USDCNY - It's Going To 7, Folk

Here's a couple of charts on a topical and divisive subject - the outlook for the Chinese yuan. This is something I've spent a lot of time looking at, and have been bearish Renminbi vs US dollar for a few good reasons. Before we look at the charts let's talk about why. It's basically 3 reasons, and it's mostly about the fundamentals: 1. Economic divergence (China's economy is slowing vs US accelerating); 2. Policy divergence (Fed hiking rates + QT vs PBOC cutting RRR, easing liquidity); 3. Politics (CNY weakness provides a timely offset against tariffs, and eases domestic pressure).

1. Interest Rate Differentials: The first chart maps the USDCNY against monetary policy rate differentials. Interest rate differentials are a fairly well-established indicator for exchange rates because they reflect incentives e.g. borrowing in one currency (lower interest rate) and investing in the other (higher interest rate), and also reflect divergences in economic developments and monetary policy cycles. If you take this chart literally the USDCNY could end up going well beyond 7 ...on that note, this is basic economics, not competitive devaluation.

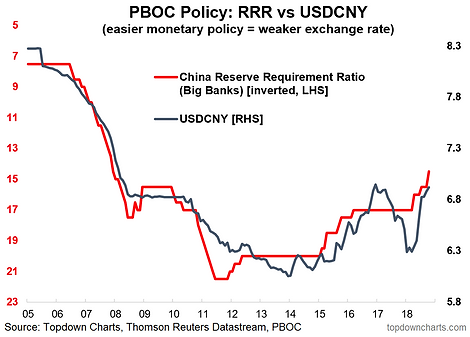

2. The RRR (and PBOC monetary policy in general): The other key chart is the RRR (reserve requirement ratio), shown here inverted against the USDCNY. There's a reasonable link here too, and again it's partly a reflection of broader monetary policy conditions, and partly a reflection of flows and liquidity. With China's economy under pressure as the short-term economic cycle turns down, odds are we could see more RRR cuts, and hence more pressure on the Renminbi.

3. The problem with all this: The big problem with a possible breach of the ominous 7.0 level (which is more about the fact that the exchange rate continues to move than the particular importance of a random round number), is the impact on global risk appetite and the inter-relation with US dollar demand. A further round of weakness in the Chinese yuan is likely to trigger more EMFX and Asian currency weakness, and hence strike risk sentiment and cause a spike in short-term demand for the US dollar - which obviously would exacerbate the issue.

And it's a key point too, because while a lot of what we've been talking about here has to do with China, when you're talking exchange rates it's all relative and there are 2 sides to the coin... a higher USDCNY will have just as much to do with a stronger US dollar as a weaker Renminbi.

So as global markets undergo a correction, if you're looking for a potential trigger for a further hit to risk appetites the potential for a weaker Chinese yuan is certainly up there.

For more and deeper insights on the global markets, good charts, and actionable investment ideas you may want to more