Morning Call For Wednesday, Feb. 1

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 +0.23%) are up +0.19% and European stocks are up +0.90%. Optimism about corporate earnings is lifting stock indexes this morning with Apple up 3% in pre-market trading after it reported better-than-expected quarterly earnings results after the market closed on Tuesday. Although expectations are for no change in monetary policy after today's FOMC meeting, the markets will parse the post-FOMC statement for any change in forward guidance as to when the Fed may next raise interest rates. European stocks received an added boost after the Eurozone Jan Markit manufacturing PMI was revised upward to the fastest pace of expansion since the data series began in 2014. Asian stocks settled mostly higher: Japan +0.56%, Hong Kong -0.18%, Australia +0.57%, Singapore +0.68%, South Korea +0.55%, India +1.76%. China and Taiwan were closed for holiday. Japan's Nikkei Stock Index recovered from a 1-week low and closed higher as strength in USD/JPY boosted exporter stocks.

The dollar index (DXY00 +0.06%) is up +0.06%. EUR/USD (^EURUSD) is unchanged. USD/JPY (^USDJPY) is up +0.41%.

Mar 10-year T-note prices (ZNH17 -0.14%) are down -4.5 ticks.

The Eurozone Jan Markit manufacturing PMI was revised upward to 55.2 from the originally reported 55.1, the fastest pace of expansion since the data series began in 2014.

The China Jan manufacturing PMI fell -0.1 to 51.3, stronger than expectations of -0.2 to 51.2.

The Japan Jan Nikkei manufacturing PMI was revised downward to 52.7 from the originally reported 52.8, still the fastest pace of expansion in 2-3/4 years.

U.S. STOCK PREVIEW

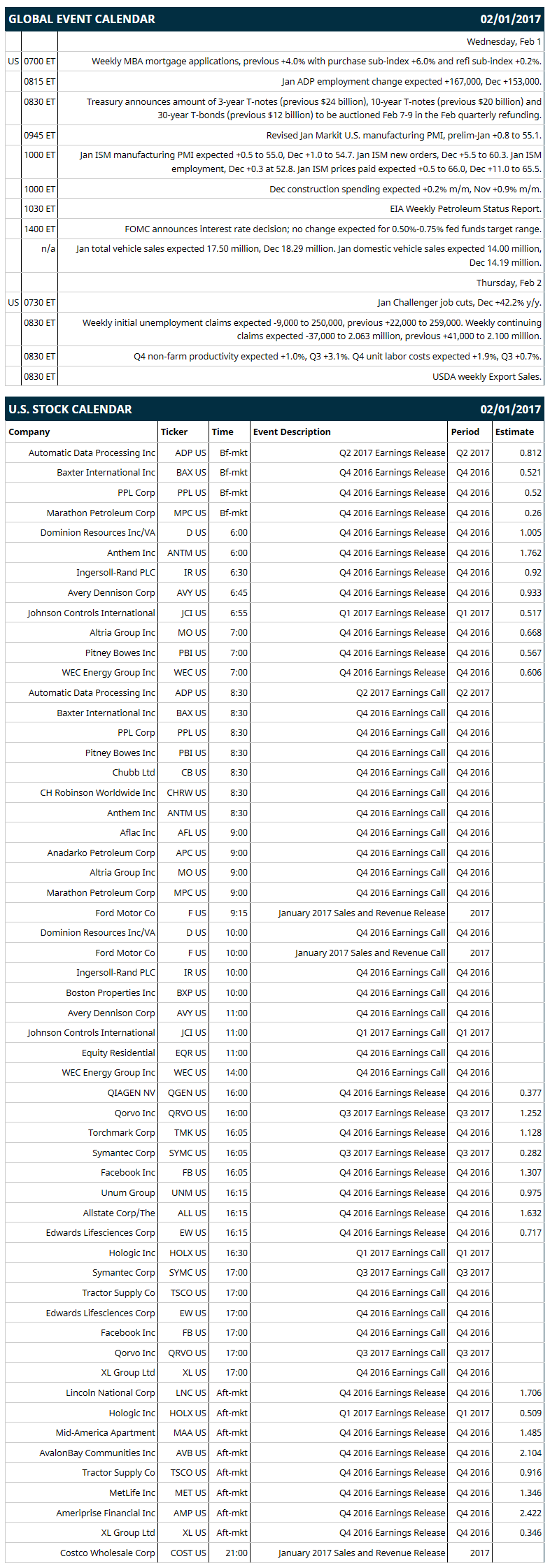

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +4.0% with purchase sub-index +6.0% and refi sub-index +0.2%), (2) Jan ADP employment (expected +167,000, Dec +153,000), (3) revised Jan Markit U.S. manufacturing PMI (prelim-Jan +0.8 to 55.1), (4) Jan ISM manufacturing PMI (expected +0.5 to 55.0, Dec +1.0 to 54.7), (5) Dec construction spending (expected +0.2% m/m, Nov +0.9% m/m), (6) FOMC announces policy decision (no change expected for 0.50%-0.75% fed funds target range), (7) Jan total vehicle sales (expected 17.50 million, Dec 18.29 million), (8) EIA Weekly Petroleum Status Report.

U.S. IPO's scheduled to price today: Kimbell Royalty Partners (KRP), IC Power Pte Ltd (ICP), Ramaco Resources (METC).

Equity conferences: none.

OVERNIGHT U.S. STOCK MOVERS

Apple (AAPL -0.23%) rose 3% in pre-market trading after it reported Q1 EPS of $3.36, higher than consensus of $3.22, and said it sold 78.3 million iPhone units, above consensus of 76.3 million.

Marathon Oil (MRO +1.33%) was upgraded to 'Sector Outperform' from 'Sector Perform' at Scotia Howard Weil with a target price of $25.

Illumina (ILMN +0.51%) lost 1% in after-hours trading after it said it sees Q1 revenue of $580 million to $595 million, below consensus of $615.3 million.

U.S. Steel (X -0.88%) lost almost 1% in after-hours trading after it reported Q4 net sales of $2.65 billion, below consensus of $2.66 billion.

Align Technology (ALGN +1.90%) gained 2% in after-hours trading after it said it sees Q1 net revenue of $295 million to $298 million, above consensus of $293.5 million.

Manhattan Associates (MANH +0.06%) fell 5% in after-hours trading after it said it sees fiscal 2017 adjusted EPS of $1.89 to $1.93, below consensus of $2.02.

Carbonite (CARB +2.37%) rose nearly 3% in after-hours trading after it reported Q4 preliminary non-GAAP EPS of 10 cents-13 cents, higher than consensus of 10 cents. It also purchased Double-Take for $65.3 million in cash and stock.

Under Armour (UA -25.74%) was downgraded to 'Underperform' from 'Neutral' at Credit Suisse.

Overstock.com (OSTK unch) surged over 13% in after-hours trading after it reported Q4 EPS of 12 cents versus zero y/y and Q4 revenue of $526.2 million versus $480.3 million y/y.

Advanced Micro Devices (AMD -2.26%) climbed nearly 5% in after-hours trading after it reported Q4 revenue of $1.11 billion, better than consensus of $1.07 billion.

Match Group (MTCH -0.52%) dropped nearly 8% in after-hours trading after it said it sees Q1 revenue of $287 million-$297 million, well below consensus of $330.2 billion.

Sanchez Energy (SN -1.49%) slid 3% in after-hours trading after it announced a public offering of 10 million shares of common stock.

Boot Barn Holdings (BOOT +3.43%) sank nearly 10% in after-hours trading after it cut its fiscal 2017 EPS estimate to 60 cents-63 cents from an Oct 26 projection of 66 cents-73 cents, below consensus of 68 cents.

Synergy Pharmaceuticals (SGYP +8.10%) sank over 10% in after-hours trading after it announced a public offering of $125 million of common stock.

Catabasis Pharmaceuticals (CATB +2.80%) plunged over 60% in after-hours trading after part B of the MoveDMD trial of its edasalonexent (CAT-1004) for treatment of Duchenne muscular dystrophy failed to meet its primary endpoint.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 +0.23%) this morning are up +4.25 points (+0.19%). Tuesday's closes: S&P 500 -0.09%, Dow Jones -0.54%, Nasdaq -0.24%. The S&P 500 on Tuesday moved lower for a third day and closed slightly lower on the -1.5-point decline in U.S. Jan consumer confidence (Conference Board) to 111.8 (weaker than expectations of -0.9 to 112.8) and on the unexpected -3.6 point drop in the Jan Chicago PMI to 50.3 (weaker than expectations of +0.4 to 55.0 and the slowest pace of expansion in 8 months).

Mar 10-year T-notes (ZNH17 -0.14%) this morning are down -4.5 ticks. Tuesday's closes: TYH7 +8.00, FVH7 +3.75. Mar 10-year T-notes on Tuesday closed higher on the unexpected decline in the Jan Chicago PMI (-3.6 to 50.3) to an 8-month low and on increased safe-haven demand with the slide in stocks.

The dollar index (DXY00 +0.06%) this morning is up +0.061 (+0.06%). EUR/USD (^EURUSD) is unch. USD/JPY (^USDJPY) is up +0.46 (+0.41%). Tuesday's closes: Dollar index -0.854 (-0.85%), EUR/USD +0.0103 (+0.96%), USD/JPY -0.97 (-0.85%). The dollar index on Tuesday tumbled to a 2-1/2 month low and closed lower on a surge in EUR/USD to a 1-1/2 month high after the Financial Times reported that Peter Navarro, the Trump administration’s chief trade advisor, said the euro was "grossly undervalued."

Mar WTI crude oil prices (CLH17 +0.74%) this morning are up +34 cents (+0.64%) and Mar gasoline (RBH17 +1.45%) is +0.0177 (+1.14%). Tuesday's closes: Mar crude +0.18 (+0.34%), Mar gasoline +0.0170 (+1.11%). Mar crude oil and gasoline on Tuesday closed higher on the slump in the dollar index to a 2-1/2 month low and the shutdown of the 400,000 bpd Legacy pipeline after it was damaged by road workers, which reduces the flow of crude from Cushing to the Gulf Coast. Gains were limited on expectations that Wednesday’s EIA data will show U.S. crude inventories rose +3.0 million bbl.

(Click on image to enlarge)

Disclosure: None.