Technically Speaking: The Bull Won’t Die Easily

Just a short note for today as I am taking a quick vacation for the “Thanksgiving” holiday.

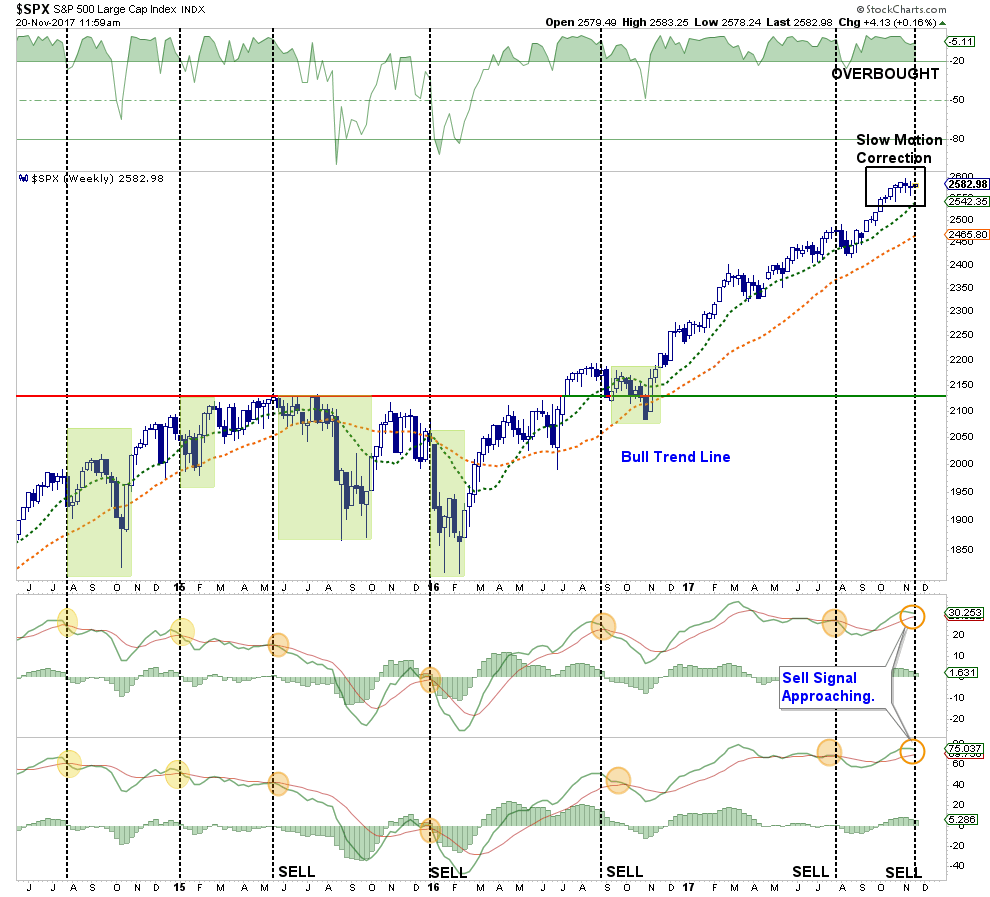

As I noted this past weekend:

“Thanksgiving week is traditionally an extremely ‘light’ trading period where the ‘inmates are running the asylum.’ With the market more overbought now than at any other period since 2011, a consolidation or further corrective action is entirely possible.

While some ‘caution’ is advised, it is NOT advisable to act ’emotionally’ to swings due to the low volume trading that will be occurring.

While the market is extremely overbought, the bullish trends remain intact. Furthermore, the last two months of the year are typically bullish for asset prices. Understanding this, these conditions keep portfolios allocated towards equity risk currently. But we do so with an eye on the risk.”

As shown below, the market is clearly overbought as the “slow motion” correction over the last 3-weeks has begun to deteriorate the September “buy” signal. While corrections have been extremely shallow (less than 3%), a continued stagnation or deterioration over the next week will likely trigger a short-term “sell signal.” This would set the stage for a mild correction in the second week of December as liquidations by mutual funds to pay out annual distributions occurs. Such a correction would work off some of the existing overbought condition and set the stage for a year-end “Santa Claus” rally.

The bigger concern, as stated over the last two weeks, is when the calendar turns into 2018. There is a risk of a deeper correction as tax-selling, concerns over monetary policy and geopolitical stresses potentially take hold. However, that is a story we will deal with over the next couple of weeks as the markets continue to develop.

For now, I am going to return to my seat, put my tray table up and settle back for my flight. I think I hear the sound of the stirring of a margarita glass and I am seriously stuck on the “salted vs non-salted” rim question.

THE RETURN OF THE MARKET WITH NO MEMORY?

– by Doug Kass

“Welcome to the party, pal.” – John McLane (Bruce Willis), “Die Hard“

The conditioning of investors has been to buy every dip and that won’t change swiftly; old habits, nine-year-old bull markets and “Die Hard’s” John McLane won’t die easily.

For many, it will be increasingly difficult to navigate a market dominated by the overly popular ETFs and quant (volatility-trending and risk-parity) strategies that worship at the altar of price momentum. It is also because the “buy the dip” mentality remains indelibly etched on the forehead of most investors and traders that the Pavlovian reaction won’t die easily.

Favoring the bulls is the diminished number of publicly held companies outstanding (from more than 7,600 in 2000 to 3,800 in 2017), a 17% reduction in the float of the remaining companies via corporate buybacks, and still-abundant liquidity. And on top of this, as previously mentioned, is the market’s participants confidence in buying the dips.

Favoring the bears is a stalled and likely ineffective tax reform initiative (an outgrowth of a dysfunctional White House), a mature business cycle, slowing domestic economic and corporate profit growth relative to consensus expectations, and elevated valuations — all among the issues discussed in yesterday’s opening missive. And on top of all this is the ever-present risk of the Global Short Volatility Bubble that could precipitate a “flash crash” at almost any time.

The markets are likely to be whippy in the near term, subject to year-end influences. The expectation or promise of a reduction in capital gains taxes could be another important factor weighing on the markets.

While my short book is sizable, I plan to trade opportunistically around it from both the long and short sides over the balance of the year.

Bottom Line

“I don’t know.

That’s nice.

I really like that

You know what I am going to do?

I am going to leave your words on this blackboard for all my classes to enjoy

Giving you full credit of course, Mr. Spicoli.” -Mr. Hand, “Fast Times at Ridgemont High“

On a daily basis, the talking heads parade in the business media with self-confident views of markets and economic growth. But the reality is that the only certainty is the lack of certainty. Despite their confidence and protestations, this is not likely a good backdrop to exhibit self- confidence in view.

Too many are confident in view at a time when there are so many political, geopolitical, economic and market outcomes that potentially are adverse.

The above is a blueprint of my strategy and my attempt to game an inconsistent market with no memory from day to day, and one dominated by investment products governed by machines and algorithms relying on price-momentum strategies that are agnostic to balance sheets, income statements, and private-market value.

If it sounds like I am confused and uncertain as to where the market is moving over the short term. I am. Others should be as well given the wide complexities of the factors that contribute to the investment mosaic today.

However, it should be reasonable to think, given the many factors raised in my Diary, that while the nine-year-old bull market may not die easily, it will die.

I continue to believe that the complexion of the market is changing, and for the worse. The technicals are deteriorating, and so are the Russell 2000 and junk bond Indices, but the machines, algorithms, and ETFs run the asylum and a move straight down seems unlikely unless a Black or Orange Swan emerges.

Regardless of my view, it’s probably a good time to try to stay out of trouble with larger-than-average cash positions.

My guess is that the market without memory from day to day will frustrate both bulls and bears with its inconsistencies in the days and weeks ahead.

I plan to remain flexible and opportunistic, placing a greater-than-normal emphasis in my portfolio on trading versus. investing over the rest of 2017.

I am still very bearish, however, using a three- to nine-month time frame in light of my view that there is roughly four times more risk than reward. And I recently have added a number of individual short names into my portfolio — namely General Motors (GM), CSX (CSX), Union Pacific (UNP), Caterpillar (CAT) and Deere (DE).

But, bull markets die hard.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more