<< Read More: The Myths Of Stocks For The Long Run - Part I

Written by Lance Roberts, Michael Lebowitz, CFA and John Coumarianos, M.S. of Real Investment Advice

Crashes Matter A Lot

In Part I – Buy and Hold can be Hazardous to your Wealth, we showed how the stock markets tend to cycle between growth and decline. Passive, “buy and hold” investors who hold their investments through the cycles are likely to endure long periods of time in which they are recovering losses and not compounding their wealth. As discussed, falling into this age-old trap for a decade or longer violates Warren Buffett’s two golden rules of investing:

- Don’t Lose Money

- Refer To Rule #1

In “Part II” of this series, we will discuss why avoiding major market corrections is so important. We also dive into a related topic, the “savings problem.”

As noted previously, many of those who promote “buy and hold’ type philosophies often claim that those who dollar cost average (DCA) on a regular basis endure much shorter periods recovering previous losses. While they are partially correct, as recovery periods from losses are shorter, evidence clearly shows few individuals actually invest that way.

As discussed previously, investors do NOT have 90, 100, or more years to invest. Given that most investors do not start seriously saving for retirement until the age of 35, or older, that leaves 30-35 years for them to reach their goals. If that stretch of time happens to include a 12-15 year period in which returns are flat, as history tells us is probable, then the odds of achieving their goals are massively diminished.

Let’s walk through an example showing why avoiding “mean reverting events” matters.

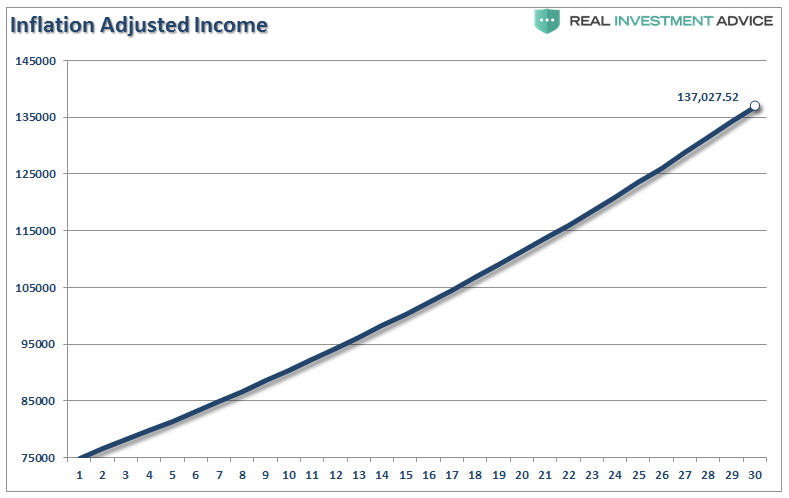

Bob is 35-years old, earns $75,000 a year, saves 10% of his gross salary each year and wants to have the same income in retirement that he currently has today. In our forecast, we will assume the market returns 7% each year (same as promised by many financial advisors) and we will assume a 2.1% inflation rate (long-term median) to help determine his desired retirement income.

Looking 30 years forward, as shown below, when Bob will be 65, his equivalent annual income requirement will be approximately $137,000 as shown below.

Understanding the relevance of this simple graph is typically problem number one for investors. Many savers fail to realize that their income needs will rise significantly due to inflation. In Bob’s case, $137,000 is the future equivalent to his current $75,000 salary assuming a modest 2.1% rate of inflation. If the double-digit inflation rate of the 1970’s were to reappear, Bob’s income needs would be significantly higher, and a larger lump sum of savings would be required to generate that higher level of income.

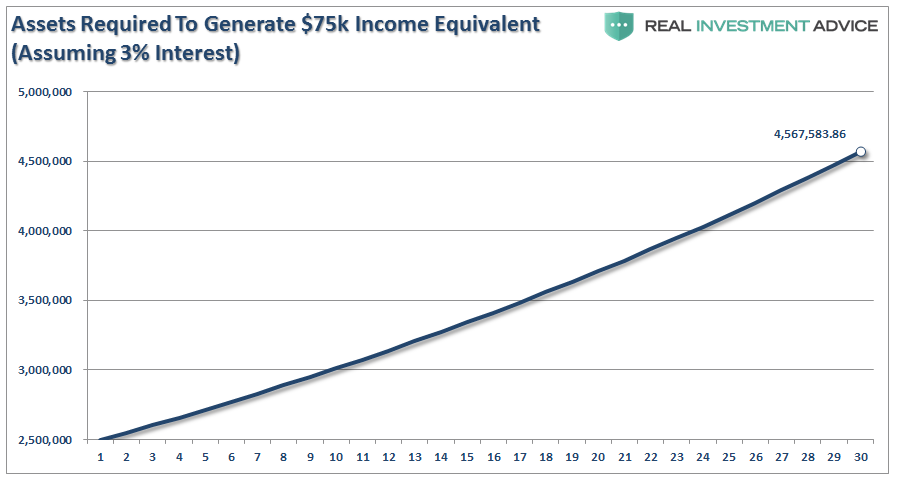

In this case, to meet his $137,000 retirement income goal and keep his wealth intact, Bob will need to amass a portfolio over $4.5 million. The figure is based on a 3% withdrawal rate matching the long-term Treasury yield.

(The graph excludes social security, pensions, etc. – this is for illustrative purposes only.)

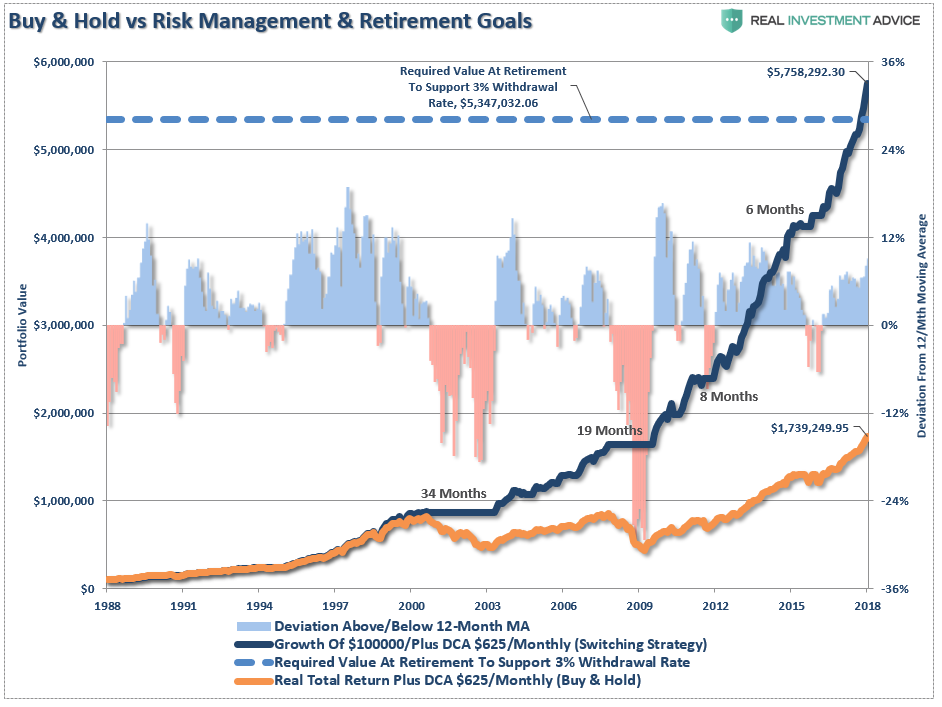

In this analysis, we give Bob a big advantage and assume that he has been a diligent saver and has accumulated a nest egg of $100,000 to jump-start his savings adventure. Furthermore, we start his investment period in 1988 following the 1987 crash. Bob’s first 12 years of investing was one of the greatest periods to be in U.S. equities.

As stated, we are giving Bob every benefit we can.

With the example set, let’s run an analysis to determine if “buying, holding and dollar cost averaging” into the S%P 500 will get Bob to his retirement goal.

To answer this question, the chart below shows the difference between two identical accounts.

- Each started at $100,000, each reflects $625/month contributions (DCA)

- Both were adjusted for inflation and include dividends. (Total Return)

- The blue dotted line shows the amount of money Bob requires to meet his retirement goal in 30-years.

- The gold line is the “buy and hold” strategy using the S&P 500 index.(Passive)

- The blue line utilizes a simple switching strategy that goes to “cash” whenever the S&P 500 declines below the 12-month moving average. (Active)

- The blue and red shaded areas show the deviation of the S&P 500 above and below the 12-month moving average.

Had Bob followed a buy and hold strategy he would have turned his $100,000 investment into a respectable $1.7 million nest egg.

While such a sum is certainly nothing to scoff at, when Bob applies his 3% withdrawal rate, his annual income will fall to just $51,000 per year. Not only is this less than he was making 30-years ago, it is far short of the $137,000 income needed.

What clearly impacted his progress was the recovery periods following the crashes of 2000 and 2008.

The obvious advantage of the actively managed portfolio is the avoidance of the major drawdowns which allowed it to effectively compound over the expected time frame. Not only did his initial $100,000 investment grow to $5.75 million, which exceeded his required retirement objective, at 3% interest it generated more than enough to meet his $137,000 income goal.

There is an important point to be made here. The old axioms of “time in the market” and the “power of compounding” are true, but they are only true as long as principal value is not destroyed along the way. The destruction of the principal destroys both “time” and “the magic of compounding.”

Or more simply put – “getting back to even” is not the same as “growing.”

While those selling passive strategies throw out the “you can’t time the market” argument, the simple truth is you can. Even the simple rule, as we applied, can be followed with little effort. The problem, however, isn’t the strategy, it is the investor. The biggest detraction from successful investing over the long-term is ourselves. Our emotional and behavioral biases consistently plague our investment decision making from the “fear of missing out,” to “herding,” “recency bias,” and many others are all inherent traits that we will discuss in an upcoming chapter. However, managing risk, and avoiding major mean reverting events, is quite achievable with a good bit of discipline and patience.

Crashes matter, and the time spent recouping those losses is likely to stop you from meeting your goals.

The Other Big Problem For Dollar Cost Averaging

In Bob’s example, we assumed dollar cost averaging. Today, there is little evidence individuals are actively saving adequately for their retirement.

- Poll: One-Third Of Americans Have Less Than $5000 In Savings

- Want To Make Millennials Mad, Talk About Saving For Retirement

- 43% Of Americans Can’t Pay For Food Or Rent

- No Retirement Savings? Keep Working Longer?

- 50% Of Americans Don’t Have Access To 401k Plans

- EBRI: The Is A Retirement Savings Shortfall

- NIRS: Retirement Crisis Is Worse Than You Think

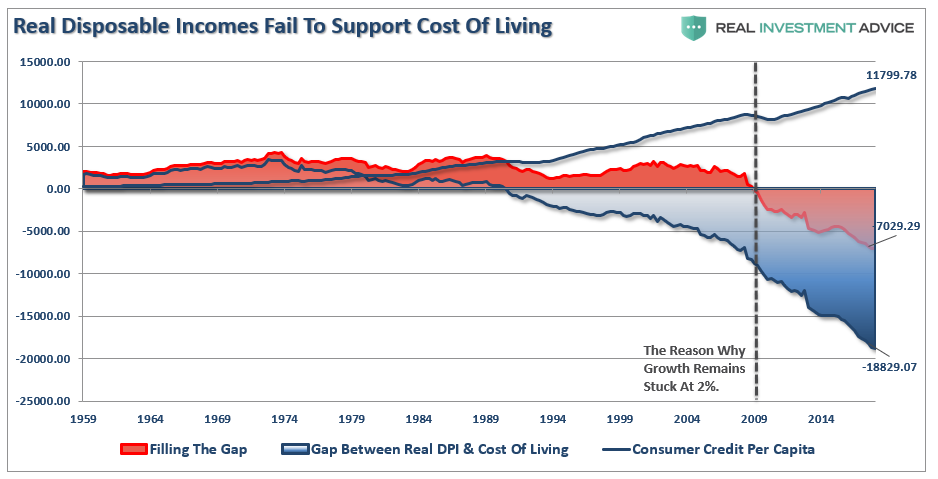

We could fill pages with study after study, but you get the idea. The reality is that about 80% of Americans currently CANNOT save adequately for retirement because of the tremendous costs associated with raising children, mortgages, debt payments, food, energy costs and health insurance. For many, these costs exceed their disposable income. As shown below, even with a sharp ramp-up in consumer credit, there is still a nearly $7000 deficit between the required standard of living and what incomes and debt combined can fill.

(Click on image to enlarge)

This goes a long way in explaining why the majority of Americans are NOT saving for their retirement. While Josh Brown was correct that individuals add to their company plans on a regular basis, the reality is that most “Americans” do not invest at all.

“Americans do most of their saving for retirement at their jobs, though many private sector workers lack access to a workplace plan. In addition, many workers whose employers do offer these plans face obstacles to participation, such as more immediate financial needs, other savings priorities such as children’s education or a down payment for a house, or ineligibility. Thus, less than half of non-government workers in the United States participated in an employer-sponsored retirement plan in 2012, the most recent year for which detailed data were available.”

But even if they don’t have access to a plan, they are surely investing in the stock market on their own, right? Not really.

“Among filers who make less than $25,000 a year, only about 8% own stocks. Meanwhile, 88% of those making more than $1 million are in the market, which explains why the rising stock market tracks with increasing levels of inequality. On average across the United States, only 18.7% of taxpayers directly own stocks.”

With the vast amount of individuals already vastly under-saved, the next major correction will reveal the full extent of the “retirement crisis” silently lurking in the shadows of this bull market cycle.

Summary

Markets stand at valuations that offer very little return yet historically large risks. In the past, every market environment like the current one was met with a major correction that took years for investors to recover from. While we do not know when such a move lower will start, make no mistake markets have not suddenly become immune from “mean reversion.”

We do not advocate you sell all of your stocks. We just hope you consider the risk/return proposition and invest with a strategy which aims to avoid major losses.

We end with a paragraph from Andrew W. Lo from his book Adaptive Markets: Financial Evolution at the Speed of Thought

“In this respect, we can think of markets as being bipolar- they can seem ordinary on most days, but once in a while, a dark mood settles over the market, and prices drop precipitously in response to the most innocuous news. When we compute an eighty-eight year average, the impact of these periodic slumps may not be very great, but the problem for investors is they do not get to earn the eighty-eight year average. Long-term averages can hide many important features of the financial landscape, especially when the long-term average is so long that it includes radically different financial institutions, regulations, political and cultural mores and investor populations. A river may have an average depth of only five feet, but that doesn’t mean it can be crossed safely by a six-foot hiker who can’t swim.”

Comments

Log in or sign up to join the conversation.