the beginning of the distribution phase, cannot recover when the stock market finally rebounds. Because of the distributions, there is less money in the portfolio to benefit from stock gains when they eventually materialize again.

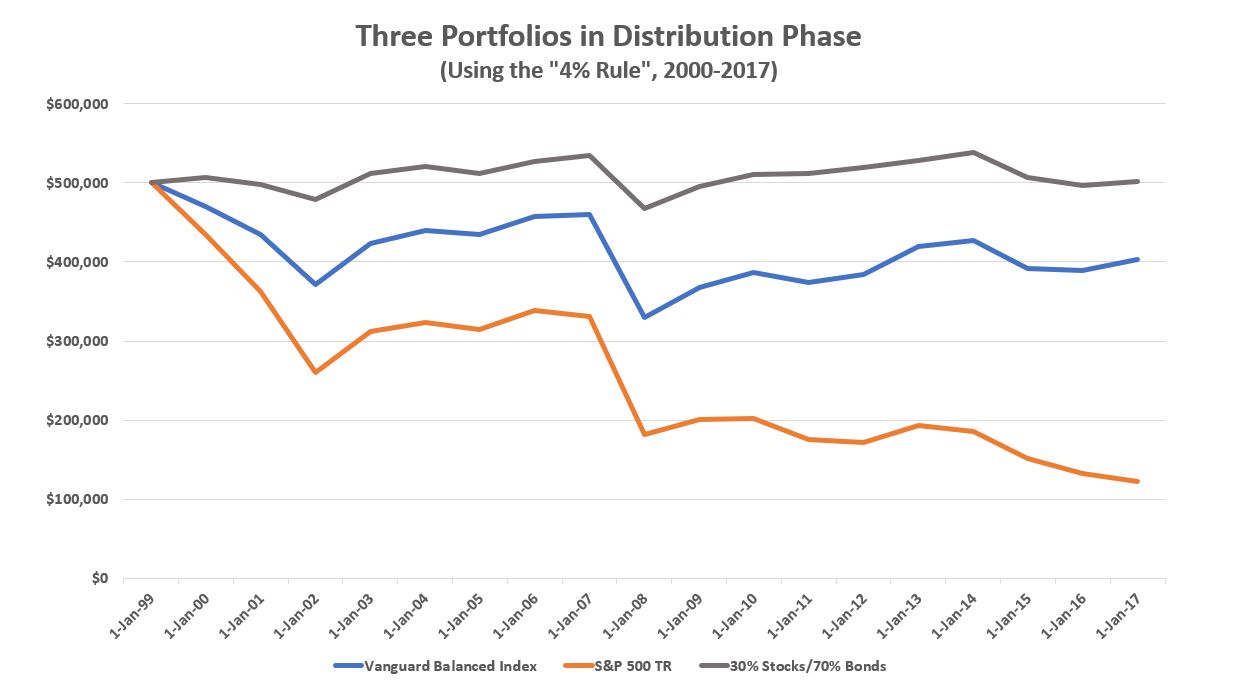

I showed that risk in a previous article where I created the following chart representing three hypothetical portfolios using the “4% rule” (withdrawing 4% of the portfolio the first year of retirement and increasing that withdrawal dollar value by 4% every year thereafter). I cherry-picked the initial year of retirement, of course (2000), so that my graphic represents a kind of worst case, or at least a very bad case, scenario. But investors close to retirement should keep that in mind because current stock prices are historically high and bond yields are historically low. That means the prospects for big investment returns over the next decade are dim and that increasing stock exposure could be detrimental to retirement plans once again. In my example, decreasing stock exposure benefits the portfolio in distribution phase, and that could be the case for retirees now.

The Psychology Is Different In Distribution

But it isn’t just that stock prices are high and that bond yields are low now. Benz argues that your mindset is likely different too. “Even if you sailed through the 2007-2009 market meltdown without undue worry or panic-selling, the next downturn could prove more visceral if retirement is closer at hand and starting to seem like a realistic possibility. It’s not fun to see your portfolio drop from $500,000 to $225,000 when you’re 45. But it’s way worse to see your $1 million portfolio drop to $450,000 when you’re 55 and beginning to think serious thoughts about the when and how of your retirement. The losses are the same (in percentage terms); the ages are different.” In other words, your proximity to retirement could make you sell at the bottom more than it might have a decade ago.

Sure, everyone probably needs some stocks in their portfolio in retirement. Returns from cash and bonds may not keep up with inflation, after all. But stock returns might fall short too. And if stocks do lag, they probably won’t do so with the limited volatility that bonds tend to deliver, barring a serious bout of inflation. So, if you’re within a decade of retirement, it may be time to think hard about how much stock exposure is enough. The answer might be less than you think for a portfolio in distribution phase.