Morning Call For Wednesday, June 14

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU17 +0.12%) this morning are up +0.11% and European stocks are up +0.81% as strength in technology stocks leads the overall market higher. Optimism in the global economy is another positive for equity prices after the IMF raised its China 2017 GDP estimate to 6.7% from a 6.6% estimate in Apr. European stocks also found support after data showed Eurozone Q1 employment rose +1.5% y/y, the largest increase in 9-years. Weakness in energy stocks limited gains in the overall market as Jul WTI crude oil (CLN17 -1.23%) slid -1.08% after API data late Tuesday showed U.S. crude inventories rose +2.75 million bbl last week. Trading activity was light ahead of the conclusion of today's FOMC meeting where the Fed is expected to raise the fed funds target range by 25 bp, but the markets will look to future Fed guidance and when it may begin to reduce its balance sheet. Asian stocks settled mostly lower: Japan -0.08%, Hong Kong +0.09%, China -0.73%, Taiwan -0.55%, Australia +1.06%, Singapore -0.13%, South Korea -0.02%, India +0.17%.

The dollar index (DXY00 +0.09%) is up +0.07%. EUR/USD (^EURUSD) is down -0.09%. USD/JPY (^USDJPY) is up +0.18%.

Sep 10-year T-note prices (ZNU17 +0.02%) are up +3 ticks.

The International Monetary Fund (IMF) raised its China 2017 GDP estimate to 6.7% from a 6.6% estimate in Apr.

China May industrial production rose +6.5% y/y, unch from Apr and stronger than expectations of +6.4% y/y.

Eurozone Apr industrial production rose +0.5% m/m and +1.4% y/y, right on expectations.

Eurozone Q1 employment rose +0.4% q/q and +1.5% y/y with the +1.5% y/y gain the largest year-on-year increase in 9 years.

U.S. STOCK PREVIEW

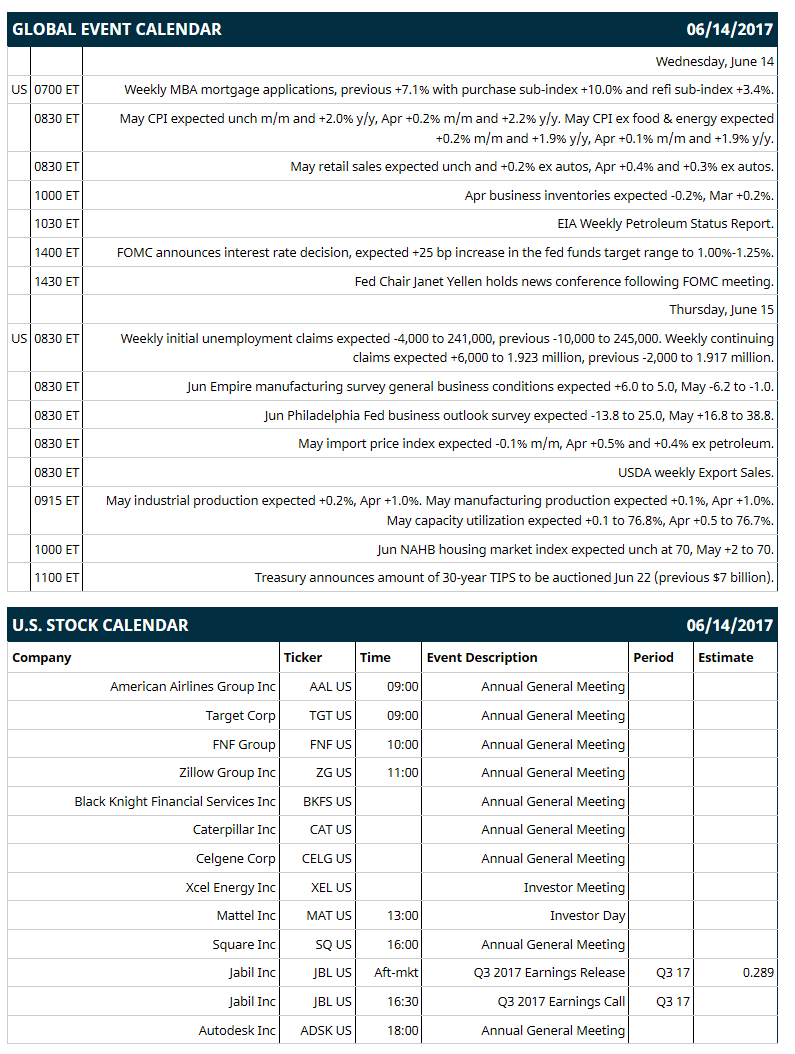

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +7.1% with purchase sub-index +10.0% and refi sub-index +3.4%), (2) May CPI (expected unch m/m and +2.0% y/y, Apr +0.2% m/m and +2.2% y/y) and May CPI ex food & energy (expected +0.2% m/m and +1.9% y/y, Apr +0.1% m/m and +1.9% y/y), (3) May retail sales (expected +0.1% and +0.1% ex autos, Apr +0.4% and +0.3% ex autos), (4) Apr business inventories (expected -0.1%, Mar +0.2%), (5) FOMC announces interest rate decision with expected +25 bp increase in the fed funds target range to 1.00%-1.25%, (6) EIA Weekly Petroleum Status Report.

Notable Russell 2000 earnings reports today include: Jabil (consensus $0.29).

U.S. IPO's scheduled to price today: Boston Omaha (BOMN), Avenue Therapeutics (ATXI).

Equity conferences: Citi Industrials Conference on Tue-Wed, Morgan Stanley Financial Services Conference on Tue-Wed, William Blair & Company Growth Stock Conference on Tue-Thu, Deutsche Bank dbAccess Global Consumer Conference on Tue-Thu, Golddman Sachs European Payment Conference on Tue-Thu, Goldman Sachs Global Health Care Conference on Tue-Thu, Piper Jaffray Consumer Conference on Wed, Vertical Research Partners Materials Conference on Wed, RBC Capital Markets Financial Technology Investor Day on Wed, Drexel Hamilton Aerospace & Defense Conference on Thu, Stifel, Nicolaus & Co Industrials Conference on Thu, NASDAQ Investor Program on Thu.

OVERNIGHT U.S. STOCK MOVERS

Restaurant Brands International (QSR +0.68%) was upgraded to 'Outperform' from 'Market Perform' at Oppenheimer.

Infinera (INFN +1.20%) was upgraded to 'Buy' from 'Neutral' at MKM Partners with a price target of $14.

Starbucks (SBUX -0.60%) was downgraded to 'Neutral' from 'Outperform' at Wedbush.

HMS Holdings (HMSY +0.31%) was initiated with an 'Overweight' rating at Cantor Fitzgerald with a 12-month target price of $23.

Janus Henderson Group PLC (JHG +1.39%) was initiated with an 'Overweight' rating at Morgan Stanley.

Alexion Pharmaceuticals (ALXN +1.05%) rose 4% in after-hours trading after it announced that Biogen CFO Paul Clancy will be the new CFO at Alexion effective July 31. Biogen (BIIB -0.26%) dropped over 2% in after-hours trading on the news.

Loxo Oncology (LOXO -3.66%) lost over 2% in after-hours trading after it announced that it intends to offer shares of its common stock in an underwritten public offering, although no size was given.

H&R Block (HRB +2.08%) jumped over 11% in after-hours trading after it reported Q4 adjusted EPS from continuing operations of $3.76, better than consensus of $3.53.

FTD Cos (FTD -3.51%) was initiated with a 'Buy' at DA Davidson with a 12-month target price of $23.

Gladstone Investment Corp (GAIN +0.33%) was rated a new 'Outperform' at Wedbush with a 12-month target price of $10.

Sequans Communications SA (SQNS unch) dropped over 5% in after-hours trading after it announced that it intends to offer newly issued American Depositary Shares (ADSs) representing ordinary shares in an underwritten public offering, although no size was given.

MARKET COMMENTS

Sep E-mini S&Ps (ESU17 +0.12%) this morning are up +2.75 points (+0.11%). Tuesday's closes: S&P 500 +0.45%, Dow Jones +0.44%, Nasdaq +0.76%. The S&P 500 on Tuesday closed higher on a rebound in technology stocks after 2 days of sharp losses and on strength in energy stocks after crude prices rose +0.82%. Gains were limited ahead of the outcome of the 2-day FOMC meeting on Wednesday where the Fed is expected to raise its fed funds rate target by 25 bp.

Sep 10-year T-notes (ZNU17 +0.02%) this morning are up +3 ticks. Tuesday's closes: TYU7 +1.50, FVU7 unch. Sep 10-year T-notes on Tuesday closed higher on weaker inflation expectations after the 10-year T-note breakeven inflation rate fell to a 7-month low. There was also decent demand for the Treasury's $12 billion auction of 30-year T-bonds that had a bid-to-cover ratio of 2.32, above the 12-auction average of 2.30. T-note prices were undercut by rising producer price pressures after U.S. May core PPI rose +2.1% y/y, stronger than expectations of +1.9% y/y and the largest year-on-year increase in 3 years.

The dollar index (DXY00 +0.09%) this morning is up +0.07 (+0.07%). EUR/USD (^EURUSD) is down -0.0010 (-0.09%) and USD/JPY (^USDJPY) is up +0.20 (+0.18%). Tuesday's closes: Dollar index -0.163 (-0.17%), EUR/USD +0.0008 (+0.07%), USD/JPY +0.12 (+0.11%). The dollar index on Tuesday closed lower on reduced inflation expectations that may slow the pace of Fed tightening after the 10-year T-note breakeven inflation rate dropped to a 7-month low.

Jul WTI crude oil prices (CLN17 -1.23%) this morning are down -50 cents (-1.08%) and July gasoline (RBN17 -1.25%) is -0.0165 (-1.10%). Tuesday's closes: Jul crude +0.38 (+0.82%), Jul gasoline +0.0115 (+0.77%). Jul crude oil and gasoline on Tuesday closed higher on a weaker dollar and on expectations that Wednesday's weekly EIA data will show U.S. crude inventories fell -2.4 million bbl. Crude oil prices were undercut by speculation that increased U.S. oil production will offset OPEC crude production cuts and the projection from the EIA for U.S. Jul shale oil output to increase by +127,000 bpd.

(Click on image to enlarge)

Disclosure: None.