Why Oil Prices Can’t Bounce Very High; Expect Deflation Instead

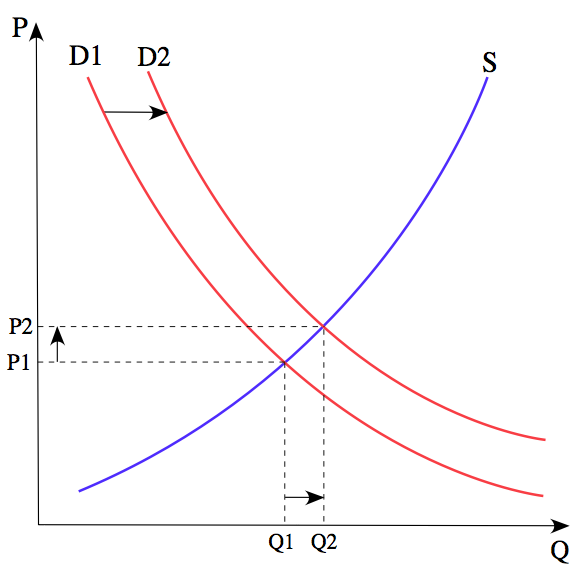

Economists have given us a model of how prices and quantities of goods are supposed to interact.

(Click on image to enlarge)

Unfortunately, this model is woefully inadequate. It sort of works, until it doesn’t. If there is too little a product, higher prices and substitution are supposed to fix the problem. If there is too much, prices are supposed to fall, causing the higher-priced producers to drop out of the system.

This model doesn’t work with oil. If prices drop, as they have done since mid-2014, businesses don’t drop out. They often try to pump more. The plan is to try to make up for inadequate prices by increasing the volume of extraction. Of course, this doesn’t fix the problem. The hidden assumption is, of course, that eventually oil prices will again rise. When this happens, the expectation is that oil businesses will be able to make adequate profits. It is hoped that the system can again continue as in the past, perhaps at a lower volume of oil extraction, but with higher oil prices.

I doubt that this is what really will happen. Let me explain some of the issues involved.

[1] The economy is really a much more interlinked system than Figure 1 makes it appear.

Supply and demand for oil, and for many other products, are interlinked. If there is too little oil, the theory is that oil prices should rise, to encourage more production. But if there is too little oil, some would-be workers will be without jobs. For example, truck drivers may be without jobs, if there is no fuel for the vehicles they drive. Furthermore, some goods will not be delivered to their desired locations, leading to a loss of even more jobs (both at the manufacturing end of the goods, and at the sales end).

Ultimately, a lack of oil can be expected to reduce the availability of jobs that pay well. Digging in the ground with a stick to grow food is a job that is always around, with or without supplemental energy, but it doesn’t pay well!

Thus, the lack of oil really has a two-way pull:

(a) Higher prices, because of the shortage of oil and the desired products it produces.

(b) Lower prices, because of a shortage of jobs that pay adequate wages and the “demand” (really affordability) that these jobs produce.

[2] There are other ways that the two-way pull on prices can be seen:

(a) Prices need to be high enough for oil producers, or they will eventually stop extracting and refining the oil, and,

(b) Prices cannot be too high for consumers, or they will stop buying products made with oil.

If we think about it, the prices of basic commodities, such as food and fuel cannot rise too high relative to the wages of ordinary (also called “non-elite”) workers, or the system will grind to a halt. For example, if non-elite workers are at one point spending half of their income on food, the price of food cannot double. If it does, these workers will have no money left to pay for housing, or for clothing and taxes.

[3] The upward pull on oil prices comes from a combination of three factors.

(a) Rising cost of production, because the cheapest-to-produce oil tends to be extracted first, leaving the more expensive-to-extract oil for later. (This pattern is also true for other types of resources.)

(b) If workers are becoming more productive, this growing productivity of workers is often reflected in higher wages for the workers. With these higher wages, workers can afford more goods made with oil, and that use oil in their operation. Thus, these higher wages lead to higher “demand” (really affordability) for oil.

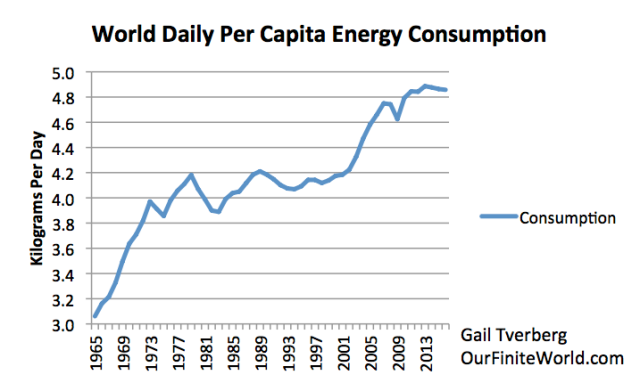

Recently, worker productivity has not been growing. One reason this is not surprising is because energy consumption per capita hit a peak in 2013. With less energy consumption per capita, it is likely that, on average, workers are not being given bigger and better “tools” (such as trucks, earth-moving equipment, and other machines) with which to leverage their labor. Such tools require the use of energy products, both when they are manufactured and when they are operated.

(Click on image to enlarge)

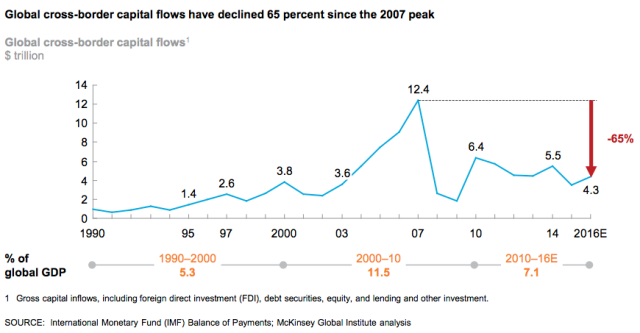

(c) Another “pull” on demand comes from increased investment. This investment can be debt-based or can reflect equity investment. It is these financial assets that allow new mines to be opened, and new factories to be built. Thus, wages of non-elite workers can grow. McKinsey Global Institute reports that growth in total “financial assets” has slowed since 2007.

(Click on image to enlarge)

More recent data by McKinsey Global Institute shows that cross-border investment, in particular, has slowed since 2007.

(Click on image to enlarge)

This cross-border investment is especially helpful in encouraging exports, because it often puts into place new facilities that encourage extraction of minerals. Some minerals are available in only in a few places in the world; these minerals are often traded internationally.

[4] The downward pull on oil and other commodity prices comes from several sources.

(a) Oil exports are often essential to the countries where they are extracted because of the tax revenue and jobs that they produce. The actual cost of extraction may be quite low, making extraction feasible, even at very low prices. Because of the need for tax revenue and jobs, governments will often encourage production regardless of price, so that the country can maintain its place in the world export market until prices again rise.

(b) Everyone “knows” that oil and other commodities will be needed in the years ahead. Because of this, there is no point in stopping production all together. In fact, the cost of production is likely to keep rising, putting an upward push on commodity prices. This belief encourages businesses to stay in the market, regardless of the economics.

(c) There is a long lead-time for developing new extraction capabilities. Decisions made today may affect extraction ten years from now. No one knows what the oil price will be when the new production is brought online. At the same time, new production is coming on-line today, based on analyses when prices were much higher than they are today. Furthermore, once all of the development costs have been put in place, there is no point in simply walking away from the investment.

(d) Storage capacity is limited. Production and needed supply must balance exactly. If there is more than a tiny amount of oversupply, prices tend to plunge.

(e) The necessary price varies greatly, depending where geographically the extraction is being done, and depending on what is included in the calculation. Cost are much lower if the calculation is done excluding investment to date, or excluding taxes paid to governments, or excluding necessary investments needed for pollution control. It is often easy to justify accepting a low price, because there is usually some cost basis upon which such a low price is acceptable.

(f) Over time, there really are efficiency gains, but it is difficult to measure how well they are working. Do these “efficiency gains” simply speed up production a bit, or they allow more oil in total to be extracted? Also, cost cuts by contractors tend to look like efficiency gains. In fact, they may simply be temporary prices cuts, reflecting the desire of suppliers to maintain some market share in a time when prices are too low for everyone.

(g) Literally, every economy in the world wants to grow. If every economy tries to grow at the same time and the market is already saturated (given the spending power of non-elite workers), a very likely outcome is plunging prices.

[5] As we look around the world, the prices of many commodities, including oil, have fallen in recent years.

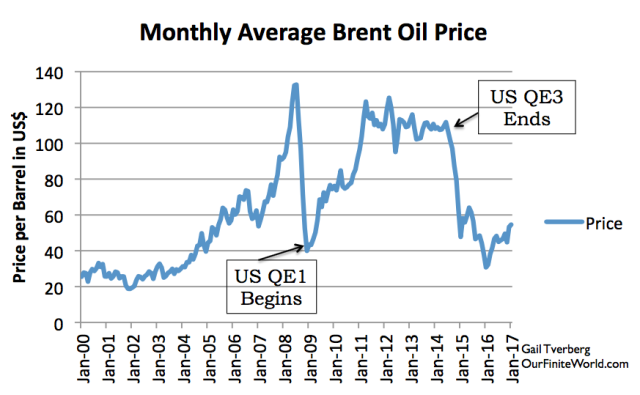

Figures 3 and 4 show that investment spending spiked in 2007. Oil prices spiked not long after that–in the first half of 2008.

(Click on image to enlarge)

Quantitative Easing (QE) is a way of encouraging investment through artificially low interest rates. US QE began right about when oil prices were lowest. We can see that the big 2008 spike and drop in prices corresponds roughly to the rise and drop in investment in Figures 3 and 4, above, as well.

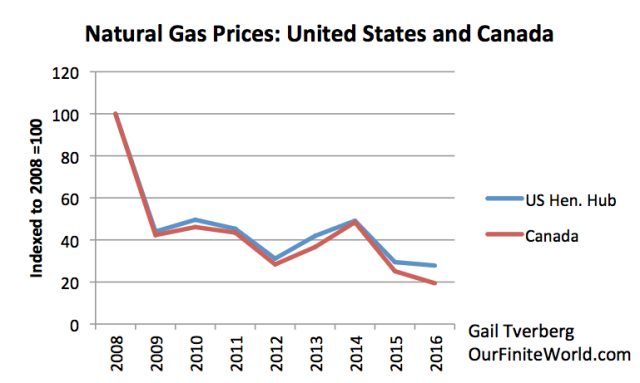

If we look at commodities other than oil, we often see a major downslide in prices in recent years. The timing of this downslide varies. In the US, natural gas prices fell as soon as gas from fracking became available, and there started to be a gas oversupply problem.

I expect that at least part of gas’s low price problem also comes from subsidized prices for wind and solar. These subsidies lead to artificially low prices for wholesale electricity. Since electricity is a major use for natural gas, low wholesale prices for electricity indirectly tend to pull natural gas prices down.

(Click on image to enlarge)

Many people assume that fracking can be done so inexpensively that the type of downslide in prices shown in Figure 6 makes sense. In fact, the low prices available for natural gas are part of what have been pushing North American “oil and gas” companies toward bankruptcy.

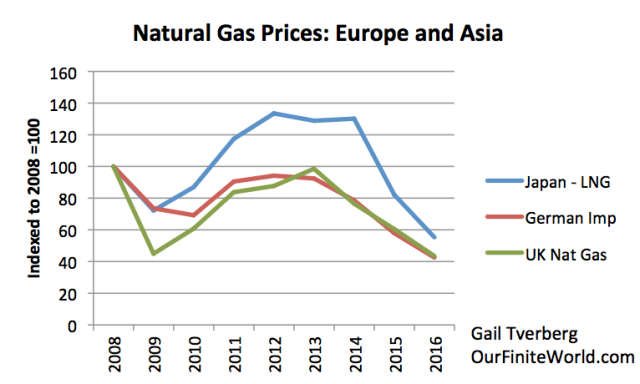

For a while, it looked like high natural gas prices in Europe and Asia might allow the US to export natural gas as LNG, and end its oversupply problem. Unfortunately, overseas prices of natural gas have slid since 2013, making the profitability of such exports doubtful (Figure 7).

(Click on image to enlarge)

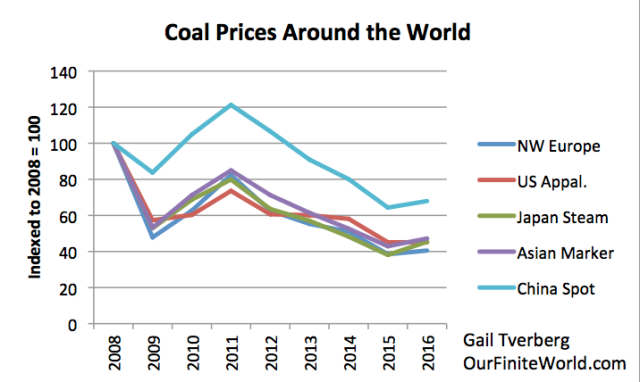

Coal prices have followed a downward slope of a different shape since 2008. Note that the 2016 prices range from 32% to 59% below the 2008 level. They are even lower, relative to 2011 prices.

(Click on image to enlarge)

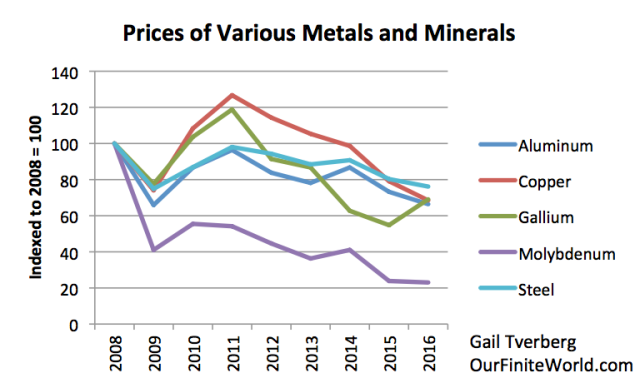

Figure 9 shows the price path for several metals and minerals. These seem to follow a downward path as well. I did not find a price index for rare earth minerals that went back to 2008. Recent data suggested that the prices of these minerals have been falling as well.

(Click on image to enlarge)

Figure 9 shows that several major metals are down between 24% and 35% since 2008. The drop is even greater, relative to 2011 price levels.

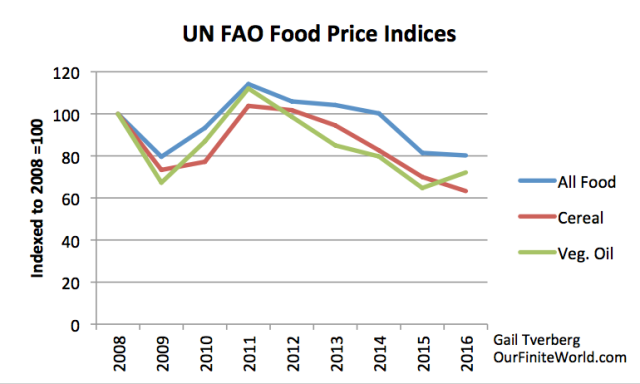

Internationally traded foods have also fallen in price since 2008.

(Click on image to enlarge)

In Item [4] above, I listed several factors that would tend to make oil prices fall. These same issues could be expected to cause the prices of these other commodities to drop. In addition, energy products are used in the production of metals and minerals and of foods. A drop in the price of energy products would tend to flow through to lower extraction prices for minerals, and lower costs for growing agricultural products and bringing products to market.

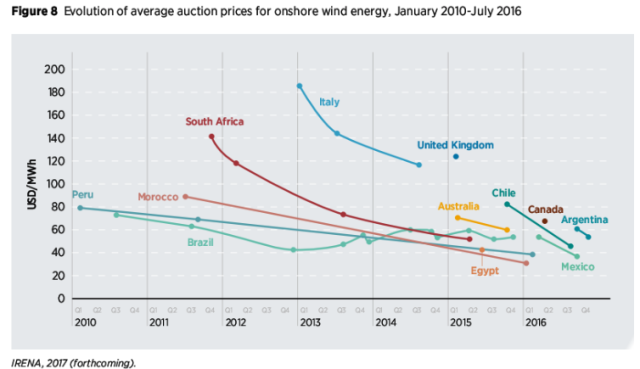

One surprising place where prices are dropping is in the auction prices for the output of onshore wind turbines. This is a chart shown by Roger Andrews, in a recent article on Energy Matters. The cost of making wind turbines doesn’t seem to be dropping dramatically, except from the fall in the prices of commodities used to make the turbines. Yet auction prices seem to be dropping by 20% or more per year.

(Click on image to enlarge)

Thus, wind energy purchased through auctions seems to be succumbing to the same deflationary market forces as oil, natural gas, coal, many metals, and food.

[6] It is very hard to see how oil prices can rise significantly, without the prices of many other commodities also rising.

What seems to be happening is a basic mismatch between (a) the amount of goods and services countries want to sell, and (b) the amount of goods and services that are truly affordable by consumers, especially those who are non-elite workers. Somehow, we need to fix this supply/demand (affordability) imbalance.

One way of raising demand is through productivity growth. As mentioned previously, such a rise in productivity growth hasn’t been happening in recent years. Given the falling energy per capita amounts in Figure 2, it seems unlikely that productivity will be growing in the near future, because the adoption of improved technology requires energy consumption.

Another way of raising demand is through wage increases, over and above what would be indicated by productivity growth. With globalization, the trend has been has been lower and less stable wages, especially for less educated workers. This is precisely the opposite direction of the change we need, if demand for goods and services is to rise high enough to prevent deflation in commodity prices. There are very many of these non-elite workers. If their wages are low, this tends to reduce demand for homes, cars, motorcycles, and the many other goods that depend on wages of workers in the world. It is the manufacturing and use of these goods that influences demand for commodities.

Another way of increasing demand is through rising investment. This can eventually filter back to higher wages, as well. But this isn’t happening either. In fact, Figures 3 and 4 show that the last big surge in investment was in 2007. Furthermore, the amount of debt growth to increase GDP by one percentage points has increased dramatically in recent years, both in the United States and China, making this approach to economic growth increasingly less effective. Recent discussions seem to be in the direction of stabilizing or lowering debt levels, rather than raising them. Such changes would tend to lower new investment, not raise it.

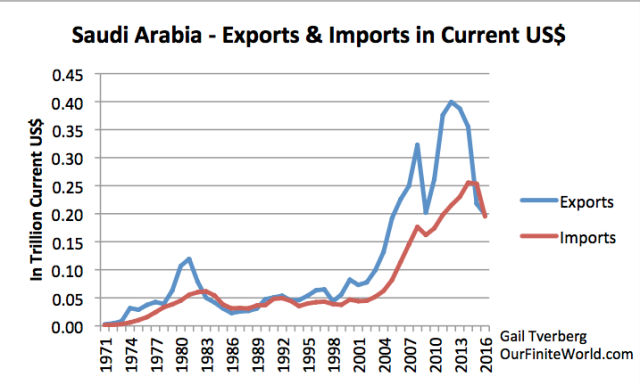

[7] In many countries, falling export revenue is adversely affecting demand for imported goods and services.

It is not too surprising that the export revenue of Saudi Arabia has fallen, with the drop in oil prices.

(Click on image to enlarge)

Because of the drop in exports, Saudi Arabia is now buying fewer imported goods and services. A person would expect other oil exporters also to be making cutbacks on their purchases of imported goods and services. (Exports in current US$ means exports measured year-by-year in US$, without any inflation adjustment.)

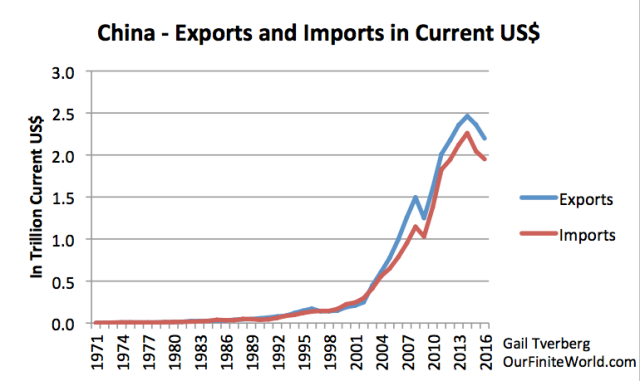

It is somewhat more surprising that China’s exports and imports are falling, as measured in US$. Figure 13 shows that, in US dollar terms, China’s exports of goods and services fell in both 2015 and 2016. The imports that China bought also fell, in both of these years.

(Click on image to enlarge)

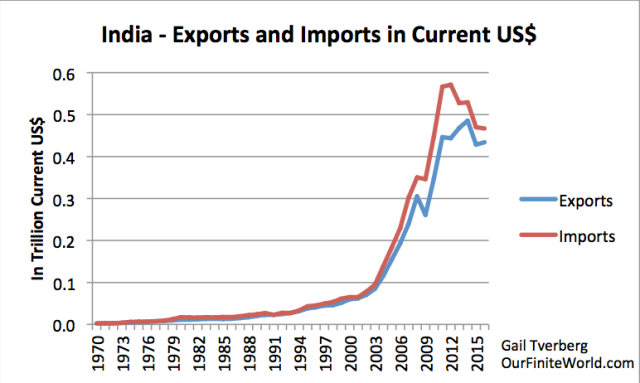

Similarly, both the exports and imports of India are down as well. In fact, India’s imports have fallen more than its exports, and for a longer period–since 2012.

(Click on image to enlarge)

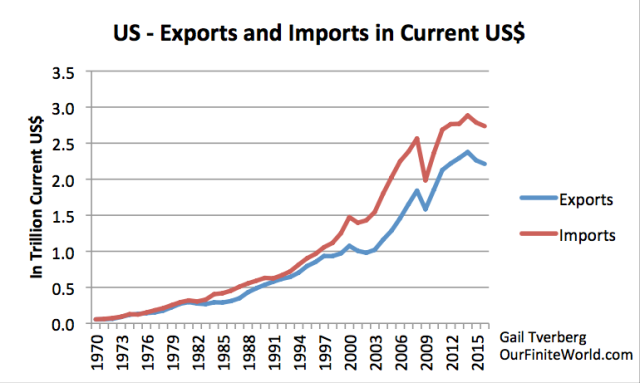

The imports of goods and services for the United States also fell in 2015 and 2016. The US is both an exporter of commodities (particularly food and refined petroleum products) and an importer of crude oil, so this is not surprising.

(Click on image to enlarge)

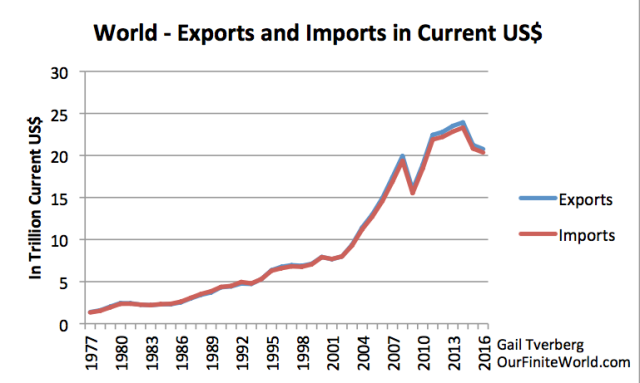

In fact, on a world basis, exports and imports of goods and services both fell, in 2015 and 2016 as measured in US dollars.

(Click on image to enlarge)

[8] Once export (and import) revenues are down, it becomes increasingly difficult to raise prices again.

If a country is not selling much of its own exports, it becomes very difficult to buy much of anyone else’s exports. This impetus, by itself, tends to keep prices of commodities, including oil, down.

Furthermore, it becomes more difficult to repay debt, especially debt that is in a currency that has appreciated. This means that borrowing additional debt becomes less and less feasible, as well. Thus, new investment becomes more difficult. This further tends to keep prices down. In fact, it tends to make prices fall, since new investment is needed to keep prices level.

[9] World financial leaders in developed countries do not understand what is happening, because they have written off commodities as “unimportant” and “something that lesser-developed countries deal with.”

In the US, few consumers are concerned about the price of corn. Instead, they are interested in the price of a box of corn flakes, or the price of corn tortillas in a restaurant.

The US, Europe and Japan specialize in high “value added” goods and services. For example, in the case of a box of cornflakes, manufacturers are involved in many steps such as (a) making cornflakes from corn, (b) boxing cornflakes in attractive boxes, (c) delivering those boxes to grocers’ shelves, and (d) advertising those cornflakes to prospective consumers. These costs generally do not decrease, as commodity prices decrease. One article from 2009 says, “With the record seven-dollar corn this summer, the cost of the corn in an 18-ounce box of corn flakes was only 14 cents.”

Because of the small role that commodity prices seem to play in producing the goods and services of developed countries, it is easy for financial leaders to overlook price indications at the commodity level. (Data available at this level of detail; the question is how closely it is examined by decision-makers.)

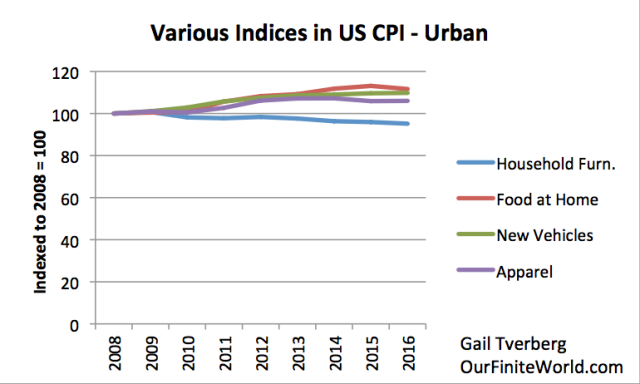

(Click on image to enlarge)

Figure 17 shows some components of the Consumer Price Index (CPI) on a basis similar to the trends in commodity prices shown in Figures 7 though 11. The category “Household furnishings and operations,” was chosen because it has furniture in it, and I know that furniture prices have fallen because of the growing use of cheap imported furniture from China. This category shows a slight downslope in prices. The other categories all show small increases over time. If commodity prices had not decreased, prices of the other categories would likely have increased to a greater extent than they did during the period shown.

[10] Conclusion. We are likely kidding ourselves, if we think that oil prices can rise in the future, for very long, by a very large amount.

It is quite possible that oil prices will bounce back up to $80 or even $100 per barrel, for a short time. But if they rise very high, for very long, there will be adverse impacts on other segments of the economy. We can’t expect that wages will go up at the same time, so increases in oil prices are likely to lead to a decrease in the purchase of discretionary products such as meals eaten in restaurants, charitable contributions, and vacation travel. These cutbacks, in turn, can be expected to lead to layoffs in discretionary sectors. Laid off workers are likely to have difficulty repaying their loans. As a result, we are likely to head back into a recession.

As we have seen above, it is not only oil prices that need to rise; it is many other prices that need to rise as well. Making a change of this magnitude is almost certainly impossible, without “crashing” the economy.

Economists put together a simplified view of how they thought supply and demand works. This simple model seems to work, at least reasonably well, when we are away from limits. What economists did not realize is that the limits we are facing are really affordability limits, and that growing affordability depends upon productivity growth. Productivity growth in turn depends on a growing quantity of cheap-to-produce energy supplies. The term “demand,” and the two-dimensional supply-demand model hide these issues.

The whole issue of limits has not been well understood. Peak Oil enthusiasts assumed that we were “running out” of an essential energy product. When this view was combined with the economist’s view of supply and demand, the conclusion was, “Of course, oil prices will rise, to fix the situation.”

Few stopped to realize that there is a second way of viewing the situation. What is falling is the resources that people need to have in order to have jobs that pay well. When this happens, we should expect prices to fall, rather than to rise, because workers are increasingly unable to buy the output of the economy.

If we look back at what happened historically, there have been many situations in which economies have collapsed. In fact, this is probably what we should expect as we approach limits, rather than expecting high oil prices. If collapse should take place, we should expect widespread debt defaults and major problems with the financial system. Governments are likely to have trouble collecting enough taxes, and may ultimately fail. Non-elite workers have historically come out badly in collapses. With low wages and high taxes, they have often succumbed to epidemics. We have our own epidemic now–the opioid epidemic.

Disclosure: None.