US stock benchmarks hit new all-time highs this month, and despite rich valuations, buyers think they’ll go higher still.

One reason for this exuberance is the growing dominance of passively indexed ETFs.

Rather than go to the trouble of picking individual stocks, people dump their cash into index ETFs. The ETF sponsor then buys every stock in the index—even the ugly ones.

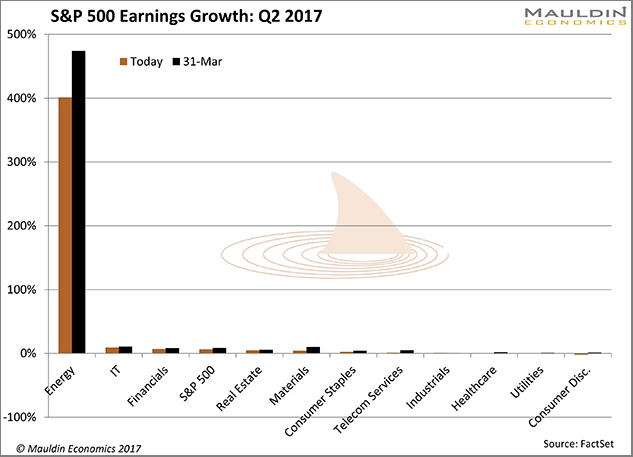

Profit growth seems to justify this, even in the broad indexes. In its June 16 bulletin, FactSet Research estimated that combined profits in the S&P 500 companies will rise 6.5% in this year’s second quarter.

So, “combined profits” means some companies (and sectors) performed better than average, some worse, right?

Actually, no.

What we really have is one sector growing profits at a gangbuster rate. The others, not so much.

Break down that 6.5% profit growth by sector, and you get this:

Here are the sectors that comprise the S&P 500’s 6.5% earnings growth this quarter, in ascending order.

| Sector |

2Q Estimated Earnings Growth |

| Consumer Discretionary |

-2.0% |

| Utilities |

-0.5% |

| Healthcare |

0.5% |

| Industrials |

0.9% |

| Telecom Services |

1.3% |

| Consumer Staples |

2.5% |

| Materials |

4.4% |

| Real Estate |

5.1% |

| S&P 500 Average |

6.5% |

| Financials |

6.9% |

| Technology |

9.4% |

| Energy |

401.3% |

As you can see, the 6.5% average disguises considerable variation. Five of the 11 sectors have 1.3% earnings growth or less. Two are actually declining.

Then there’s energy, where earnings growth is not just above above-average but 61 times more than average.

Needless to say, earnings growth is way out of balance. The energy sector’s big recovery skews the average—remove it and the average drops from 6.5% to 3.6%, according to FactSet.

In other words, almost half of this quarter’s S&P 500 earnings growth originates in a single sector that probably won’t keep growing at its present rate.

Yet money still pours into index ETFs.

Theory, Meet Reality

Keep in mind, these are earnings estimates. We won’t know the real numbers until companies release their quarterly reports, starting next month. But there’s good reason to think they will be lower than many investors expect.

The analysts behind these estimates presumed the average Q2 oil price to be $51.96 per barrel—a pretty optimistic estimate, to say the least. Oil traded below $50 the entire month of June and most of May as well.

Oil and gas producers don’t always sell at the spot price. Some probably hedged at higher prices. Their industry has bigger problems, though.

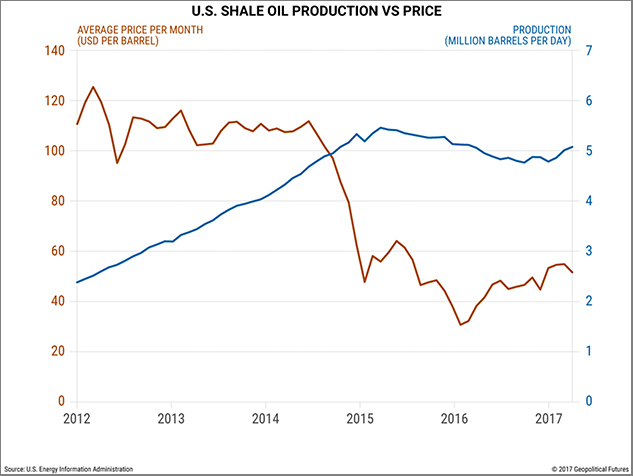

Economic theory tells us that “the cure” for excessively high or low commodity prices is more of the same. High prices encourage more production until, eventually, excess supply makes the price fall. Low prices cause production cuts that reduce supply and ultimately raise prices.

Except that this theory no longer works for the US energy sector, as we see in this chart from Geopolitical Futures:

Oil prices plunged in late 2014, from over $100 to half that level. That should have led to lower production, but it didn’t—hence the present oil glut.

Apparently, the rules have changed.

Technology is a big factor. New exploration and drilling technologies have made production costs fall sharply in the last three years. Many companies can produce oil and gas profitably even at today’s prices or lower.

Some producers are so leveraged, they’ll have to keep pumping even if prices drop further. They need revenue to stay current on their debts.

To be sure, any sudden supply disruption could push prices way up. A hurricane damaging Gulf Coast energy facilities or warfare in the Middle East would do it, at least temporarily. But the broader trends don’t look good if you need oil to stay over $50.

Image: GoFish

While the S&P 500 earnings outlook looks impressive mainly due to a bounced-back energy sector, two other sectors—technology and financial services—look impressive as well. But they depend on energy too.

If oil prices fall enough to hurt the energy sector, some producers will miss loan payments. That would be bad news for the lenders in the financial-services sector.

Likewise, energy companies won’t buy as much hardware and software if they have to cut back on drilling activity. Not good for some technology companies.

Bottom line: the bull market in US stocks will be on even shakier ground if oil prices dip below $40 again. In any case, earnings growth probably won’t continue at current rates unless oil prices climb higher.

Opportunities will still exist—but throwing money into an index ETF isn’t be the way to find them. Millions of investors will learn that lesson the hard way. Don’t be one of them.

Disclosure: Follow Mauldin as he uncovers the truth behind, and beyond, the financial headlines in his free publication, Thoughts ...

more

Disclosure: Follow Mauldin as he uncovers the truth behind, and beyond, the financial headlines in his free publication, Thoughts from the Frontline. The publication explores developments overlooked by mainstream news to help you understand what’s happening in the economy and navigate the markets with confidence.

Copyright 2016. Follow John Mauldin on Twitter.

To subscribe to John Mauldin's Thoughts from the Frontline e-newsletter and a selection of other free newsletters, please click here:& ;

http://www.mauldineconomics.com/subscribe

Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President and registered representative of Millennium Wave Advisors, LLC MWA which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA and SIPC, through which securities may be offered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com (formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC MWA, which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273.

less

thanks