The American Energy Independence Index

The U.S. energy sector has undergone dramatic changes over the past five years. Hydraulic fracturing (“fracking”) and horizontal drilling have roiled global energy markets. America has shifted from planning to import Liquefied Natural Gas (LNG) to exporting it, with LNG exports expected to more than quadruple over the next three years. Cheap domestic methane has made natural gas the biggest single source of electricity in the U.S., in the process supplanting coal and unexpectedly helping reduce CO2 emissions. Increasing production of Natural Gas Liquids (NGLs) such as ethane are behind close to $200BN of investments in new petrochemical facilities. Propane exports are up five-fold in five years.

In late 2016 OPEC was forced to abandon its strategy of trying to bankrupt U.S. shale oil producers with low prices, because production fell less than needed and many OPEC countries faced gaping budget holes with little to show for it (see OPEC Blinks). Almost 40% of the world’s oil producing nations had tried and failed to kill off the Shale Revolution. American free enterprise triumphed.

(Click on image to enlarge)

The dramatic increase in hydrocarbon production represents one of the greatest examples in recent years of the power of American private sector capitalism. Technological ingenuity and constantly improving productivity allowed costs of production to keep falling. The world’s biggest capital markets provided funding to support a culture of entrepreneurialism and new business formation. Highly developed energy infrastructure networks and a skilled energy labor force were already in place, and other natural resources such as water were conveniently available. Lastly, privately owned mineral rights, a global rarity, allowed individual landowners to profit from the Shale Revolution by signing drilling leases with energy companies. In short, the Shale Revolution leveraged all that’s great about America’s form of capitalism (see America Is Great!).

The changes have been so dramatic that they’re leading us to American Energy Independence. Among the many changes are the positioning of the energy infrastructure business. For years, pipelines were synonymous with reliably stable cashflows that grew modestly and required minimal reinvestment. An entire class of investment, Master Limited Partnerships (MLPs), evolved to provide tax-advantaged exposure for those willing to handle K-1s at tax time rather than 1099s. Over $50BN was raised for deeply flawed mutual funds and ETFs that provide 1099-type MLP exposure while incurring a heavy additional tax burden (see Some MLP Investors Get Taxed Twice).

Energy infrastructure is key to American Energy Independence. Steadily increasing volumes of hydrocarbons are leading to increased investment in infrastructure. Traditional sources of crude oil, such as the Permian in West Texas, are producing more than ever even after almost a century of output. More recent discoveries such as the Marcellus Shale in Pennsylvania are producing substantial volumes of natural gas where little production existed a decade ago. Although the “toll-model” of pipelines, storage assets and processing facilities still thrives, the long-term growth opportunities in infrastructure are attracting investors willing to reinvest cashflows back into accretive projects.

As a result, energy infrastructure businesses are evolving beyond MLPs, as their need for capital has not always aligned with traditional, yield-oriented MLP investors. Simplification, in which an MLP and its General Partner merge into a single corporate entity, has broadened the investor base. MLPs are nowadays an important but shrinking portion of the opportunity set.

The secular theme of American Energy Independence reaches beyond MLPs, and this is why we’re launching the American Energy Independence Index. It’s designed to incorporate those infrastructure businesses that are critical to supporting our growing energy needs. It includes both MLPs and corporations; some large Canadian companies as well as American ones, since infrastructure is highly integrated between the U.S. and Canada. In fact, the market capitalization of the corporations in the index is $300BN, approximately the same as the Alerian MLP Index. Those investors who seek energy infrastructure exposure via MLPs are limiting themselves to a steadily shrinking subset of the relevant companies. Energy infrastructure today is about growth, and many large businesses have adopted a traditional corporate structure so as to attract global investors, rather than simply those wealthy Americans who will accept the complexity of K-1 tax reporting.

Moreover, investing in MLPs via mutual funds or ETFs usually comes with the substantial tax drag noted above (see Are You in the Wrong MLP Fund?).

The American Energy Independence Index is designed to track the companies of our energy future. The Shale Revolution is bringing the U.S. closer to energy independence. Increasing volumes of hydrocarbons need to be gathered, processed, transported and stored, all of which requires additional infrastructure.

Today the index is almost fully infrastructure supporting oil, natural gas, refined products and NGLs, because those reflect our energy mix and offer reliable cashflows. Hydrocarbons will remain the dominant source of our energy for the foreseeable future, and the index consists of energy infrastructure offering consistent economic returns over the long term. This excludes coal, since it moves by rail and ship where barriers to entry are lower, and so it is not included in the index. Although the transportation and storage of renewable energy isn’t a business today, as these technologies mature and their infrastructure begins supporting similarly stable cashflows, their place in the index will grow. The American Energy Independence Index is designed to evolve with America’s changing energy needs. It is biased towards energy infrastructure that provides reliable cashflows growing over the long term.

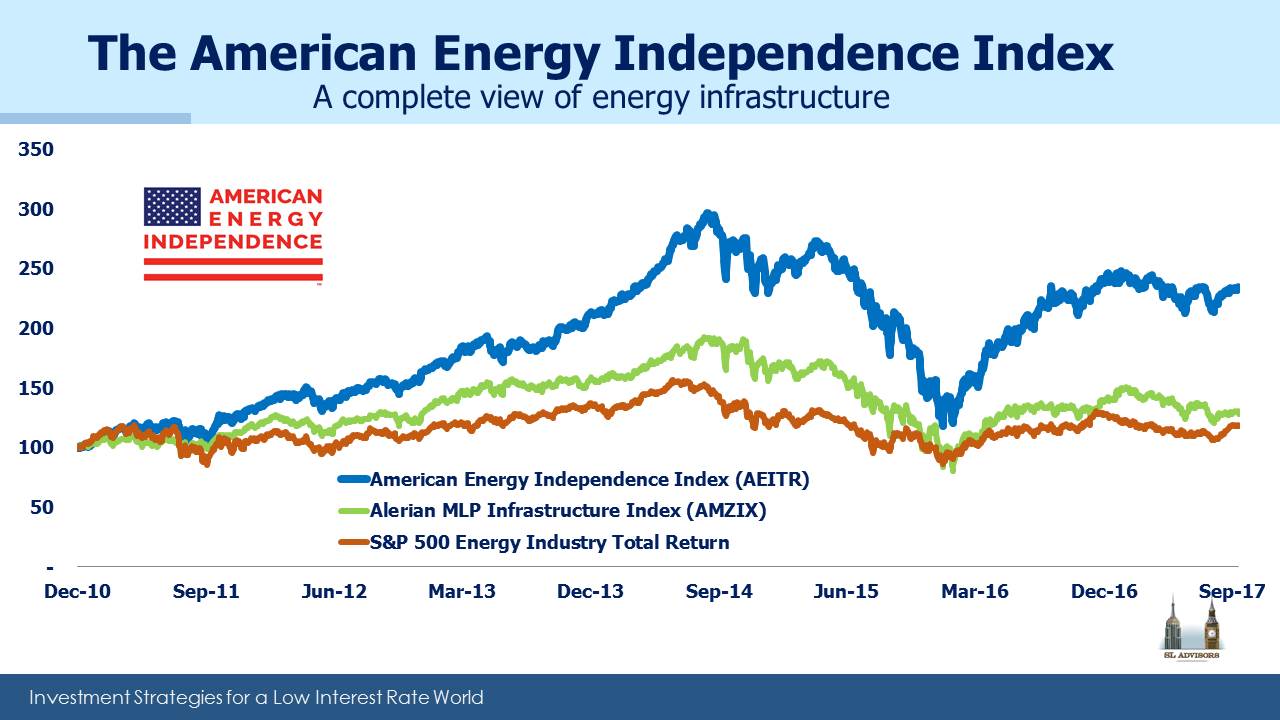

Since 2010 the American Energy Independence Index has reflected the performance of the broader energy infrastructure sector. It has moved with the Alerian Infrastructure Index but has performed better because it’s not limited to MLPs. It better reflects the future of financing infrastructure, which still uses the MLP vehicle but relies on it less than in the past. Almost all the ETFs and mutual funds in the sector focus too narrowly on MLPs, instead of covering the entire universe of energy infrastructure opportunities.

In a few weeks, we will be making available an opportunity to invest in the index. We think it represents a superior way to participate in our energy future, as America heads towards Energy Independence.

Disclosure: None.