Morning Call For Wednesday, March 29

OVERNIGHT MARKETS AND NEWS

Jun E-mini S&Ps (ESM17 unch) this morning are little changed, down -0.02%, and European stocks are up +0.08% at a 1-1/4 year high. Strength in crude oil prices is lifting energy producing stocks with May WTI crude oil (CLK17 +0.41%) up +0.45% at a 1 week high on disruptions in Libyan oil output after Libya's NOC said that its crude production fell to 500,000 bpd when a pipeline from the Sharara oil field, the country's biggest, stopped operating. GBP/USD fell -0.10% to a 1-week low and gains in European stocks were muted ahead of the expected signing of Article 50 of the Lisbon Treaty by UK Prime Minister May that will begin the exit of the UK from the European Union. Another negative is the potential breakup of the UK as Scotland may use Brexit and start a referendum in their push for autonomy from England. Asian stocks settled mixed: Japan +0.08%, Hong Kong +0.19%, China -0.36%, Taiwan -0.20%, Australia +0.90%, Singapore +0.85%, South Korea +0.22%, India +0.41%. Chinese stocks retreated as property stocks fell on concern the government will start imposing tighter property controls to keep the housing market from a bubble.

The dollar index (DXY00 +0.09%) is up +0.15%. EUR/USD (^EURUSD) is down -0.26%. USD/JPY (^USDJPY) is down -0.16%.

Jun 10-year T-note prices (ZNM17 +0.06%) are unchanged.

The German Feb import price index rose +0.7% m/m and +7.4% y/y, stronger than expectations of +0.4% m/m and +7.0% y/y with the +7.4%y/y gain the largest year=on-year increase in 5-3/4 years.

Japan Feb retail sales rose +0.2% m/m and +0.1% y/y, weaker than expectations of +0.3% m/m and +0.7% y/y.

U.S. STOCK PREVIEW

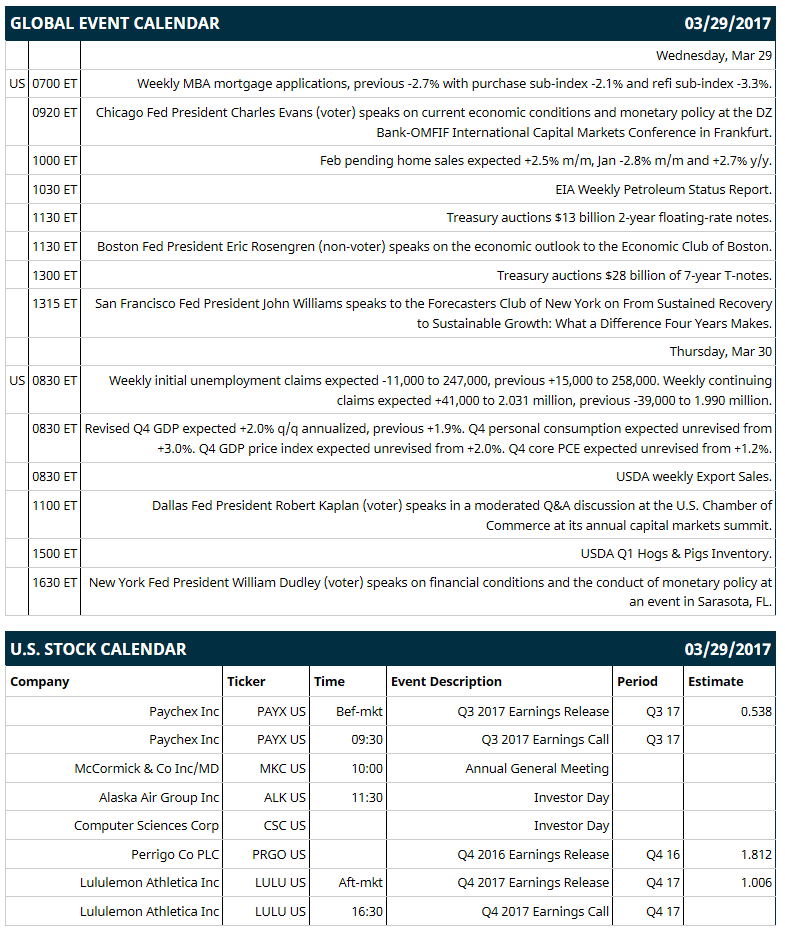

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -2.7% with purchase sub-index -2.1% and refi sub-index -3.3%), (2) Chicago Fed President Charles Evans (voter) speaks on current economic conditions and monetary policy at the DZ Bank-OMFIF International Capital Markets Conference in Frankfurt, (3) Feb pending home sales (expected +2.5% m/m, Jan -2.8% m/m and +2.7% y/y), (4) Treasury auctions $13 billion 2-year floating-rate notes, (5) Boston Fed President Eric Rosengren (non-voter) speaks on the economic outlook to the Economic Club of Boston, (6) Treasury auctions $28 billion of 7-year T-notes, (7) San Francisco Fed President John Williams speaks to the Forecasters Club of New York on “From Sustained Recovery to Sustainable Growth: What a Difference Four Years Makes,” (8) EIA Weekly Petroleum Status Report.

Notable Russell 1000 earnings reports today include: Paychex (consensus $0.54), Perrigo (1.81), Lululemon (1.01).

U.S. IPO's scheduled to price today: none.

Equity conferences: Jefferies Animal Health Summit on Thu.

OVERNIGHT U.S. STOCK MOVERS

Groupon (GRPN +0.25%) and Twitter (TWTR -0.33%) both fell 1% in pre-market trading after Barclays PLC initiated coverage on the Internet sector with 'Underweight' ratings for both stocks.

CyberArk Software (CYBR unch) was upgraded to 'Outperform' from 'Neutral' at Evercore ISI with a price target of $60.

RH (RH +3.57%) surged 15% in after-hours trading after it forecast Q1 net revenue of $530 million-$545 million, above consensus of $485.1 million

Computer Sciences (CSC +1.50%) gained 1% in after-hours trading after it was announced that it will replace Southwestern Energy in the S&P 500 before the open of trading on Tuesday, April 4.

Wells Fargo (WFC +1.03%) reached an agreement in principle to pay $1110 million to settle a class action lawsuit concerning retail sales practices over fake accounts.

Dave & Buster's Entertainment (PLAY +2.34%) fell over 3% in after-hours trading after it reported Q4 comparable sales rose +3.2%, below consensus of +3.7%.

Ollie's Bargain Outlet Holdings (OLLI +0.46%) rose 3% in after-hours trading after it reported Q4 net sales of $283.4 million, higher than consensus of $281 million.

Western Union (WU +0.60%) was downgraded to 'Sell' from 'Hold' at Edward Jones.

Sonic (SONC +2.44%) lost nearly 3% in after-hours trading after it reported Q3 revenue of $100.2 million, weaker than consensus of $104.6 million and said Q2 system-wide comparable sales fell -7.4%, a bigger decline than consensus of -4.5%.

Landex (LNDC +0.87%) said it sees Q4 EPS of 9 cents-11 cents, well below consensus of 21 cents.

Depomed (DEPO -4.50%) slid 4% in after-hours trading after it said it sees Q1 net sales of $95 million-$100 million, below consensus of $114.7 million.

Laureate Education (LAUR +2.51%) reported Q4 EPS of 27 cents, well above consensus of 12 cents.

Verint Systems (VRNT -1.13%) jumped 8% in after-hours trading after it reported Q4 adjusted EPS of 90 cents, better than consensus of 86 cents.

Orexigen Therapeutics (OREX +2.66%) dropped 7% in after-hours trading after it reported a Q4 loss per share of -$1.69, much wider than consensus of -86 cents.

Pernix Therapeutics Holdings (PTX -2.64%) tumbled nearly 10% in after-hours trading after it said it continues to analyze various alternatives, including strategic and refinancing alternatives, to improve financial flexibility.

MARKET COMMENTS

Jun E-mini S&Ps (ESM17 unch) this morning are down -0.50 points (-0.02%). Tuesday's closes: S&P 500 +0.73%, Dow Jones +0.73%, Nasdaq +0.61%. The S&P 500 on Tuesday closed higher on the unexpected +9.5 point increase in U.S. Mar consumer confidence (Conference Board) to 125.6 (stronger than expectations of -0.8 to 114.0 and the highest in 16-1/4 years) and the unexpected +5 point increase in the Mar Richmond Fed manufacturing index to 22 (stronger than expectations of -2 to 15 and the fastest pace of expansion in 6-3/4 years). Energy producer stocks rallied due to the +1.3% rally in crude oil prices.

Jun 10-year T-notes (ZNM17 +0.06%) this morning are unch. Tuesday's closes: TYM7 -10.-0, FVM7 -7.00. Jun 10-year T-notes on Tuesday closed lower on the unexpected increase in U.S. Mar consumer confidence to a 16-1/4 year high and on reduced safe-haven demand with the strength in stocks.

The dollar index (DXY00 +0.09%) this morning is up +0.145 (+0.15%). EUR/USD (^EURUSD) is down -0.0028 (-0.26%) and USD/JPY (^USDJPY) is down -0.18 (-0.16%). Tuesday's closes: Dollar index +0.546 (+0.55%), EUR/USD -0.0050 (-0.46%), USD/JPY +0.49 (+0.44%). The dollar index on Tuesday closed higher on the unexpected increase in U.S. Mar consumer confidence to a 16-1/4 year high (+9.5 to 125.6) and on weakness in EUR/USD after ECB Executive Board member Praet said that it's too soon to start discussing when to withdraw stimulus.

May WTI crude oil prices (CLK17 +0.41%) this morning are up +22 cents (+0.45%) at a 1-week high and May gasoline (RBK17 +0.75%) is +0.0105 (+0.64%). Tuesday's closes: May crude +0.64 (+1.34%), May gasoline +0.0101 (+0.62%). May crude oil and gasoline on Tuesday closed higher with May gasoline at a 2-week high. Crude oil prices were boosted by the action by Libya's NOC to declare force majeure on loadings of Sharara crude from its Zawiya oil terminal after it closed its pipeline from the Sharara field, its biggest pipeline. Crude oil prices were undercut by expectations for EIA crude inventories to climb +2.0 million bbl on Wednesday.

(Click on image to enlarge)

Disclosure: None.