The Fed’s Credit Channel Is Broken And Its Bathtub Economics Has Failed

Among the many evils of monetary central planning is the conceit that 12 members of the FOMC can actually tweak the performance of a $17 trillion economy on virtually a month to month basis—using the crude tools of interest rate pegging and word cloud emissions (i.e. “verbal guidance”). Read the meeting minutes or the actual transcripts with a five-year release lag and they sound like an economic weather report. Unlike the TV weatherman, however, our monetary politburo actually endeavors to change the economic weather for the period immediately ahead.

Accordingly, the Fed is pre-occupied with utterly transient and frequently revised-away monthly release data on retail sales, housing starts, auto production, business investment, employment and inflation. But its always about the latest ticks in the data—never about the larger patterns and the deeper longer-term trends. And of course that’s the essence of the Keynesian affliction. The denizens of the Eccles Building—-overwhelmingly academics and policy apparatchiks—-rarely venture into the real economic world, and, therefore, do believe that the US economy is just a giant bathtub that must the filled to the brim with “aggregate demand” and all will be well.

Filling the economic bathtub is accomplished through something called “monetary accommodation”, which essentially means credit expansion. That is, market capitalism left to its own devices is inherently suicidal—or at least a chronic underperformer. Households and businesses almost always spend too little and therefore need to be induced to become more exuberant in the shopping aisles and on the factory floor.

In this framework, the blunt instrument of artificially depressed interest rates is the natural policy tool of choice. If cautious households are saving too much for a rainy day or even their children’s education or their own retirement, why club them with ZIPR (zero interest rates); get them shopping until they drop. Likewise, if businessmen do not see the case for opening another store or buying a new lift truck for their warehouse (or expanding same), bribe them with cheap debt financing.

In short, the primary route of monetary policy transmission for Keynesian central bankers is the credit expansion channel. Using that economic plumbing system they endeavor to goose aggregate demand and thereby fill the economic bathtub to its brim—otherwise know as potential output and full employment. Furthermore, by a Keynesian axiom—-known as the Phillips Curve trade-off between inflation and employment—there is no possibility of serious goods and services inflation until the tub is fall and all capital and labor resources are fully employed.

So the whole gig amounts to a simple mandate: Keep pumping aggregate demand through the credit channel until potential GDP is fully realized because, ipso facto, that means that the Fed Humphrey-Hawkins mandate of price stability and maximum employment have also been achieved. So in effect, the Fed heads watch the ticks and blips of the “in-coming data” with such intensity because they believe their job will be done when the US economy finally reaches its brim.

This entire Keynesian bathtub model is nonsense, of course, not the least because the US economy is not a closed system, but functions in a rambunctious, open global economy where massive flows of trade, investment and finance impinge heavily on prices, costs, wages and productive asset returns, and therefore the daily behavior of millions of domestic workers, businesses, investors and financial intermediaries. So the Fed’s Keynesian model is fundamentally flawed—-a reality that perhaps explains its stubborn adherence to policies that do not achieve their stated macro-economic objectives, but fuel serial financial bubbles instead.

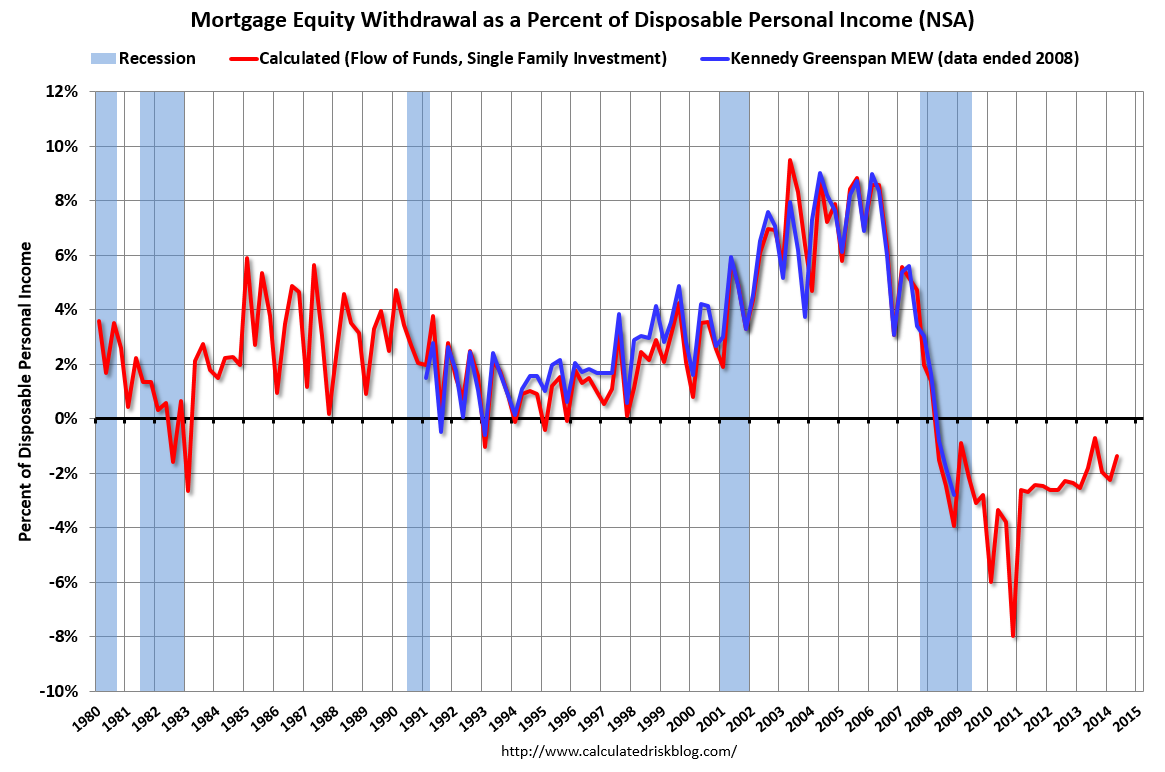

However, even apart from the fundamental flows of its basic economic model, the Keynesian pre-occupation with the economy’s mythical full-employment brim and the short-run business cyclical fluctuations related to it cause our monetary central planners to ignore the obvious. Namely, that the credit transmission channel is broken and done, and that the massive resort to money printing—especially since the dotcom bust in 2000—have been accompanied by sharply deteriorating economic trends.

Stated differently, the growth rate and general health of the US economy has drastically down-shifted during the last decade and one-half and now stands at only a fraction of its historic trends. Specifically, real GDP grew at a 4.0% rate during the golden age of sound money and fiscal rectitude between 1950 and 1970. Then it dropped to about 3% during the next 30 years after Nixon defaulted on our Bretton Woods obligation to redeem the dollar in a constant weight of gold; and since the dotcom bust in 2000 when the Greenspan Fed went all out with printing press monetary expansion, real GDP growth has amounted to only 1.7% annually. That is just 42% of its golden age rate, and in truth probably even worse if inflation were to be honestly measured by the government statistical mills.

Disclosure: None.