Will The Fed’s Rate-Hike Plans Eventually Trigger A Recession?

The Financial Times observes that the Federal Reserve’s forecast for higher interest rates in the next several years is accompanied by expectations of slower economic growth and rising unemployment. Given the tendency for US recessions to coincide or closely follow periods of tighter monetary policy, it’s hard to ignore the potential for trouble down the road.

Citing this week’s revised Fed forecasts, the FT notes:

Seven current members of the FOMC want the policy rate to be above 2.75 per cent by the end of 2019 — and five want it to be above 3 per cent. Only one person thinks the “longer run” rate is above 3 per cent. That means at least five out of the maximum of 19 policymakers want the Fed to be actively slowing the US economy by the end of 2019.

Using these predictions as a guide suggests that “America’s central bank is determined to tighten monetary policy sufficiently to slow growth and raise unemployment. The aim is to prevent inflation from accelerating from its current quiescent pace.”

The question is whether the Fed is on track to once again satisfy a phenomenon that the economist Rodi Dornbusch described as macro homicide: “none of the US expansions of the past 40 years died in bed of old age; every one was murdered by the Federal Reserve.”

If and when the Treasury yield curve inverts – short rates rise above long rates – history suggests that the odds are elevated that a new recession is near, as a number of studies have pointed out, including this analysis by the New York Fed.

The good news is that the yield curve is still positive. For instance, the benchmark 10-year Treasury yield currently commands a premium of 123 basis points over the 3-month T-bill, as of Sep. 21. That’s down from nearly a 200-basis-point premium at the start of the year, but for the moment this business-cycle indicator remains in positive terrain, if only modestly.

Still, the downward bias appears to be intact, and given the latest Fed forecasts it’s reasonable to wonder if we’ll see further compression of the yield curve in the weeks and months ahead. If so, will that constitute a new recession signal?

Some analysts have questioned the value of the Treasury yield curve in an age of extraordinary monetary policy via quantitative easing. As Bloomberg points out today:

Years of unconventional monetary accommodation have led to many market distortions, one of which has been the disappearing term premium, which measures the extra compensation investors need to own long-term bonds instead of continuously rolling over short-term debt. By guaranteeing unprecedented levels of liquidity through its asset purchases, the so-called Fed put has taken risk out of the system and the term premium along with it.

The implication: Treasury yield spreads are no longer a reliable indicator for monitoring business-cycle risk. Perhaps, although the jury’s still out until we can review the hard numbers on the other side of the next downturn.

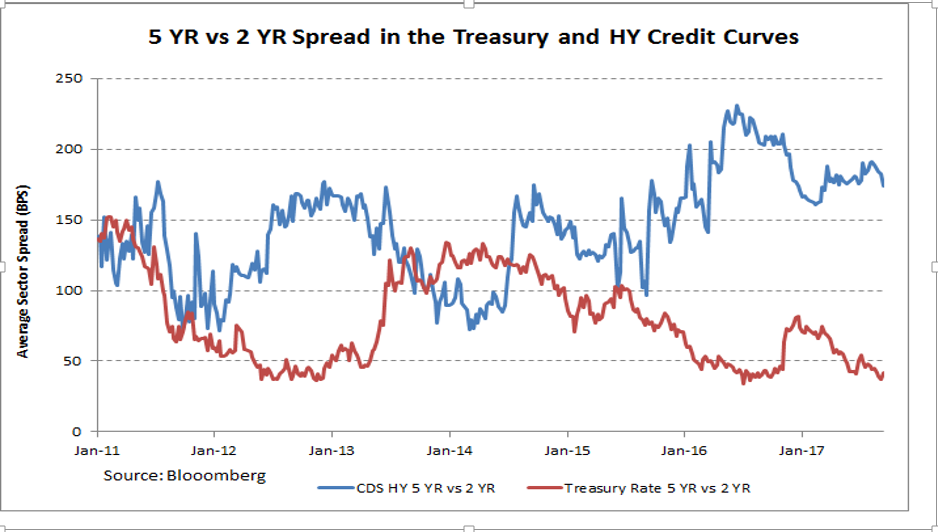

Meantime, Bloomberg advises that high-yield credit markets offer a clearer picture of the macro trend. “A much truer assessment of the threat of a slowdown can be gleaned from the high-yield credit curve, where the impact of central bank policy is much less pronounced.” By that standard, current conditions still look favorable: “yield curves are steep in credit markets and showing no signs of flattening or inverting,” based on five-year high-yield credit default swaps less their two-year counterparts.

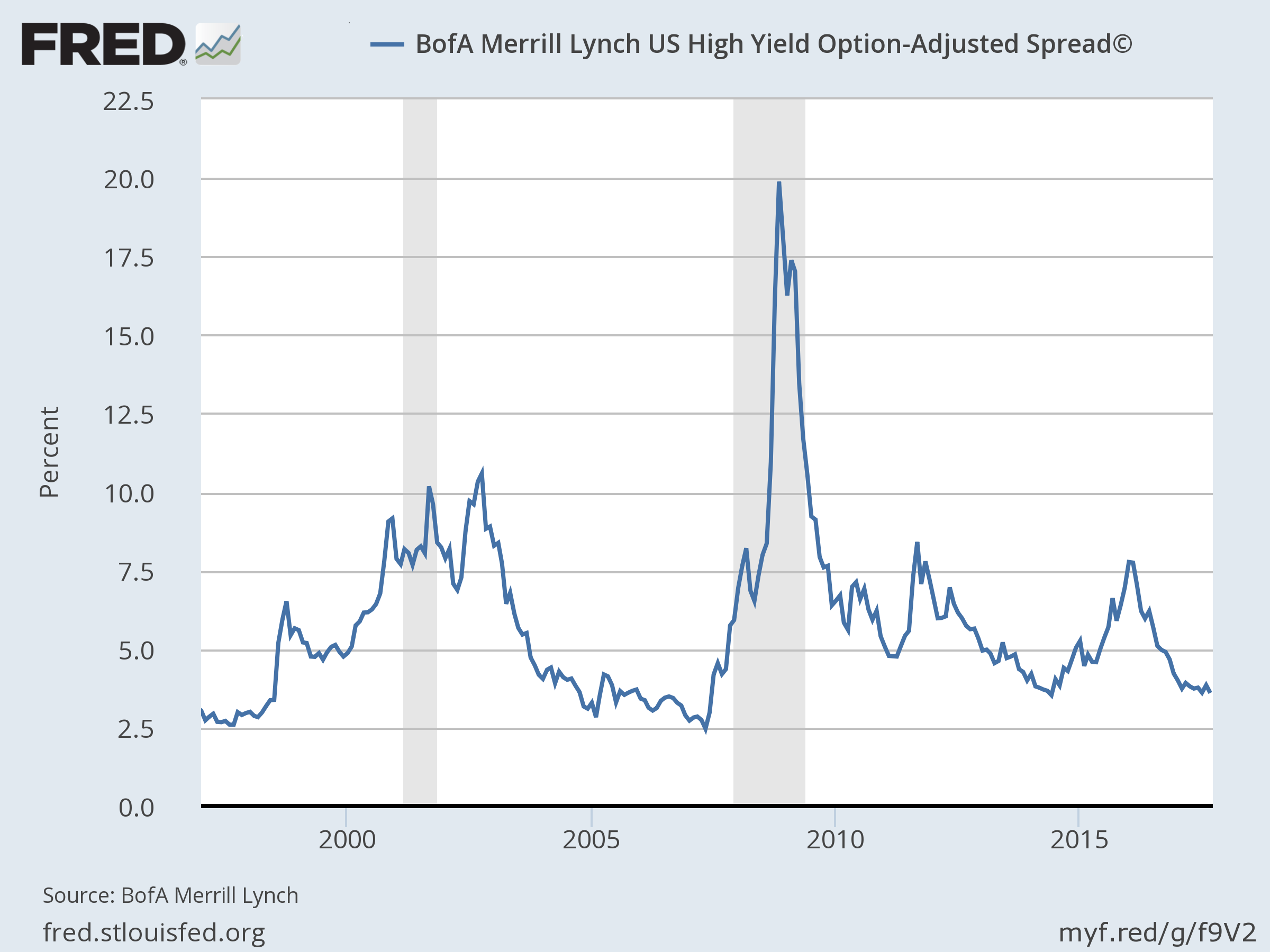

In fact, the case for using the high-yield market as an alternative measure of business-cycle risk is old news. A 2000 working paper from the National Bureau of Economic Research, for instance, notes that “the high yield spread has had significant explanatory power for the business cycle.” Not surprisingly, the BofA Merrill Lynch US High Yield Option-Adjusted Spread has shown an upward bias in the last two downturns.

Deciding which spread will be more valuable as a business-cycle indicator in the months and years ahead, however, is a mug’s game. A careful review of a broad set of indicators reveals that the value of any one data set waxes and wanes for analyzing recession risk. The empirical record inspires using a diversified set of signals beyond interest rates and financial markets to monitor the macro profile — a framework that’s applied in The Capital Spectator’s monthly economic reviews and the weekly updates in The US Business Cycle Risk Report.

This much is clear: there’s always another downturn lurking in the future, an event that’s likely to be accompanied by considerable investment risk. Accordingly, monitoring the business cycle should be a key part of a risk-management process.

Fortunately, there’s a wide mix of relevant factors for nowcasting this risk (forecasting, by contrast, tends to be counterproductive). Cherry-picking one or two indicators may be tempting, but it’s also risky since it’s never clear when a data set that’s been reliable in the past will stop working. The solution: avoid putting all your eggs in one basket. That’s solid advice for investing and it’s equally practical for evaluating recession risk.

Disclosure: None.