Shorts Piling Into Equifax (EFX)

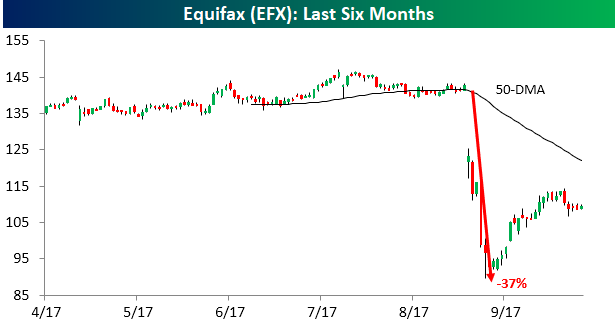

What happens when a company entrusted with the personal information of US consumers gets hacked and exposes the names, addresses, Social Security numbers, birth dates, and even drivers license numbers of just about every American who has a credit report?Well, for starters, your stock price goes down, and that’s exactly what happened to the price of Equifax’s stock after news of the massive security breach first broke in early September. From the close on 9/7 to its intraday low on 9/14, shares of EFX plunged more than 37%.

(Click on image to enlarge)

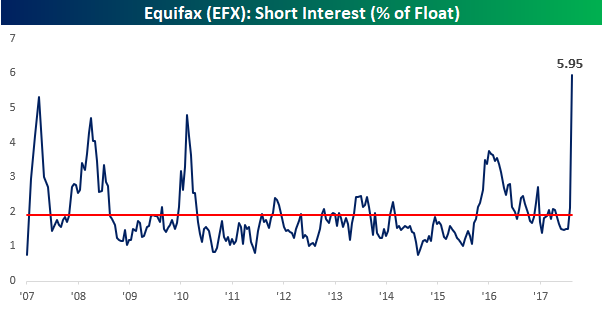

While they have recovered a bit of that decline in the last month, short-sellers have been piling into the stock, sending its short interest as a percentage of float up to just under 6%. While 6% may not sound like a lot when other stocks have more than half of their float sold short, with its historically stable business, EFX is not the type of stock that typically attracts short-sellers. For EFX, 6% short interest is a stratospheric level. In fact, looking back over the last decade, short interest levels for EFX have never been as high as they are now after the security breach. Not even during the financial crisis! Now, one could easily argue that for Equifax at least, the latest security breach is a much more negative event than the financial crisis, so the high level of short interest may very well be warranted. After all, the company is undoubtedly far from being out of the woods. What the high short interest level does provide, though, is some degree of cushion against further weakness. With the stock already down over 25% and 6% of its outstanding shares sold short, eventually, those shares will have to be covered.

(Click on image to enlarge)

Disclosure: Gain access to 1 month of any of Bespoke’s premium membership levels for ...

more