Morning Call For Oct. 9, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 -0.03%) this morning are up +0.14% and European stocks are up +0.29% after Wednesday's dovish minutes from the Sep 16-17 FOMC meeting bolstered speculation the Fed may hold off on raising interest rates. Another positive for stocks is the nearly 3% jump in Alcoa which kicked off the start of Q3 earnings season late yesterday by reporting its highest earnings in 3 years. As expected, the BOE maintained its benchmark interest rate and kept its asset purchase target at 375 billion pounds following the conclusion of its 2-day policy meeting. Asian stocks closed mostly higher: Japan -0.75%, Hong Kong +1.17%, China +0.14%, Taiwan +0.13%, Australia +1.06%, Singapore +1.01%, South Korea closed for holiday, India +1.49%. Japan's Nikkei Stock Index bucked the trend of rallying global stocks and tumbled to a 1-1/4 month low as exporters declined after the yen rose to a 3-week high against the dollar, which dampens exporters' earnings prospects, while China's Shanghai Stock Index pushed up to a 1-1/2 year high after Premier Li Keqiang said the Chinese government will use "targeted measures" to support economic growth. Commodity prices are mixed. Nov crude oil (CLX14 -0.10%) is up +0.07%. Nov gasoline (RBX14 -0.83%) is down -0.69%. Dec gold (GCZ14 +1.95%) is up +1.94% at a 1-1/2 week high as the dollar slides. Dec copper (HGZ14 +1.33%) is up +1.18%. Agriculture and livestock prices are mixed with Dec live cattle up +0.60% at a contract high. The dollar index (DXY00 -0.30%) is down -0.26% at a 2-week low after yesterday's FOMC minutes pushed backed expectations on when the Fed will start to raise interest rates. EUR/USD (^EURUSD) is up +0.24% at a 2-week high. USD/JPY (^USDJPY) is down -0.42% at a 3-week low. Dec T-note prices (ZNZ14 +0.30%) are up 11.5 ticks at a new contract high as the 10-year T-note yield tumbled to a 15-month low of 2.293%.

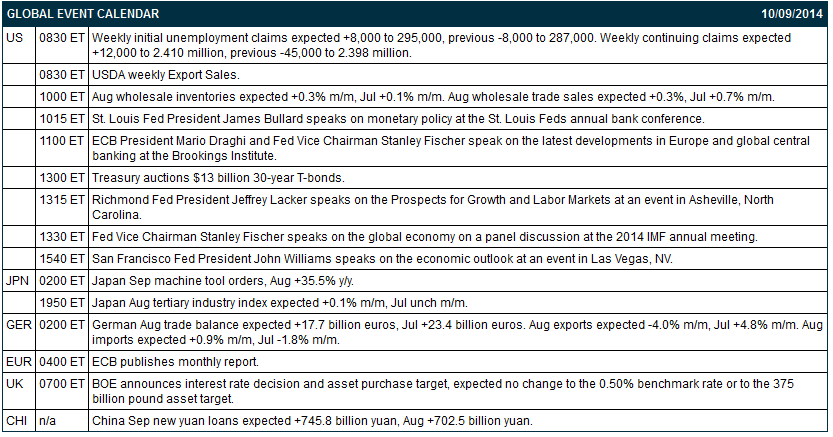

The German Aug trade balance narrowed to a surplus of +14.1 billion euros from a +23.5 billion euros surplus in Jul, narrower than expectations of +17.7 billion euros and the smallest surplus in 8 months. Aug exports fell -5.8% m/m, a larger decline than expectations of -4.0% m/m and the biggest monthly drop in 5-1/2 years. Aug imports unexpectedly fell for a second month s they declined -1.3% m/m, weaker than expectations of +0.9% m/m.

Japan Sep machine tool orders jumped +34.8% y/y, the twelfth consecutive monthly increase.

Japan Aug machine orders rose +4.7% m/m and fell -3.3% y/y, stronger than expectations of +0.5% m/m and -4.9% y/y.

The UK Sep RICS housing market survey price balance fell to 30% from a downward revised 39% in Aug, the lowest in 15 months.

U.S. STOCK PREVIEW

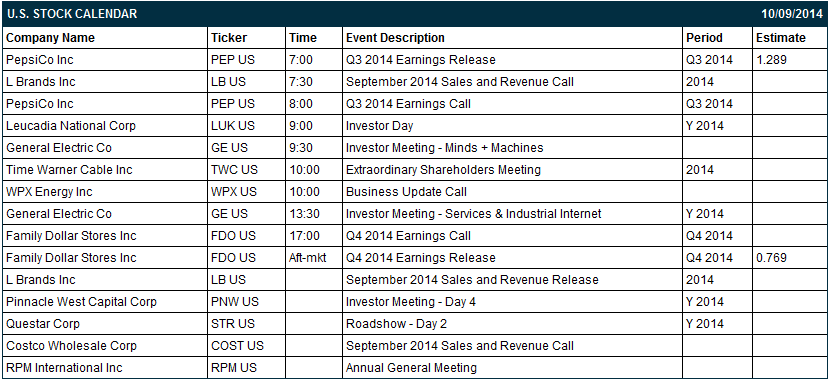

Today’s initial claims report is expected to show an increase of +8,000 to 295,000, exactly offsetting last week’s decline of -8,000 to 287,000. Today's continuing claims report is expected to show an increase of +12,000 to 2.410 million, offsetting part of last week’s decline of -45,000 to 2.398 million. The Treasury today will sell $13 billion of 30-year T-bonds, concluding this week’s $61 billion coupon package. There are two of the Russell 1000 companies that report earnings today: PepsiCo (consensus $1.29), Family Dollar Stores (0.77). Equity conferences during the remainder of this week include: 2014 IIF Annual Membership Meeting on Fri.

OVERNIGHT U.S. STOCK MOVERS

Apple (AAPL +2.08%) was upgraded to 'Outperform' from 'Perform' at Oppenheimer.

Endo (ENDP +3.80%) will acquire Auxilium (AUXL -0.57%) in a cash and stock transaction valued at approximately $2.6 billion.

Toyota Motors (TM +0.38%) was upgraded to 'Buy' from 'Neutral' at BofA/Merrill Lynch.

Colgate-Palmolive (CL +1.42%) was downgraded to 'Market Perform' from 'Outperform' at BMO Capital.

Vulcan Materials (VMC +1.24%) was upgraded to 'Buy' from 'Neutral' at Longbow with a price target of $70.

Men's Wearhouse (MW +1.07%) was initiated with a 'Buy' at Jefferies with a price target of $60.

PepsiCo (PEP +0.90%) reported Q3 EPS of $1.36, better than conensus of $1.29.

Nuance (NUAN +0.41%) rose over 2% in after-hours trading following rumors that Carl Icahn will recommend that Apple buy the company.

Tesoro (TSO +4.13%) was initiated with a 'Buy' at Deutsche Bank with a price target of $81.

Digiies reports that Q3 worldwide PC shipments declined -1.7% on year.

GrubHub (GRUB +2.51%) rose nearly 1% in after-hours trading after it was initiated with a 'Buy' at CRT Capital with a price target of $44.

Karpus Management reported an 8.63% stake in Chase Industries (CSI -0.10%) .

Alcoa (AA +0.75%) jumped nearly 3% in after-hours trading after it reported Q3 adjusted EPS of 31 cents, well above consensus of 23 cents.

Gap (GPS +1.70%) slumped nearly 8% in after-hours trading after the company named Art Peck to succeed Glenn Murphy as CEO.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 -0.03%) this morning are up +2.75 points (+0.14%). The S&P 500 index on Wednesday tumbled to a 2-month low early but recovered in the afternoon and closed sharply higher: S&P 500 +1.75%, Dow Jones +1.64%, Nasdaq +2.08%. Bullish factors included (1) comments from Chicago Fed President Evans who said the Fed should be “exceptionally patient” before they start to raise interest rates, and (2) reduced expectations that the Fed will raise interest rates sooner than expected after the Sep 16-17 FOMC meeting minutes stated that Fed members were worried that a global slowdown and a stronger dollar posed potential risks to the U.S. economy.

Dec 10-year T-notes (ZNZ14 +0.30%) this morning are up +11.5 ticks at a new contract high. Dec 10-year T-note futures prices on Wednesday posted a contract high and closed higher. Bullish factors for T-notes included (1) reduced inflation expectations after the 10-year breakeven inflation expectations rate (i.e., the 10-year T-note yield minus the 10-year TIP yield) fell to a 1-1/4 year low of +1.91%, and (2) the Sep 16-17 FOMC meeting minutes saying that Fed members were concerned that a global slowdown and dollar strength may undercut the U.S. economy. Closes: TYZ4 +12.00, FVZ4 +11.25.

The dollar index (DXY00 -0.30%) this morning is down -0.221 (-0.26%) at a 2-week low. EUR/USD (^EURUSD) is up +0.0030 (+0.24%) and USD/JPY (^USDJPY) is down -0.45 (-0.42%) at a 3-week low. The dollar index on Wednesday fell to a 1-week low and closed lower. Bearish factors included (1) the Sep 16-17 FOMC meeting minutes in which policy makers expressed concern that a global slowdown and a stronger dollar may undercut the U.S. economy, and (2) dovish comments from Chicago Fed President Evans who said the Fed should be “exceptionally patient” before they start to raise interest rates. Closes: Dollar index -0.375 (-0.44%), EUR/USD +0.00649 (+0.51%), USD/JPY +0.053 (+0.05%).

Nov WTI crude oil (CLX14 -0.10%) this morning is up +6 cents (+0.07%) and Nov gasoline (RBX14 -0.83%) is down -0.0161 (-0.69%). Nov crude and Nov gasoline prices on Wednesday closed lower with Nov crude at a 17-1/2 month low and Nov gasoline at a 3-3/4 year low: CLX4 -1.54 (-1.73%), RBXX4-0.0499 (-2.10%). Bearish factors included (1) the +5.01 million bbl increase in weekly EIA crude inventories, more than twice expectations of +2.0 million bbl, (2) the unexpected +1.18 million bbl increase in EIA gasoline inventories, higher than expectations of a -500,000 bbl draw, and (3) the +0.4% increase in U.S. crude production in the week ended Oct 3 to 8.875 million bpd, a new 28-1/2 year high.

Disclosure: None