Unhinged And Unrepentant - The Central Bankers' Demolition Squad

We are still doubled over with laughter about this one, hoping we can regain enough composure to keep typing. Thus spake Charles L. Evans, one of the most economically illiterate fools ever to serve on the Federal Reserve:

“The first order thing for policy right now is to get inflation up to our objective,” Evans said at a financial literacy event in Green Bay, Wisconsin.

Yes, we know that the Fed heads are obsessed with hitting the 2.00% inflation mark as if it were some kind of religious totem, but must they insult the common folk at a "financial literacy event" in Green Bay with the risible proposition that we don't have enough inflation?

Even when you allow for all the manipulations of the CPI such as the geometric mean adjustment and hedonics, the chart below shows what "insufficient inflation" looks like since the year 2000. And that's after you have paid double the price for a new auto that the BLS says has not increased in price for 17 years; substituted more hamburger for steak, and gotten squeezed into an ever-shrinking airline coach seats that the BLS says have gone down in price!

In fact, the BLS' sawed-off price ruler known as the CPI was up 2.2% on a Y/Y basis in September. Not only is that in excess of the magic Fed target, but it's not a one-off monthly aberration, either. Since the year 2000, the compound annual increase in the CPI has been 2.1% (red line below).

How in the world is that insufficient inflation? A buck you saved in honor of the millennium is now worth just 70 cents.

And that's assuming that you are not in the lower half of the income distribution where necessities take up a larger share of budgets than their weightings in the CPI. Thus, over the last 17-years, housing rents are up 3.1% per year (purple line), gasoline prices have risen 3.5% annually (brown line), medical care is higher by 3.8% per annum ( dark blue line) and education prices have risen by 5.0% each year (light blue line).

So, yes, Charles, we got no shortage of inflation. Well, except for the green line in the chart below, which says that "inflation" has averaged only 1.8% per year since the turn of the century when the Fed went into money printing on a big time basis. That is, its balance sheet went from $500 billion then to $4.4 trillion now, thereby rising at a 13.7% CAGR.

It put's you in mind of Ronald Reagan's great story about the birthday boy who was delighted to be shown into a room full of manure. "There has to be a pony in there somewhere", the Gipper always gamely rejoined.

But don't even give Evans credit for finding the shortest inflation yardstick in the room. The Fed's favorite measuring rod----the personal consumption expenditure deflator----is not a proper cost of living index at all; it's a chain-price deflator, not a fixed price index.

Accordingly, if society is getting poorer because people are eating more chicken and less steak, inflation goes down! And if society is getting richer due to technological change, inflation goes down, too!

For crying out loud, Charles, despite all its imperfections the CPI has been hitting the Fed's inflation target year after year----when you average out the short-term puts and takes----for the entirety of this century. Isn't that close enough for government work?

Stated differently, where is one single scientific study that shows that a 0.2% shortfall even on the PCE chain deflator over an extended period of time has caused real production and living standards to be lower than that would have been at the magic 2.00%?

Obviously, there is none. The "insufficient inflation" mantra is simply ritual incantation by the high priests of the central banking system attempting to justify there immense power to falsify financial asset prices and redistribute wealth to the top tier of households and Wall Street speculators.

Nor is Charles Evans alone in his inflation-envy. Our Keynesian schoolmarm was at it again at the IMF confab in Washington, instructing one and all on why the Fed keeps pleasuring Wall Street with cheap carry trade funding that actually bears a negative cost after inflation.

Such a deal! Speculators only need buy something with a yield or prospect of price appreciation and Yellen & Co will see to it that they can finance those positions with overnight money that does not dent their winnings---even ever so slightly.

That's what the Fed is actually doing because under conditions of Peak Debt the central bank's falsified "low" interest rates never get to main street; they do not "stimulate" much housing or refrigerator purchases by consumers or equipment investments by business. Instead, they are operative mainly in the canyons of Wall Street where they fuel massive leveraged speculations---especially in options, derivatives and bespoke trades fabricated by Goldman Sachs et.al.

By contrast, here is what Janet thinks she is doing:

Federal Reserve Chairwoman Janet Yellen said “the ongoing strength of the economy will warrant gradual increases” in short-term interest rates, to keep unemployment low and to nudge inflation toward the Fed’s 2% target.

Huh? The bolded statement is just plain gibberish. Economics 101 says rising interest rates will restrain demand and curtail inflation; and historically they have been the villain that triggers rising unemployment, not a tool to keep it low.

Still, there is no mystery as to why Yellen is turning economic law upside-down. After 100 months of radical monetary repression and negative real interest rates, our Keynesian central bankers are desperate to replenish their "dry powder" for the next inevitable downturn.

Even Yellen & Co recognizes that we are only 18 months from exceeding the longest business expansion in history, but that slashing rates to counteract a downturn from a starting point of 113 basis points (today's federal funds level) would amount to wielding a wet macroeconomic noodle.

So the Fed is on a math-driven formulaic course toward a 3% federal funds target rate and a basket full of monetary dry powder-----the very opposite of the "data-driven" policy they espouse. That is, the Fed is no longer the speculator's deft friend at the ready with a liquidity fire hose to keep the market rising.

Indeed, here's the skunk in the woodpile. The domestic and global financial system is so water-logged with excess deposit money owing to year of egregious money printing that the Fed cannot easily get back to its 3% funds target without an extended period of massive QT (quantitative tightening). That means central banks will of necessity be draining monumental amounts of cash from the financial system for years to come.

After its cold start this month of $10 billion in runoff from its bond portfolio, the Fed alone will be draining cash at a $600 billion per year annualized rate next October. Eventually, the ECB and other central banks will be forced to join the retreat and most especially the People Printing Press of China. The latter's exchange rate will literally collapse in the face of the Fed's QT unless it drains liquidity from its own bloated, over-leveraged and unstable domestic financial system.

We have called this the Great Demonetization and see no possibility that it will not eventually trigger a thundering collapse of the global financial bubble that was inflated by the opposite central bank action---the last two decade's $20 trillion monetization of government debt and related securities.

To be sure, we are not reproaching the central banks for shrinking their balance sheets---even if they are doing so for the wrong, Keynesian reasons. Unlike the Donald, we are not a "low rate" person.

Indeed, we think the Fed should neither hawk nor dove be. It shouldn't set money market rates at all. That's what the free market is designed to accomplish---and thereby assure efficient allocations of capital and honest pricing of risk and financial assets based on their intrinsic merits, not the expected machinations of the central banks.

Still, even as Yellen commences the great monetary drain she is actually doing they boys and girls and robo-machines of Wall Street an immense disservice by her preoccupation with inflation shortfalls, and preposterous suggestion that raising interest rates will help it hit the magic 2.00%.

Self-evidently, Fed ordered increases in the funds rate will not "nudge" inflation nor help "sustain" the expansion. After all, Janet used to say that Fed ordered decreases in the funds rate were also necessary to spur economic expansion. Both propositions cannot be true in either this world or the next.

What is really happening, therefore, is a giant disconnect. Our Keynesian central bankers have fostered the current "low" rate of gain in the PCE deflator by causing capital to be massively mispriced all around the planet. Consequently, there has been massive, deflationary over-investment in commodity production, manufacturing capacity and physical distribution in the EM world, thereby mobilizing and activating its vast pools of cheap peasant labor.

At the same time, central bank fostered Bubble Finance in the DM world has caused corporate C-suites to become financial engineering machines, flushing cash from dividends, stock buybacks and M&A deals back into the casino. This, in turn, has positively goosed stock prices and executive options but has done so by strip-mining cash flows, balance sheets, wage payments and employment roosters.

So there is no mystery as to why $20 trillion of central bank monetary expansion since 1995 has not produced enough gain in the PCE deflator to satisfy our Keynesian central bankers. It has actually generated unprecedented inflation---but in the price of financial assets on Wall Street rather than in the short yardstick of the PCE deflator.

Not unexpectedly, lost in her Keynesian fog, Yellen doesn't have a clue.

“The fact that a number of other advanced economies are also experiencing persistently low inflation understandably adds to the sense among many analysts that something more structural may be going on,” she said to the G-30, a private group of prominent central bankers, financiers, regulators and academics.

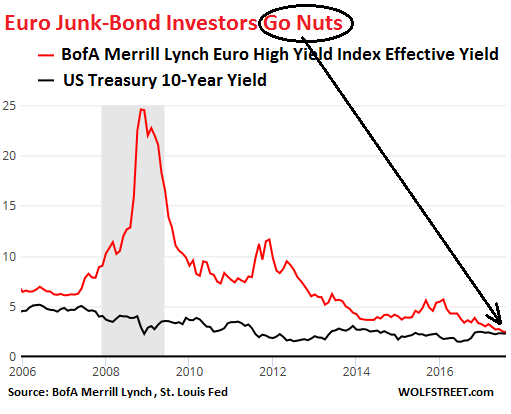

Needless to say, Janet is not alone in her obliviousness to the massive speculative bubble that has been created by the central banks over the last two decades. That is, junk bonds in Europe are now yielding less than US Treasuries, but Draghi professed at the same IMF soiree that there are no bubbles or financial imbalances in sight.

Let me be clear, I think people are convinced that stocks and shares right now and bonds can go up as well as down," Draghi said in response to a question from CNBC. "I don't think we're living in a bubbly situation.

Draghi might just contemplate for a moment that state of the economy in his home country. In 2017 Italy’s real GDP will apparently grow by 1.5% compared to the previous year. But it would still end up 6% smaller than what it was in 2007, ten years earlier! Within the same period unemployment has doubled and the number of people in poverty tripled from 1.5 million to almost 5 million.

So nearly $2 trillion of money printing has not done much for real output and living standards in Europe, but the speculators in junk bonds have made out like bandits.

At the end of the day, the whole insufficient inflation meme is a dangerous digression. By giving speculators hope that the central banks are not on a formulaic course toward demonetization, Yellen and the other central bankers are simply delaying the day of reckoning in the casino and worsening the scale of the eventual bloodbath.

The proverbial visitors from Mars might well wonder whether the planet's central banks have organized themselves into a demolition squad. So doing, they wouldn't be too far from the truth.

Disclosure: None.