Which Smart Beta Was Smartest In October?

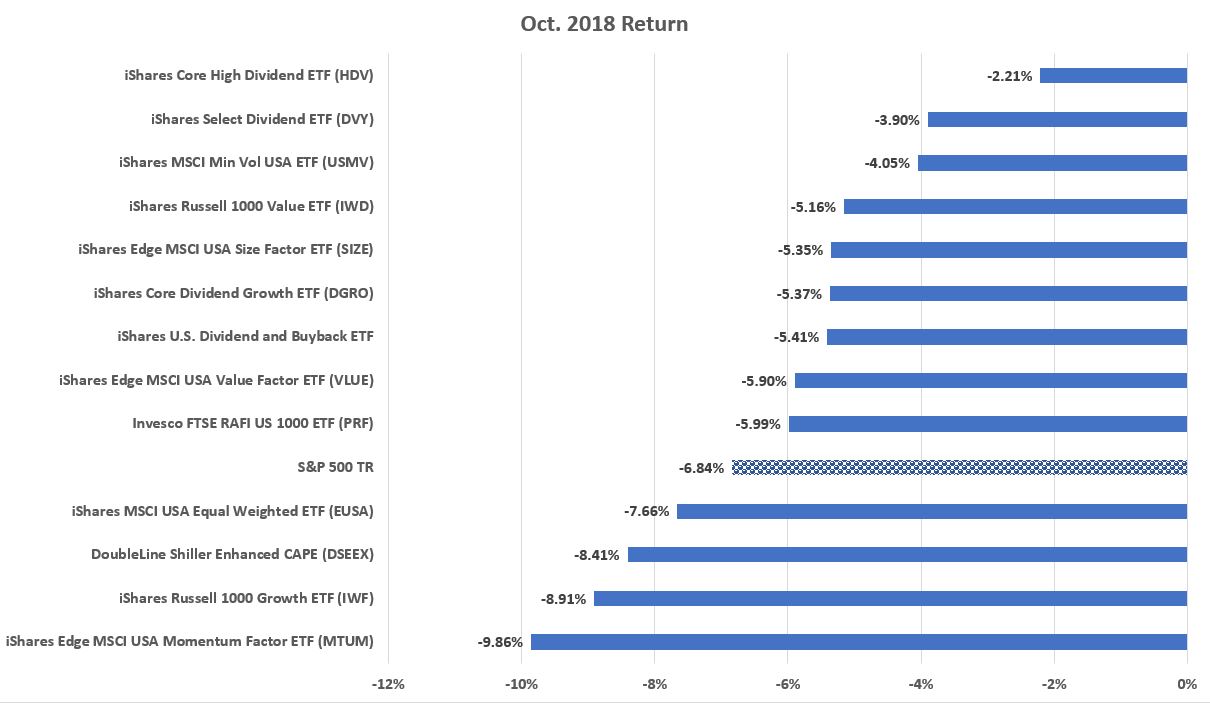

It’s no secret that October was a bad month for stocks. The S&P 500 Index dropped nearly 7%, including dividends. Granted, the index still had a positive return for the year after the decline, but October wiped out nearly all the gains the index had posted for the year up to then.

Given the increasing popularity of “smart beta” strategies – portfolios tracking an index organized around a factor such as a stock’s valuation, size, dividend payout, price momentum, etc…, we thought it would be a good time to see how various strategies held up during the difficult month. It turns out, value and dividend strategies tended to hold up better than growth and momentum strategies.

For example, using mostly a variety of iShares funds, the iShares Core High Dividend ETF (HDV) was the best fund on our list, clocking a loss of 2.21% for the month. The second-best fund was the iShares Select Dividend ETF (DVY), which posted a 3.9% loss. Every dividend factor ETF that iShrares has outpaced the S&P 500 for the month.

Similarly, all value strategies did relatively well for the month. And the value-over-growth theme was on display in the Russell 1000 returns too. The iShares Russell 1000 Value ETF (IWD) posted a 5.16% loss for the quarter. That was a favorable showing versus the 6.84% loss of the S&P 500 and the 8.91% loss of the iShares Russell 100 Growth ETF (IWF).

Minimum volatility strategies such as the iShrares MSCI Min Vol USA EGTF (USMV), which lost 4.05% for the month, also did relatively well. Minimum volatility strategies were first developed by a professor of finance named Robert Haugen, who didn’t agree with the modern academic finance notion that volatility defined risk. The theory states that higher return must come from higher volatility or, to say the same thing, higher risk stocks. But Haugen thought lower volatility stocks could produce higher returns over long periods of time. A student of Benjamin Graham, Haugen suspected that higher volatility stocks were those Graham called “glamor” stocks that were market darlings for a time, but whose businesses ultimately couldn’t support the lofty prices the market awarded them. Better to own the steadier stocks of steadier businesses that didn’t inspire infatuation – and then great disappointment — in the market, thought Haugen.

Sure enough, those glamor stocks struggled in October. The iShares Russell 1000 Growth ETF (IWF) lost nearly 9% while the iShares Edge MSCI USA Momentum Factor ETF (MTUM) lost nearly 10%. The top holdings of the Russell 1000 Growth Index are Apple, Microsoft, Amazon, Facebook, and Alphabet. Two of those, Microsoft and Amazon, are also top holdings of the momentum fund in addition to Visa, Boeing, and Mastercard.

It’s important to note that I examined a lot of iShares funds, and many of them have a unique way of doing smart beta. Often different factors can emphasize different sectors. For example, a quality sector may emphasize consumer staples and consumer discretionary, while a value factor emphasizes energy, materials, and industrials, which generally trade at lower valuation multiples than, say, technology and healthcare. The iShares funds, however, do things a little differently. The quality fund picks the highest quality stocks from each sector. So the fund’s sector distribution is the same as the S&P 500 Index, which wouldn’t be the case if the fund simply chose the stocks that scored the highest on a quality screen. The difference between the fund and the index is simply that the fund emphasizes different stocks in each sector than the index.

In any case, the results from October suggest that investors should be alert to a rotation from more aggressive and inherently richly priced sectors to cheaper ones.