US Monetary And Fiscal Authorities Need To Get Their Acts Together

A Fed that is determined (for now) to raise the Fed funds rate is driving up the US dollar and inflicting hardship on Emerging Markets…. Historically, Fed Chairs liked to consider the Fed being just the central bank for the US until things blew up globally. Powell is no exception. We could be witnessing a slow-moving train wreck”, William Chin, Caldwell Securities, June 2018

It now appears that the slow-moving train is moving much faster and already there is some debris on the track. Today, Turkey announced a reduction in the limits for Turkish banks to execute foreign currency swap transactions. The swap is a key component in the whole mechanism for a forward sale of the Turkish lira. Now short selling and capital flight are more difficult to execute. Should Turkey take the next step and impose full foreign exchange controls, investors will be rushing to the exits. Debris from this train wreck started to fall when the lira tumbled about 20%, almost overnight. Now, exchange restrictions just add to the pile of debris.

In a previous blog1, I outlined how the build-up towards the crisis in Turkey started with the Federal Reserve decision to flood the world’s financial markets with liquidity with quantitative easing. Dollars poured into emerging markets, especially countries such as Turkey, Brazil, Argentina, Indonesia and South Africa, to fund infrastructure projects and large-scale industrial projects. As long as U.S. interest rates remained close to zero, investors were only too delighted to receive higher yields overseas.

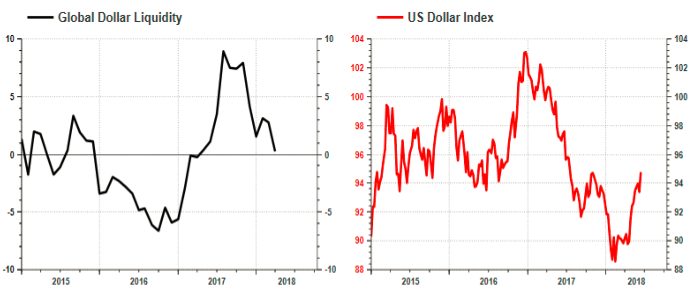

But now something has happened. The Fed is in a tightening mode and not only are short-term interest rates on the rise but more importantly, the Fed is shrinking its balance sheet which means that liquidity is tightening. As Fed-held US Treasuries mature, the Fed essentially withdraws liquidity from the financial system. This withdrawal is now been felt worldwide. Global liquidity is shrinking and that means the USD index is on the rise (Figure 1). The Fed should slow down the tapering of its balance sheet and also slow down its moves towards normalization. Both policies contribute to a higher dollar and that is damaging U.S trading interests and, more significantly, it is playing havoc with the currencies and debt levels in the emerging markets. Reports out of India indicate that the Governor of the Bank of India is pleading with the Fed to slow down its tapering activities because the rise in dollar is forcing investors to re-price foreign debt and pressuring the rupee.

Figure 1 Global Liquidity and the USD Index

(Click on image to enlarge)

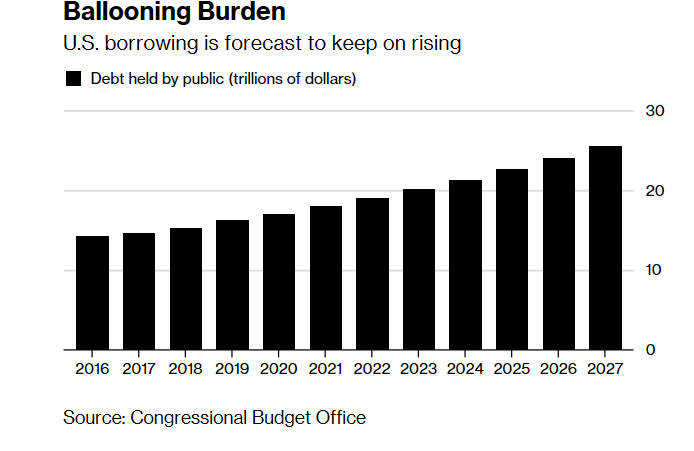

Turning to U.S. fiscal policy, the ballooning Fed debt is making this train wreck even worse (Figure 2). U.S.Federal deficits will exceed $1 trillion annually for each of the next five years or more. Since the United States is unable to fund its deficits from domestic savings, it must turn to foreign investors to absorb the bulk of the new debt issuances. As foreign central banks and major sovereign wealth funds participate in the purchase of U.S. debt, dollar liquidity is drained even further. Changing the course of U.S. government spending is virtually impossible at this stage. The relief for emerging markets is for the Federal Reserve to back down somewhat on its tightening stance.

Figure 2 US Borrowing Requirement