This bull market seems unstoppable.

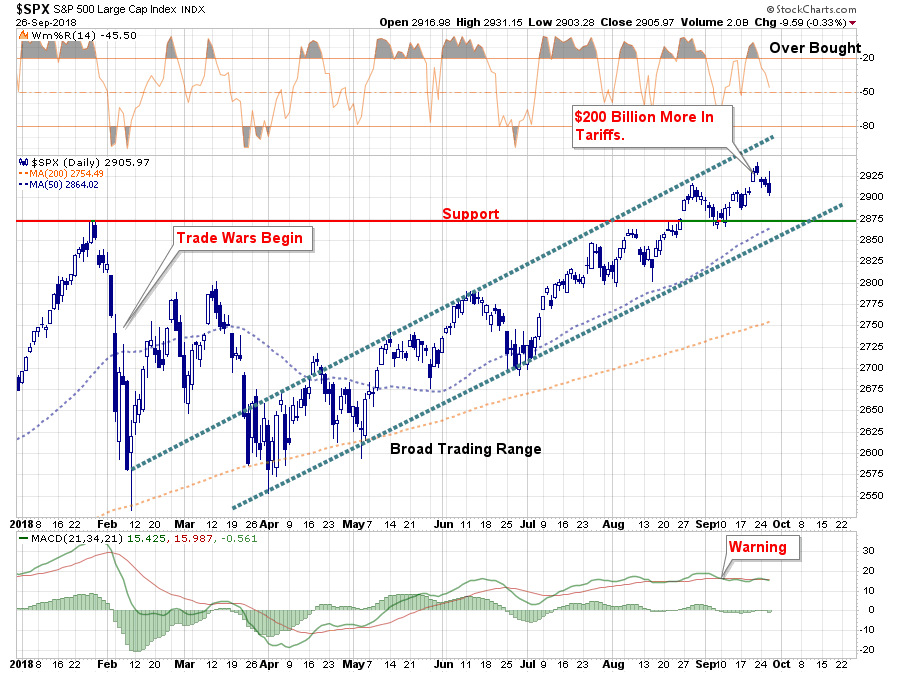

Regardless of short-term events, investors have quickly looked beyond those risks to in a bid to push stock prices higher. For example, in February of this year the markets dove roughly 10% as “trade wars” became a “thing.” Over the next two months, the markets vacillated coming to grips with what “Trump’s war with China” would actually mean. Last week, the Administration announced a further $200 billion in tariffs against China, China cancels talks with the U.S., and China imposes similar tariffs against the U.S. – and the market barely budges..

Seemingly, nothing can derail this bull market which is now the “longest in history” by some counts.

However, in my opinion, the two biggest threats to the bull market may very well be the two issues which are the most visible currently – tariffs and interest rates.

Tariffs

One of the biggest drivers of the “bullish thesis” is the explosion in earnings due to the tax cuts passed in December of 2017. However, the issue is that tax cuts only provide a very short-term benefit and, since we compare earnings on a year-over-year basis, growth will drop back towards the growth rate of the economy next year.

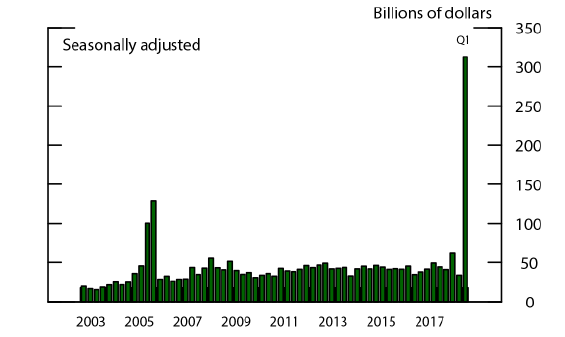

For now, the issue has been overlooked due to the surge in earnings from the changes to the tax code as well as the massive surge in repatriated dollars from overseas due to that lower tax rate. As shown by the Federal Reserve:

“Balance of payments data show that U.S. firms repatriated just over $300 billion in 2018:Q1, roughly 30 percent of the estimated stock of offshore cash holdings. For reference, the 2004 tax holiday, which provided a temporary one-year reduction in the repatriation tax rate, resulted in $312 billion repatriated in 2005, of an estimated $750 billion held abroad.”

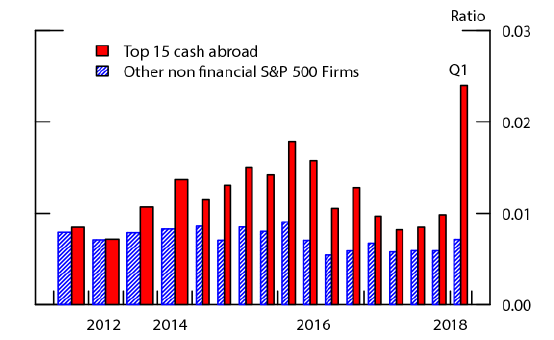

Of course, while it was expected to go to CapEx and wages, it went to share buybacks instead.

“The top 15 firms account for roughly 80 percent of total offshore cash holdings, and roughly 80 percent of their total cash (domestic plus foreign) is held abroad. Following the passage of the TCJA in late December 2017, share buybacks spiked dramatically for the top 15 cash holders, with the ratio of buybacks to assets more than doubling in 2018:Q1.”

Not surprisingly, since buybacks reduce the number of shares outstanding, bottom line EPS surged sharply despite a quarterly decline in revenues/share which slumped from $329.59/share in Q4 to $320.39/share in Q1.

While the bull market thesis continues to be that earnings expansion will justify higher valuations, such may not be the case. Tariffs, which are a “tax on profits,” could effectively eliminate the majority of the temporary benefits provided by tax cuts to begin with.

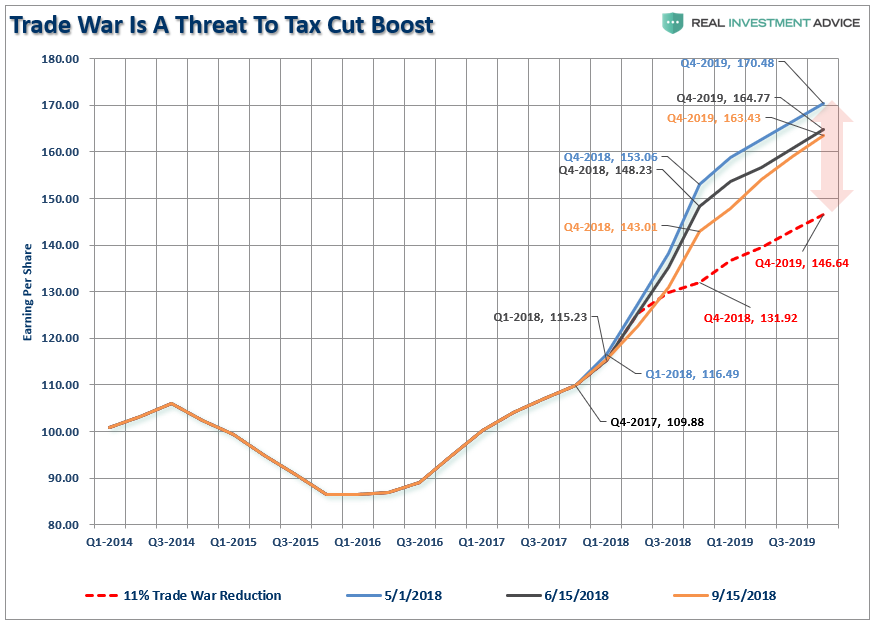

“As I wrote recently, the estimated reported earnings for the S&P 500 have already started to be revised lower (so we can play the “beat the estimate game”) but an ongoing trade war could effectively wipe out the entire benefit of the tax cut bill. For the end of 2019, forward reported estimates have declined by roughly $9.00 per share.”

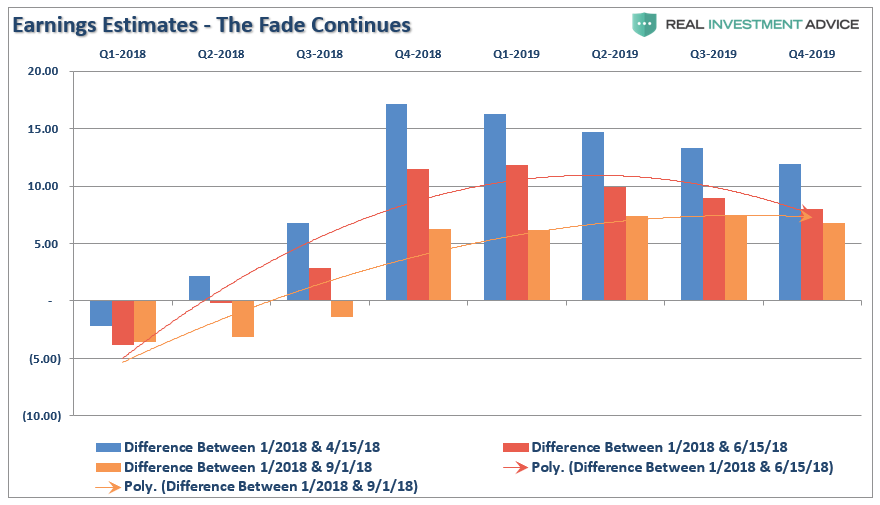

But it isn’t just this year where estimates are falling, but into 2019 as well. The chart below shows the changes in estimates a bit more clearly. It compares where estimates were on January 1st versus April, June, and September 1st. Currently, optimism is exceedingly “optimistic” for the end of 2019.

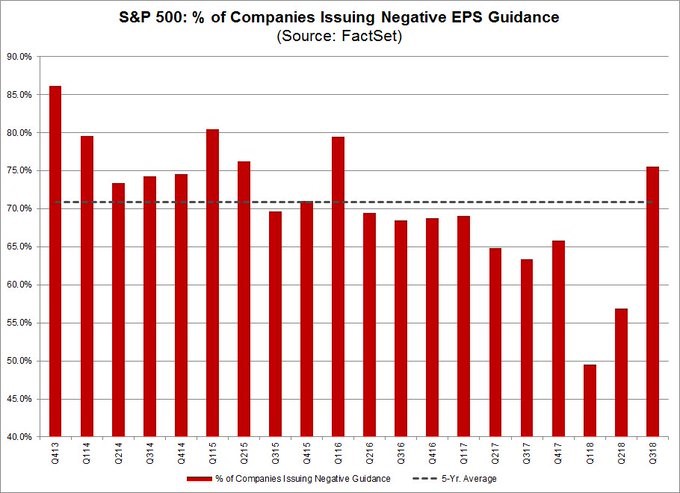

However, those estimates are likely to be revised down sharply in the months ahead as the number of S&P 500 companies issuing negative EPS guidance is now the highest since 2016.

The more tariffs that are laid on companies which do international business, the more likely we are going to see further decreases in earnings expectations. This is particularly the case given the divergence between the U.S. and the global economy.

“The trade war is now a reality. The recently announced imposition of US tariffs on a further $200 billion of imports from China will have a material impact on global growth and, even though we have now included the 25 percent tariff shock in our GEO [Global Economic Outlook – Ed.] baseline, the downside risks to our global growth forecasts have also increased.” – Fitch Chief Economist Brian Coulton.

Of course, the other issue that will weigh on corporate profitability and earnings is interest rates.

Interest Rates Matter

Yesterday, the Fed hiked interest rates for a third time this year and is set to raise again by the end of the year. With the Fed Funds rate now at 2%, it is equivalent to the Fed’s long-term outlook of the economy and inflation. More importantly, the Fed removed the word “accommodative” from their statement which also suggests they may be nearing the “neutral rate policy setting.”

Nonetheless, markets have continued to discount the risk of rising rates.

They most likely shouldn’t.

Rising interest rates, like tariffs, are a “tax” on corporations and consumers as borrowing costs rise. When combined with a stronger dollar, which negatively impacts exporters (exports make up roughly 40% of total corporate profits), the catalysts are in place for a problem to emerge.

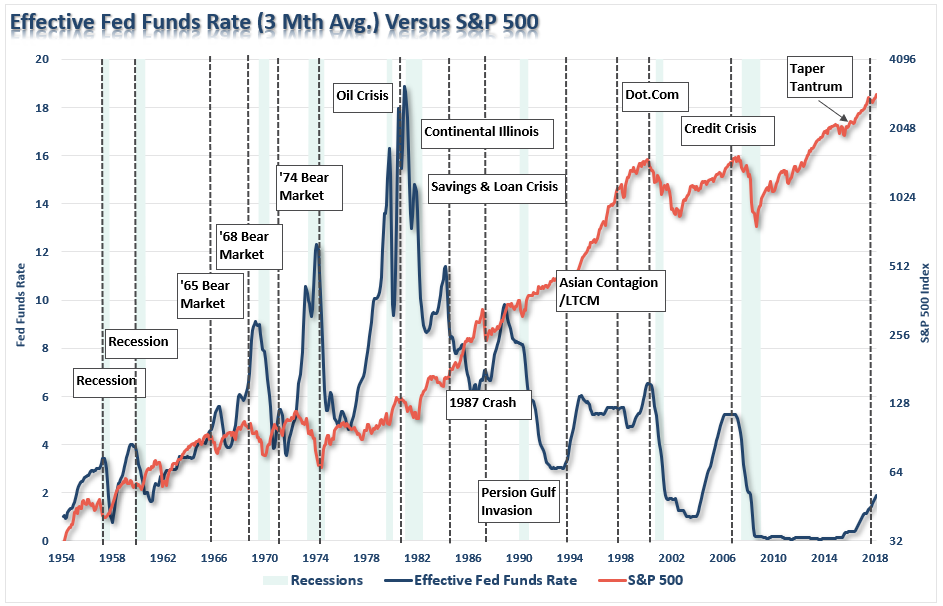

The chart below compares total non-financial corporate debt to GDP to the 2-year annual rate of change for the 10-year Treasury. As you can see sharply increasing rates have typically preceded either market or economic events. Of course, it is during those events which loan default rates rise, and leverage is reduced, generally not in the most “market-friendly” way.

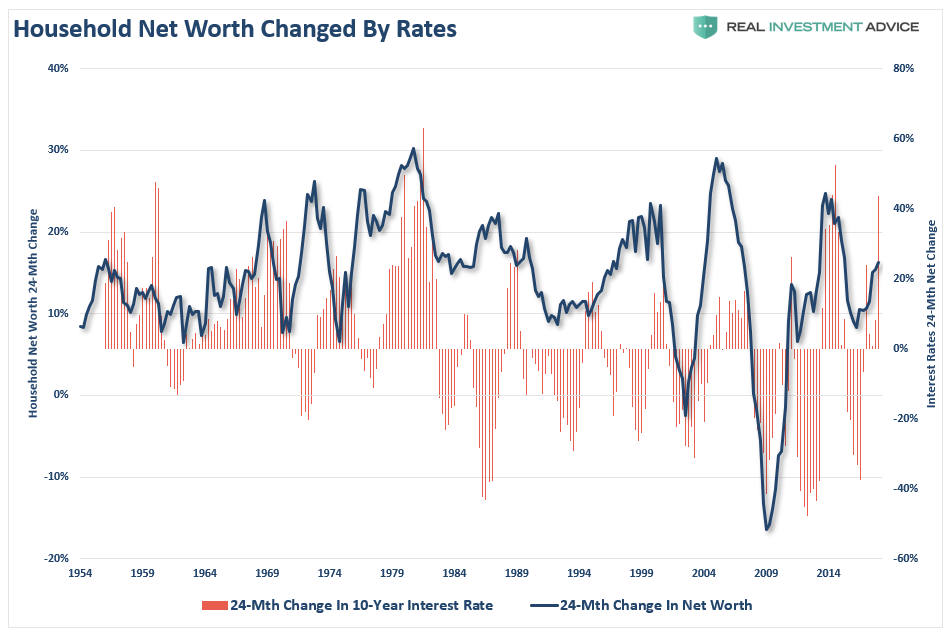

The same applies for heavily levered households. With household debt is also at historic highs, rising rates eventually lead to a reversion in household net worth.

With leverage, both corporate and household, at historical peaks, the question is not “if” but “when” rising interest rates pricks the debt balloon.

As Doug Kass recently noted – rising interest rates do matter:

- The private and public sector have inflated debt loads today. Rising interest rates raise the cost of servicing that debt and reduce spending and productive investment.

- Private sector activity is importantly influenced by interest rates:

- Rising mortgage rates and higher mortgage payments reduce home affordability and hurt home turnover and refinancings.

- Slowing home sales and reduced refinancings hurt spending on renovations and remodeling.

- Given record-high auto prices and the difficulty in further lengthening out already long auto loan maturities, rising interest rates will hurt auto sales by raising monthly payments.

- Consumer, mortgage and corporate loans that are variable rate are hurt by climbing interest rates.

- The credit markets fall when interest rates rise, serving to have a negative wealth effect on consumers and corporations that own bonds.

- Rising interest rates impede corporate profit margins, overall profits and earnings per share

- Debt is issued by corporations in order to buy back stock and pay dividends. Advancing rates reduce a company’s return on investment on those buybacks.

- Corporate capital spending is partially dependent on borrowings. Higher borrowing costs could lead to lower capital spending.

- Public sector activity and profitability are greatly influenced by interest rates:

- The deficit/GDP ratio will increase as interest rates rise and the expectation for lower future deficits will crumble.

- Dividend discount models are based on future estimates of cash flow discounted back at an appropriate interest rate:

- Rising interest rates reduce the value of those future cash flows and, in turn, the value or worth of a company’s stock.

- There is now an alternative to stocks as the yield on the one-month Treasury bill (2.06%) and two-year Treasury note (2.85%) compare favorably to the S&P’s dividend yield of only 1.75%. Additional increases in interest rates will serve as an even more competitive and attractive alternative to stocks.

As I noted previously, the Fed has a bad habit of hiking rates until something breaks.

Stock Market Implications

As long as the backdrop is healthy, in this case, strong earnings and economic growth, the markets can fend off attacks from higher rates and geopolitical issues. However, as tariffs attack corporate profitability, and weakens economic growth, it makes the system much more susceptible to the virus of higher rates. This will most likely expose itself as credit-related event which will be blamed for a bigger correction in the market. However, “Patient Zero” will be the Federal Reserve.

Even one of the most bullish individuals on Wall Street, Wharton finance professor Jeremy Siegel, is now turning cautious. While he isn’t abandoning his bullish backdrop for stocks, particularly since he is involved in everything from ETF’s to Robo-advisors, he suggests it is vital for investors to be aware of growing risks stemming from tariffs and interest rates which could spark a sell-off.

“This market has had a great run, and I wouldn’t be surprised to see another correction. We have some major challenges. The trade war is not yet resolved.

We’re going to see how hawkish [the Fed] is with the labor market as tight as it is. I still believe that they’re going to be on track for four increases this year. The question is how will they feel about another raise in December. And, I think between the trade situation and the interest rate situation, and then, of course, the midterms in November, there are a lot of challenges facing Wall Street.” – Trading Nation.

While Siegel only expects a sell-off like the one we saw in February of this year, the real risk is of one much deeper in nature. As noted just recently in “Ingredients Of An Event.”

“The risk to investors is NOT just a market decline of 40-50%. The real crisis comes when there is a ‘run on pensions.’

This is a $4-5 Trillion problem with no resolve to “fix” the problem before it occurs. This leaves a large number of pensioners already eligible for their pension at risk and the next decline will likely spur the “fear” benefits will be lost entirely. The combined run on the system, which is grossly underfunded at a time when asset prices are dropping, will cause a debacle. With consumers are once again heavily leveraged with sub-prime auto loans, mortgages, and student debt, they too will be forced to liquidate assets to meet payment demands.

All the ingredients for a more severe market correction are currently present. Between Trump’s “trade war” and the Fed insistence on hiking rates, it certainly seems as if they are “hell-bent” on lighting the fuse.

Comments

Log in or sign up to join the conversation.