Morning Call For Wednesday, March 1

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 +0.51%) this morning are up +0.44% at a new all-time nearest-futures high and European stocks are up +1.57% at a 14-1/2 month high on signs of global economic strength. President Trump's address to Congress last night turned out to be a non-event as it lacked specifics on his tax cut plans or details on infrastructure spending. Global stocks rallied after Chinese manufacturing activity unexpectedly expanded last month and Eurozone manufacturing activity remained at a 3-year high. Mining stocks and raw-material producers also moved higher as May copper (HGK17 +1.11%) climbed +1.34% to a 1-week high on expectations of stronger global demand for commodities. Asian stocks settled mostly higher: Japan +1.44%, Hong Kong +0.15%, China +0.16%, Taiwan -0.78%, Australia -0.13%, Singapore +0.84%, South Korea closed for holiday, India +0.84%. Asian stocks found support on signs of strength in Chinese manufacturing activity, while Japanese exporter stocks also garnered support from a slide in the yen as USD/JPY rose +0.88% to a 1-1/2 week high, which boosts the earnings prospects of exporters.

The dollar index (DXY00 +0.74%) is up +0.66% at a 1-1/2 month high as hawkish Fed commentary late yesterday boosted the odds of a Mar Fed rate hike. EUR/USD (^EURUSD) is down -0.41%. USD/JPY (^USDJPY) is up +0.88% at a 1-1/2 week high.

Jun 10-year T-note prices (ZNM17 -0.61%) are down -21.5 ticks.

St. Louis Fed President Bullard (non-voter) said he's "agnostic" about when to raise the fed funds rate and that being pre-emptive "would be overkill" as he "doesn't think the fiscal uncertainty will be resolved before summer."

The China Feb manufacturing PMI unexpectedly rose +0.3 to 51.6, stronger than expectations of -0.1 to 51.2.

The Eurozone Feb Markit manufacturing PMI was revised downward to 55.4 from the originally reported 55.5, still the fastest pace of expansion since the data series began in 2014.

Japan Q4 capital spending rose +3.8% y/y, stronger than expectations of +0.8% y/y. Q4 capital spending ex-software rose 3.3% y/y, stronger than expectations of +1.1% y/y.

U.S. STOCK PREVIEW

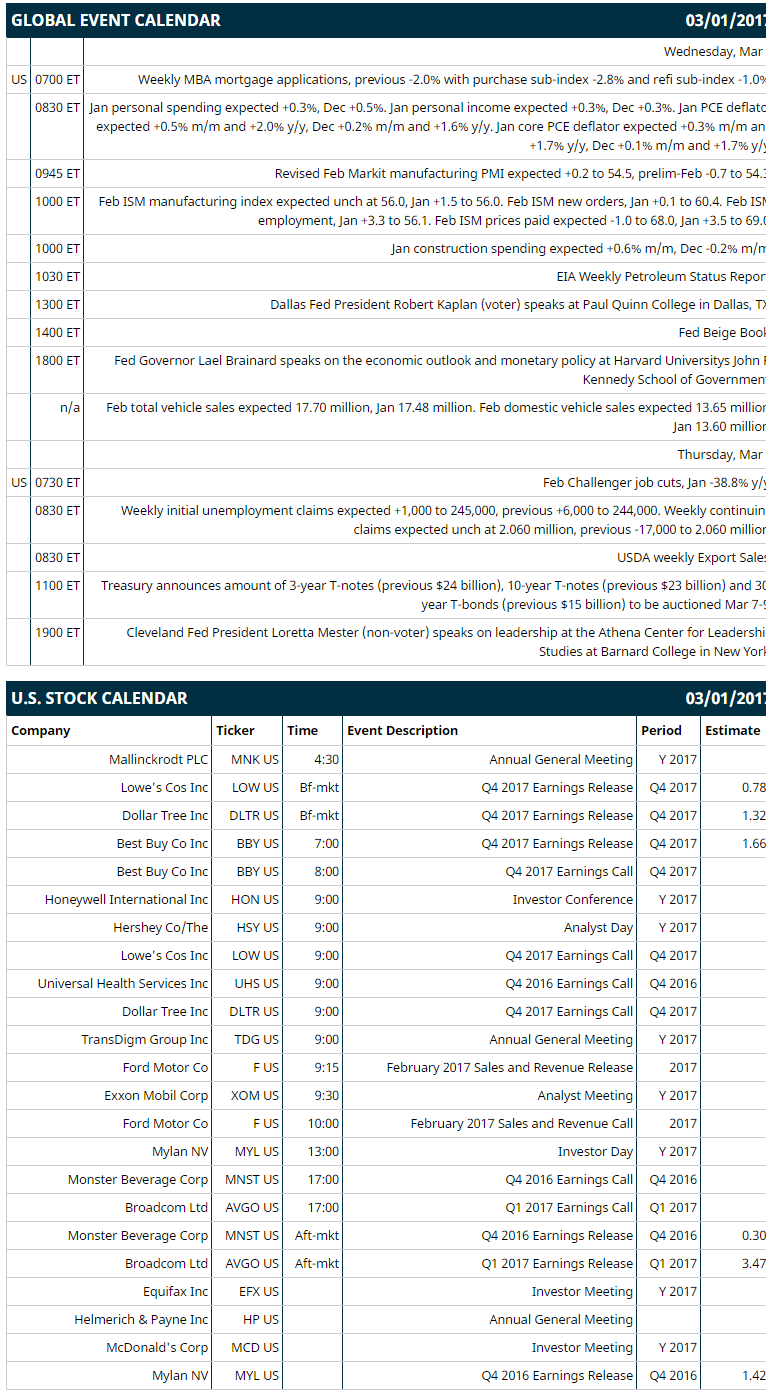

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -2.0% with purchase sub-index -2.8% and refi sub-index -1.0%), (2) Jan personal spending (expected +0.3%, Dec +0.5%) and Jan personal income (expected +0.3%, Dec +0.3%), (3) Jan PCE deflator (expected +0.5% m/m and +2.0% y/y, Dec +0.2% m/m and +1.6% y/y) and Jan core PCE deflator (expected +0.3% m/m and +1.7% y/y, Dec +0.1% m/m and +1.7% y/y), (4) revised Feb Markit manufacturing PMI (expected +0.2 to 54.5, prelim-Feb -0.7 to 54.3), (5) Feb ISM manufacturing index (expected +0.2 to 56.2, Jan +1.5 to 56.0), (6) Jan construction spending (expected +0.6% m/m, Dec -0.2% m/m), (7) Dallas Fed President Robert Kaplan (voter) speaks at Paul Quinn College in Dallas, TX, (8) Fed Beige Book, (9) Fed Governor Lael Brainard speaks on the economic outlook and monetary policy at Harvard University’s John F. Kennedy School of Government, (10), Feb total vehicle sales (expected 17.70 million, Jan 17.48 million), (11) EIA Weekly Petroleum Status Report.

Notable S&P 500 earnings reports today include: Best Buy (consensus $1.67), Lowe's (0.79), Dollar Tree (1.32), Monster Beverage (0.30), Broadcom (3.48), Mylan (1.42).

U.S. IPO's scheduled to price today: Snap (SNAP).

Equity conferences: CITI Asset Management, Broker Dealer & Market Structure Conference on Wed, Gabelli & Company Pump, Valve & Water Systems Symposium on Wed, Wells Fargo Real Estate Securities Conference on Wed, ABA National Conference on Wed, EnerCom The Oil & Gas Conference on Wed, J.P. Morgan Gaming, Lodging, Restaurant & Leisure Management Access Forum on Thu, Bank of America Merrill Lynch Global Agriculture and Chemicals Conference on Wed-Thu, BTIG Healthcare Conference on Thu, Capital Link Master Limited Partnership Investing Forum on Thu, Simmons Energy Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Micron (MU -1.35%) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs with a price target of $29.

Allstate (ALL +1.01%) was downgraded to 'Market Perform' from 'Outperform' at Keefe, Bruyette & Woods with a 12-month target price of $81.

William Lyon Homes (WLH -2.28%) rose 3% in after-hours trading after it was announced that it will replace Arctic Cat in the S&P SmallCap 600 at the opening of trade on Monday, March 6.

Intel (INTC -0.85%) was downgraded to 'Underperform' from 'Market Perform' at Bernstein with a 12-month target price of $30

salesforce.com (CRM -0.23%) slid over 1% in after-hours trading after it said it sees full-year revenue of $10.15 billion-$10.20 billion, below consensus of $10.20 billion.

Tesaro (TSRO +0.51%) lost 1% in after-hours trading after it reported a Q4 loss of -$2.60 a share, wider than consensus of -$1.95.

Palo Alto Networks (PANW -1.33%) slumped nearly 20% in after-hours trading after it said it sees Q3 revenue of $406 million-$416 million, below consensus of $454.6 million.

Weight Watchers International (WTW +9.93%) jumped over 8% in after-hours trading after it reported Q4 EPS of 20 cents, better than consensus of 19 cents, and said it sees full-year EPS of $1.30-$1.40, above consensus of $1.17.

Darling Ingredients (DAR +1.64%) rallied over 6% in after-hours trading after it reported Q4 EPS of 25 cents, above consensus of 19 cents.

Veeva Systems (VEEV -1.02%) fell nearly 2% in after-hours trading after it forecast fiscal 2018 EPS of 78 cents-80 cents, below consensus of 80 cents.

TASER International (TASR -1.57%) gained over 1% in after-hours trading after it reported Q4 EPS of 12 cents, better than consensus of 10 cents.

CyberOptics (CYBE -1.01%) sank over 10% in after-hours trading after it reported Q4 revenue of $13.50 million, less than consensus of $14.21 million.

Builders FirstSource (BLDR +0.94%) climbed nearly 6% in after-hours trading after it reported Q4 net sales of $1.55 billion, higher than consensus of $1.50 billion.

Chuy's Holdings (CHUY +0.88%) fell over 3% in after-hours trading after it reported Q4 EPS of 14 cents, below consensus of 17 cents, and said it sees full-year EPS of $1.11 to $1.15, weaker than consensus of $1.19.

Big 5 Sporting Goods (BGFV -2.89%) jumped over 13% in after-hours trading after it said it sees Q1 EPS of 12 cents-18 cents, well above consensus of 6 cents.

Dynavax (DVAX +2.27%) surged over 20% in after-hours trading after it announced the FDA will review Dynavax's responses to the Complete Response Letter issued by the FDA in Nov 2016 for the Biologics License Application for HEPLISAV-B, Dynavax's vaccine for immunization against hepatitis B infection in adults 18 years and older.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 +0.51%) this morning are up +10.50 points (+0.44%) at a fresh record nearest-futures high. Tuesday's closes: S&P 500 -0.26%, Dow Jones -0.12%, Nasdaq -0.32%. The S&P 500 on Tuesday closed lower on the unrevised U.S. Q4 GDP of +1.9% (weaker than expectations of +2.1%) and some long liquidation ahead of President Trump's address to Congress on Tuesday night. Stocks were supported by the unexpected +3.2 increase in U.S. Feb consumer confidence (Conference Board) to 114.8 (stronger than expectations of -0.8 to 111.0 and a 15-1/2 year high) and the +7.1-point increase in the Feb Chicago PMI to 57.4 (stronger than expectations of +3.2 to 53.5 and the fastest pace of expansion in 2 years).

Jun 10-year T-notes (ZNM17 -0.61%) this morning are down -21.5 ticks. Tuesday's closes: TYM7 -0.50, FVM7 -2.75. Jun 10-year T-notes on Tuesday closed slightly lower on comments from New York Fed President Dudley (voter) who said the case for tightening had become "a lot more compelling" in recent months and on the +3.2 increase in U.S. Feb consumer confidence to 114.8, a 15-1/2 year high. Losses were limited after U.S. Q4 GDP was left unrevised at +1.9%, weaker than expectations of +2.1%.

The dollar index (DXY00 +0.74%) this morning is up +0.67 (+0.66%) at a 1-1/2 month high. EUR/USD (^EURUSD) is down -0.0043 (-0.41%). USD/JPY (^USDJPY) is up +0.99 (+0.88%) at a 1-1/2 week high. Tuesday's closes: Dollar index -0.01 (-0.01%), EUR/USD -0.0011 (-0.10%), USD/JPY +0.58 (+0.52%). The dollar index on Tuesday closed lower on the weaker-than-expected U.S. Q4 GDP report and long liquidation in the dollar ahead of President Trump's speech to Congress on Tuesday night. Losses were limited after New York Fed President Dudley said the case for tightening had become "a lot more compelling" in recent months.

Apr WTI crude oil prices (CLJ17 +0.26%) this morning are up +13 cents (+0.24%) and Apr gasoline (RBJ17 -1.14%) is -0.0205 (-1.19%). Tuesday's closes: Apr crude -0.04 (-0.07%), Apr gasoline -0.0123 (-0.71%). Apr crude oil and gasoline on Tuesday closed lower on the prediction from JBC Energy GmgH that OPEC Feb crude production rose by +55,000 bpd to 32.245 million bpd and by expectations that Wednesday's weekly EIA data will show U.S. crude inventories rose by +3.0 million bbl.

Disclosure: None.