Why Focus On Risk? Because It’s Good For You

My end of the year newsletter generated the following comment at Seeking Alpha:

“I look at last year’s numbers and I feel all warm and content. I read articles like this and all that comfort disappears like it was never there. Reading this author is like taking your medicine, it’s good for your investing prowess, but it sure is not much fun. I guess folks find it bracing to write such things, ‘It’s for your own good.’ Ugh.The sad thing is that is likely a reasonable forewarning of disaster to come. Shoot the messenger, I say, let me bask in the sun of my success to date. Tomorrow we die, don’t you know, eat drink and be merry. It is good until it is no more.”

He’s right.

It’s the same thing as having to pass on a big, juicy hamburger and opt for the salad with low-fat dressing. It is not nearly as satisfying, but we do it because we don’t want to die from cardiac arrest.

The same thing with “working out.”We trudge to the gym to grind away on a stair-climber so we don’t drop dead from a heart attack. (Maybe, if they called it something more fun sounding, like “sex prepping,” people might be more inclined to actually do it.)

But when it comes to the investment world, doing something for the “health and welfare” of your portfolio, especially when regard for risk is at historic lows, is a “buzzkill.”

Hey, I get it.

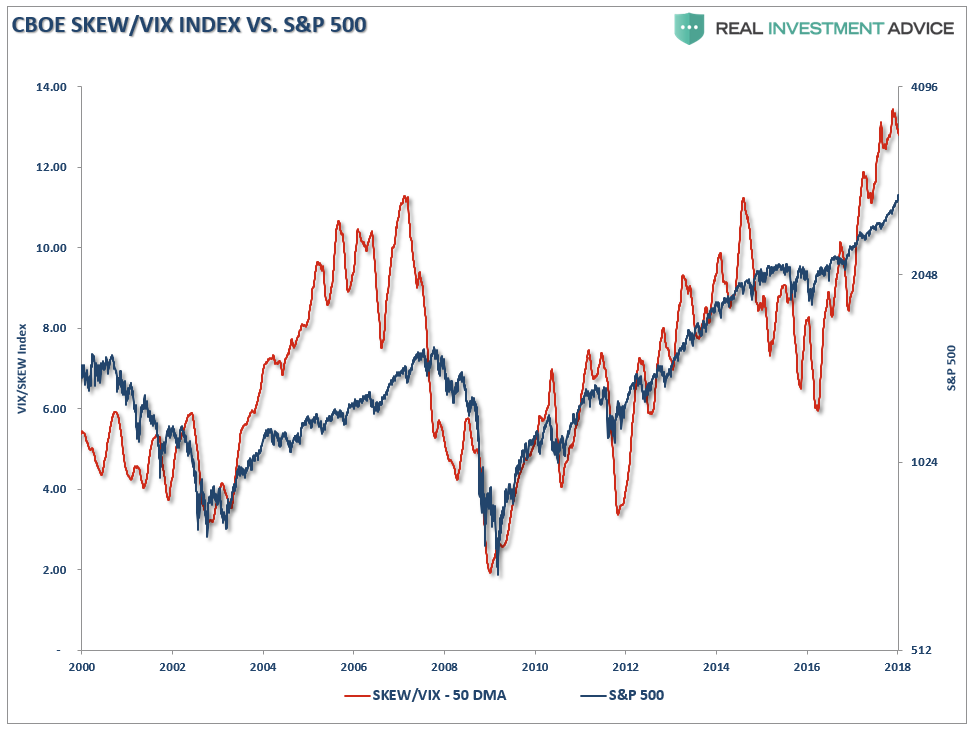

In fact, right now, the view of hedging a portfolio is virtually non-existent. The chart below is the 50-dma of the CBOE SKEW Index (which is derived from the price of S&P 500 tail risk and is calculated from the prices of S&P 500 out-of-the-money options) divided by the volatility index (VIX).

(Click on image to enlarge)

With the “lack of fear” index at near record highs, who wants to hear about why things may not stay that way?

But, isn’t this exactly the reason that we SHOULD be worrying about what comes next?

We diet, exercise and do all things we hate to try and live a healthier life. We buy life insurance to hedge off the risk of dying too soon. Yet, we don’t want to give the same concern toward the “health” of the one thing we are going to be MOST dependent upon in retirement – OUR SAVINGS.

This is why my missives most often discuss the “risk” of what could go wrong with the market and your money.

No one wants to hear their doctor tell them to stop eating all that delicious fattening food. Nor do they want some fitness guru telling them they need to get to the gym. However, when the diagnosis is dire enough, it is the push needed for us to focus on what is important.

Of course, in the investment world, since such a view is considered “bearish,” it is immediately assumed that I am all in cash and have been sitting idly on the sidelines awaiting the next crash.

That is simply not the case.

In fact, in each weekly missive, I make a conscious effort to reinforce the fact that we are remain fully allocated in portfolios currently. I also discuss what we are doing within our client-centric portfolios. As noted this past weekend:

“As I noted last week, we did add some defensive positions to our portfolio allocations while we still retain a fully allocated long-position as well. These defensive ‘shock absorbers’ are simply in place to reduce a volatility shock when, not if, one occurs.”

(Click on image to enlarge)

“Again, our portfolios remain on the long-side for now. However, as I will discuss below, we are also starting to add hedges and looking for additional opportunities to de-risk portfolios as prices continue their exuberant press higher.”

Here is the point.

I could easily become a “market cheerleader.”

But there are already a multitude of those from the mainstream media to Wall Street.

Since I am already fully allocated to markets in our models, focusing on reasons why the markets will continue to rise seems a bit redundant to me.

What is more important to me, and the basis from which I write, is what potentially could take a large chunk of capital away from our clients. For us, capital preservation is the key to winning the long-term investment game.

Take a look at the chart above.

The markets have ONLY been this extended, overbought and exuberant a few times throughout history. The subsequent outcomes for investors have never been good and, in some instances, have been downright disastrous.

Could this time be different?

No.

It is only a function of timing as to when something triggers a mean-reverting event. However, it could be 6-months or 2-years before such an event occurs.

It will, but, as the saying goes, “timing is everything.”

So, I apologize if I seem to be a “Schleprock,” but as I have written many times in the past:

“I am not bullish or bearish. My job as a portfolio manager is simple; invest money in a manner that creates returns on a short-term basis but reduces the possibility of catastrophic losses which wipe out years of growth.

In the end, it does not matter IF you are ‘bullish’ or ‘bearish.’ The reality is that both ‘bulls’ and ‘bears’ are owned by the ‘broken clock’ syndrome during the full-market cycle. However, what is grossly important in achieving long-term investment success is not necessarily being ‘right’ during the first half of the cycle, but not being ‘wrong’ during the second half.”

No Excuses

My hope, through my writings, is that you have been sufficiently warned.

It may not be today, next month, or even next year.

“Bull markets are built on optimism and die on exuberance.”

But they all die. Simply ignoring history won’t make the damage any less catastrophic.

Of course, given that investors are just “mere mortals” and do not have an infinite amount of time to reach their financial goals, the ends of bull market cycles matter, and they matter a great deal.

While “perma-bulls” may enjoy taking stabs at portfolio managers who take their risk management and capital preservation responsibilities very seriously, it should be done without taking those comments out of context.

Have I warned of risks in the markets?

Absolutely.

Does that mean I have somehow been sitting in “cash” this whole time and “missing out?”

Absolutely Not.

We are all trying to predict the future. No one will ever be right all the time.

I have more than once in my career written a “mea culpa,” and I am sure that I will write many more before I am finished with this business.

But here is my point.

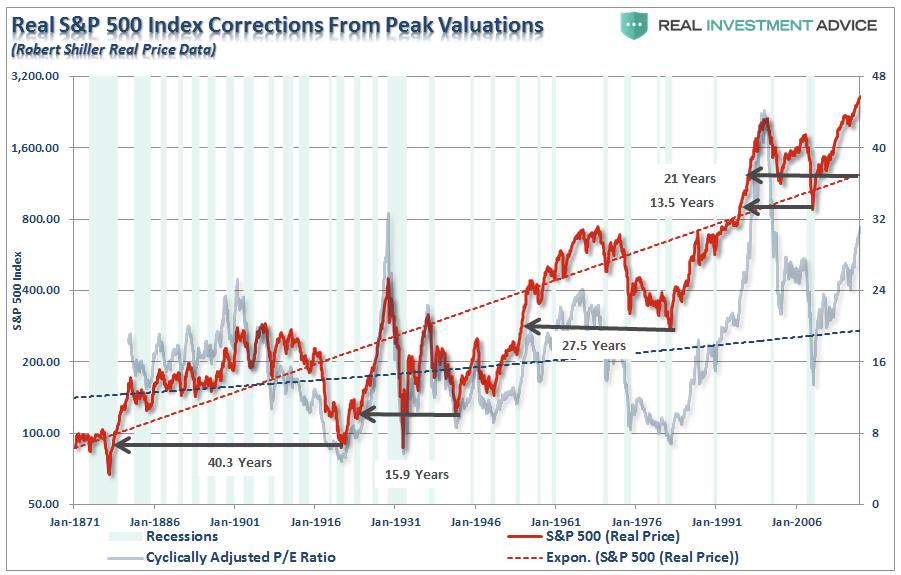

The chart below brings this idea of reversion into a bit clearer focus. I have overlaid the real, inflation-adjusted, S&P 500 index over the cyclically-adjusted P/E ratio.

(Click on image to enlarge)

Historically, we find that when both valuations and prices have extended well beyond their intrinsic long-term trendlines, subsequent reversions BEYOND those trend lines have ensued.

Every Single Time.

Importantly, these reversions have wiped out a decade, or more, in investor gains. As noted, if the next correction begins in 2018 and ONLY reverts back to the long-term trendline, which historically has never been the case, investors would reset portfolios back to levels not seen since 1997.

Two decades of gains lost…again.

A Prescription For Portfolio Health

With valuations elevated, the economic cycle very long in the tooth, and the 3-Ds applying downward pressure to future economic growth rates, there is a valid reason to consider the following:

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerate the principal bleed. Plans should be made during rising market years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years and the low interest rate environment have created an extremely risky situation for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean that you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk than you most likely want, or can afford. Two massive bear markets over the last decade have left many individuals further away from retirement goals than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to reach their retirement goals.

Oh, and while you’re at it, it’s probably time to call the doctor for that annual physical.

I can already hear the latex gloves popping.

Just remember, you have been sufficiently warned.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

Indeed, the key is asset preservation and then returns. It is often said often but rarely followed through. Rather than getting out of the market, or buying puts, asset rotation to safer but less exuberant stocks that pay sustainable dividends is a wise move as the cycle continues. One should focus on cash flows and look at the balance sheet to consider stocks from now on.