Trade, Deregulation, Taxes & Sanctions

“Davidson” submits:

Major policy changes are having economic impacts.

1st-Regulation reductions occurred in 2017 and continue today. A positive multi-year impact.

2nd– Tax reductions began in 2018 and have a positive multi-year impact.

3rd-Sanctions against disruptive autocrat-led governments have gradually ramped higher resulting a stronger US$.

4th– The shift towards global tariff reductions is a new policy initiative which has likely contributed to a stronger US$.

So much change in the process without a clear outcome in view. How do we adjust portfolios to be best positioned? Taking the various outcomes one at a time and signals from the economic data provide useful insight. At the moment conditions remain decently positive and could even turn more positive should initiatives produce hoped for outcome.

Outcomes that have occurred and what appears likely to occur:

Points 1: Fewer regulations lower costs to businesses and leaves room to hire more employees where needed and/or raise employee pay. Some of this has been in the headlines.

Point 2: Lower taxes raise incomes for individuals and businesses. The multi-year benefit should be obvious.

Points3&4: We have seen a recent rise in the US$ Index which shows some shifting of capital to US$ assets as sanctions have been applied against No. Korea, Russia, Turkey, Iran, and Venezuela. The tariff issues are also having some impact on where capital sees the better opportunities.

At issue for the US businesses is the impact a rise in US$ has on exports. But, US$, currently at 90, has not risen to the 95 level which created the industrial recession 2014-2016. In every well-managed US manufacturing company, major adjustments occurred with costs lowered. They became more competitive and business has resumed with a surge of new orders. US businesses have a tradition of meeting market disruption with a new competitive attitude. The phenomena of ‘The Leaning of US Manufacturing’ continues as a dominant theme.

I note: The currencies of sanctioned countries have been falling for several years as internal business climates deteriorated. The newer sanctions have only accelerated existing trends.

(Click on image to enlarge)

Along with US$ strength, we have also seen a fall in the US 10yr Treasury rate as global capital seeks a safe haven away from sanctioned countries. This provides an interesting dichotomy as T-Bill rates rise because the strengthening business climate in the US is resulting in investors shifting capital into equities. This narrows the T-Bill/10yr Treasury rate spread to 0.85% which is just below the historical mid-range characteristic of global economic expansion. We remain well above 0.2% level which characterizes the slowing of bank lending that leads to recessions. Lending remains at decent levels.

(Click on image to enlarge)

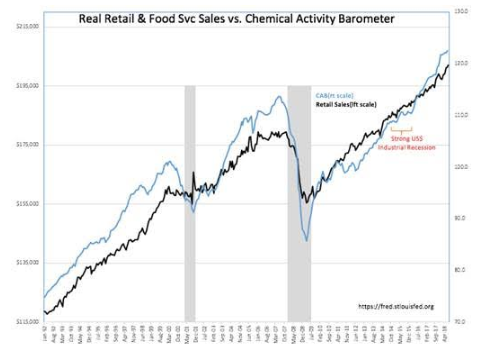

Two key leading indicators of economic activity which have a history of marking ends/beginnings of the economic cycle are Real Retail&Food Svs Sales and the Chemical Activity Barometer(CAB). Both of these and others not shown display no signs of economic slowing. Their current trends indicate some acceleration of US consumer spending. A very good sign and in agreement with tax and business regulations reduction.

Note in Trade Weighted US$ Index Major Currencies vs. $WTI Daily chart: $WTI has broken from the inverse relationship with US$ in place since 2003. I interpret this to mean that global oil supply/demand is driving prices higher contrary to the pricing influence of a stronger US$.

(Click on image to enlarge)

The Investment Thesis August 16, 2018:

Multiple policy initiatives have occurred or are in the process of initiation 2017-2018. Even with the many moving parts, the impact thus far is quite positive. There has been significant confusion in Wal Street commentary with many planning for a market top/recession. Recessions do not come out of the blue. Recessions have well-defined triggers which show up in multiple indicators with 12mos-24mos of warning. At the moment, it appears economic activity is accelerating. We should see higher equity prices in the months ahead.

My recommendation remains that investors exit Intl equities to be fully committed to US-based equities. Any positive changes in tariffs will favor US businesses and I expect US$ to eventually return to lower levels as US trade continues to expand globally.

Disclosure: The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or ...

more