Zillow’s Bottom-Line To Suffer Once Again?

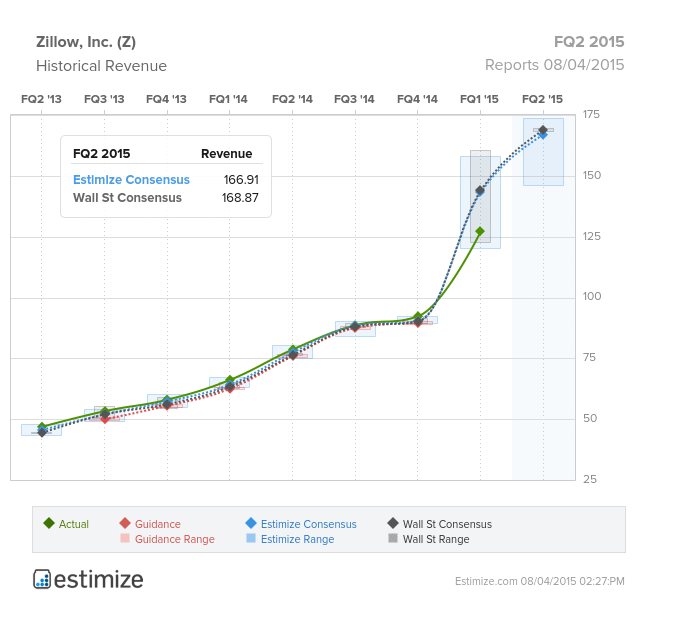

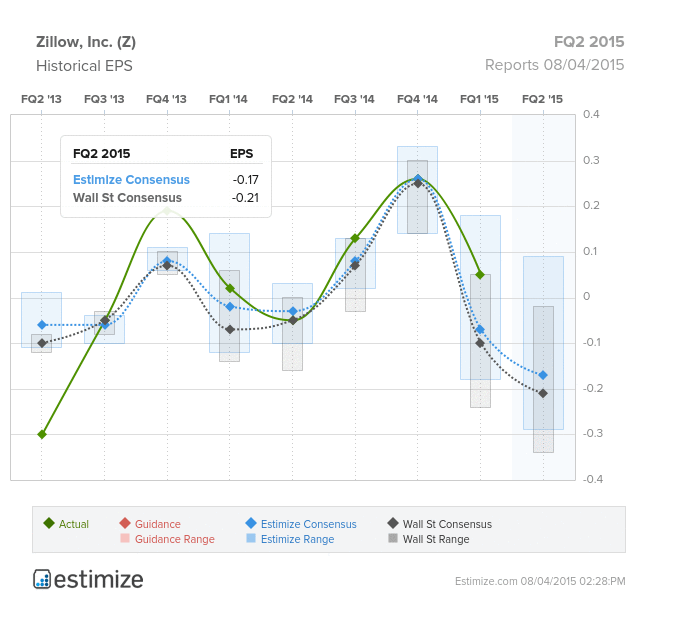

Zillow Group Inc. (Z) will report its FQ2 ’15 figures after the closing bell this afternoon. Sentiment heading into the result for Zillow is definitely negative with the stock falling over 8% in the past 30 days. Wall Street and the Estimize community are expecting a fall in EPS YoY and QoQ. Estimize are predicting an EPS figure of -$0.17 and Wall Street is predicting -$0.21. In terms of revenues, Estimize are predicting a figure of $166.83M and Wall Street comes in slightly above this figure at $168.87.

Zillow provides online content on real estate and other home-related information through mobile technology and the web. Zillow has a portfolio of specialized products targeting varying sectors of the market. Some of Zillow’s key brands are Zillow, Trulia (recently acquired) and StreetEasy.

Peak housing season should be kind to Zillow’s monthly unique visitors, which in January 2015 hit 36M, but the Q1 acquisition of Trulia will add a significant amount more. The company has been doing well with respect to driving revenues on both sides of its business: marketplace revenues, which consists of local real estate agent subscriptions, ad display revenues from advertising.

The problems for Zillow do not stem from the company’s ability to increase revenues or produce gross profit margins. In their FQ1 ’15 results, Zillow sported an impressive YoY revenue growth figure of 92.13% and a gross profit margin of 89.77%. Despite these impressive numbers, Zillow continues to lose money on the bottom line. Unfortunately for Zillow’s shareholders, the increased revenues are a result of an increase in sales and marketing expense, circa 49% of Zillow’s revenues are attributed to sales and marketing. This business model is clearly not desirable as management have no leverage or economies of scale with its expansion in revenues. In order for Zillow to grow its revenues, management must boost its expenses and therefore depresses the bottom line.

The lack of leverage in Zillow’s business model is not the only issue for management, increased competition is also going to be an increasingly painful annoyance moving forward. News Corp (NWS) recently purchased realtor.com and has stated that they intend on boosting the online real estate listings site’s advertising budget. Realtor.com already has a comparative advantage over Zillow, with their online feeds getting updated directly from real estate agents’ databases every fifteen minutes as compared to the much slower and stagnant manual process that Zillow currently offers.

The report this afternoon will be very important for Zillow, shareholders are relying on a solid report to help reverse the share price trend. Management will need to prove to the market that they have a strategy that can boost net profit margins and also drive user acquisition organically in order for the market to feel optimistic about Zillow.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.