Why It Is Important To Watch Long Term Rates As Central Banks Hike Short Term Rates

Yield curve flattening is not new to bond investors, yet it seems to have generated a lot of attention as the Fed pursues its goal of normalizing the Fed funds rate. The theory is that when the Fed starts hiking the Fed funds rate, long-term rates would move up accordingly and the entire yield curve would shift in a positive upward direction. Thus, the spread between the yields would remain unchanged.

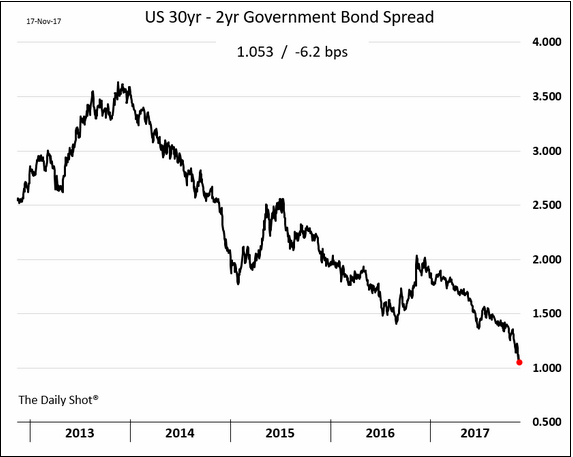

Stubbornly, long-term rates have not behaved according to that script. The spread between the 30yr and 2yr bond yields has narrowed dramatically. Starting at 125bps at the beginning of this year, the spread has been compressed to just 61 basis points. We have not experience a spread less than 100bps since 2007. More importantly, the speed with which the spread narrows should set off some alarm bells regarding the economic outlook. This spread compression is taking place at a time when the Fed has made it clear that it will pursue a tightening policy well into 2018.

Fed watchers cannot help but take notice of these developments in the long end of the bond market. They wonder if the Fed will overshoot and engineer a serious slowdown or even recession. That is what is implied by this flattening. While it is not certain that a recession is on the horizon, the curve flattening does suggest that growth will be subdued and that inflation will remain well contained, most likely below the target rate of 2%. This is not what the Fed had in mind when it signaled that rates needed to be “normalized”.

The Fed is not the only central bank to be concerned about the path of long-term rates. Governor Poloz of the Bank of Canada let it be known that one of the variables that will influence future monetary policy will be the behavior of long rates in Canada. And, true to form, there has been considerable yield curve flattening in Canada as the short end yield has moved up dramatically while the longer end has drifted down. Since the beginning of the year, the yield on the Canadian 30yr-2yr spread has narrowed from 155 bps to 83bps.

What is behind the yield curve flattening?

Long-term interest rates can be segmented into three components. First, there is the expected path of short-term interest rates; the long rate can be viewed as a yearly succession of short-term rates. If the long end falls, then this puts a ceiling on how much the central bank can raise short rates for fear that the curve will invert. Inversion is a sure sign of impending recession. Second, long rates are heavily impacted by the expected inflation rates over the life of the bond. With the 30yr US Treasury at 2.75%, bondholders anticipate that inflation will average less than 2% over that period. They feel that the yield provides adequate protection against future inflation. Finally, there is the “term premium” which is often considered to be that additional amount of interest needed to entice investors to hold the bond to full term.

Narrowing spreads mean that bankers have very limited room in which to raise short-term rates. If short-term rates were to increase to the point in which the yield actually inverts--- long rates are lower than short rates--- then this would raise the red flag of recession. For the moment, the curve remains upward sloping, but the recent flattening trend cannot be ignored in setting monetary policy.

Disclosure: None.