Morning Call For Wednesday, Feb. 15

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 -0.03%) are down -0.06% on light profit-taking after climbing to a new record nearest-futures high in overnight trade. European stocks are up +0.42% at a 2-1/2 week high on strength in bank stocks. U.S. stock indexes were undercut by a -0.68% decline in Mar WTI crude oil (CLH17 -0.60%) prices, which has put pressure on energy producing stocks. Crude oil fell back after the API reported late yesterday that U.S. crude inventories rose 9.94 million bbl last week. Asian stocks settled mostly higher: Japan +1.03%, Hong Kong +1.23%, China -0.15%, Taiwan +0.83%, Australia +0.94%, Singapore +0.52%, South Korea +0.34%, India -0.65%. China's Shanghai Composite fell back from a 2-month high and closed lower on liquidity concerns after the 7-day repurchase rate, a gauge of interbank funding liquidity, jumped 29 bp to a 19-month high of 2.81%. Banks are hoarding cash amid concerns liquidity will tighten with more than $150 billion of loans coming due.

The dollar index (DXY00 +0.16%) is up +0.16% at a 3-1/2 week high. EUR/USD (^EURUSD) is down -0.21% at a 1-month low. USD/JPY (^USDJPY) is up +0.21% at a 2-1/2 week high. The dollar is higher on positive carry-over from Tuesday's testimony from Fed Chair Yellen who said it "would be unwise" to wait too long to raise interest rates.

Mar 10-year T-note prices (ZNH17 -0.04%) are down -2.5 ticks.

U.S. STOCK PREVIEW

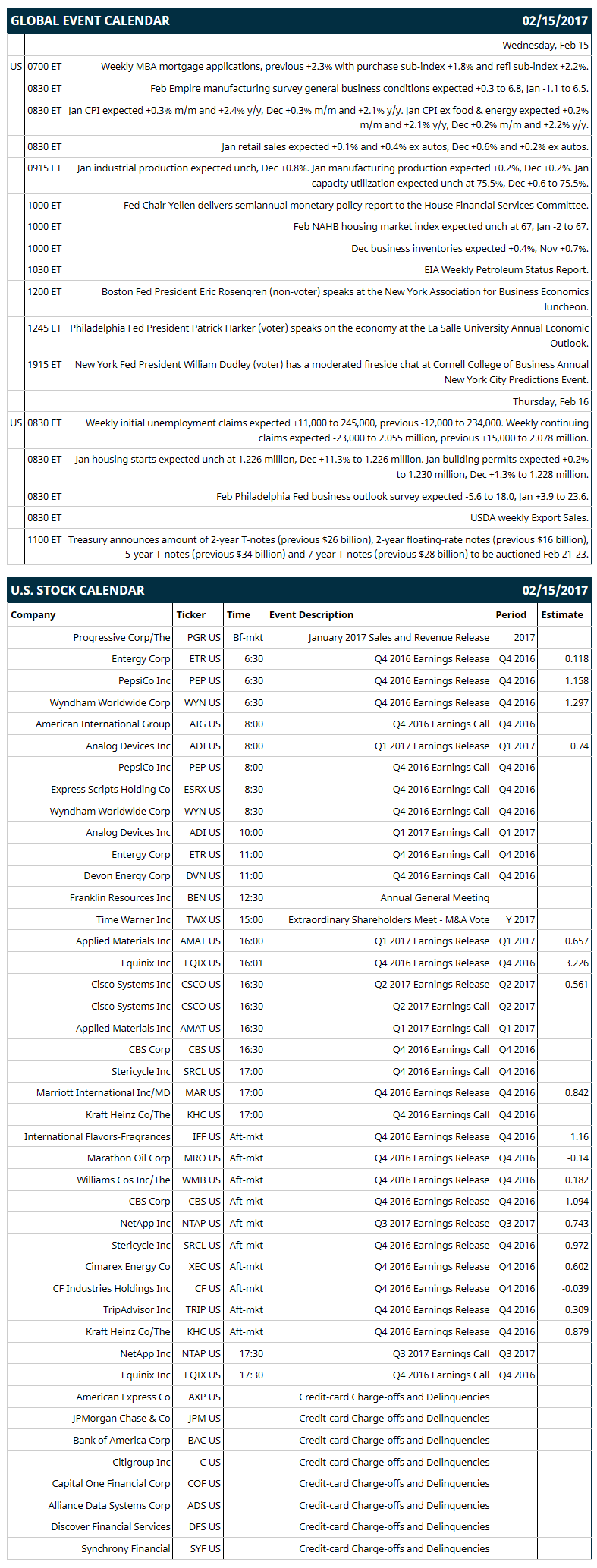

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +2.3% with purchase sub-index +1.8% and refi sub-index +2.2%), (2) Feb Empire manufacturing index (+0.3 to 6.8, Jan -1.1 to 6.5), (3) Jan CPI (expected +0.3% m/m and +2.4% y/y, Dec +0.3% m/m and +2.1% y/y) and Jan CPI ex food & energy (expected +0.2% m/m and +2.1% y/y, Dec +0.2% m/m and +2.2% y/y), (4) Jan retail sales (expected +0.1% and +0.4% ex autos, Dec +0.6% and +0.2% ex autos), (5) Jan industrial production (expected unchanged, Dec +0.8%) and Jan manufacturing production (expected +0.2%, Dec +0.2%), (6) Fed Chair Yellen delivers semiannual monetary policy report to the House Financial Services Committee, (7) Feb NAHB housing market index (expected unch at 67, Jan -2 to 67), (8) Dec business inventories (expected +0.4%, Nov +0.7%), (9) Boston Fed President Eric Rosengren (non-voter) speaks at the New York Association for Business Economics luncheon, (10) Philadelphia Fed President Patrick Harker (voter) speaks on the economy at the La Salle University Annual Economic Outlook, (11) New York Fed President William Dudley (voter) has a moderated fireside chat at Cornell College of Business Annual New York City Predictions Event, (12) EIA Weekly Petroleum Status Report.

Notable S&P 500 earnings reports today include: Pepsico (consensus $1.16), Applied Materials (0.66), Marathon Oil (-0.14), Williams Cos (0.18), Cisco (0.56), TripAdvisor (0.31), Kraft Heinz (0.87).

U.S. IPO's scheduled to price today: none.

Equity conferences: Credit Suisse Energy Summit on Mon-Wed, RSA Security Conference on Mon-Thu, Stifel Transportation and Logistics Conference on Tue-Wed, Goldman Sachs Technology and Internet Conference on Tue-Thu, Bank of America Merrill Lynch Insurance Conference on Wed-Thu, Leerink Partners Global Health Care Conference on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

Under Armour (UA +4.08%) was downgraded to 'Negative' from 'Positive' at Susquehanna Financial with its price target cut to $14 from $24.

Agilent Technologies (A -0.26%) rose 4% in after-hours trading after it reported Q1 adjusted EPS continuing operations of 53 cents, above consensus of 49 cents, and said it sees full-year revenue of $4.33 billion-$4.35 billion, higher than consensus of $4.33 billion

Procter & Gamble (PG -0.51%) climbed 3% in after-hours trading after Trian Fund Management LP said it added the company to its investments in Q4.

American International Group (AIG +1.13%) dropped over 4% in after-hours trading after it reported a Q4 operating loss of -$2.72 a share, much weaker than consensus of 42 cents EPS.

Devon Energy (DVN +1.50%) gained over 1% in after-hours trading after it reported Q4 core EPS of 25 cents, above consensus of 21 cents.

Express Scripts Holding Co. (ESRX +0.48%) fell over 1% in after-hours trading after it reported Q4 revenue of $24.9 billion, below consensus of $26.3 billion, and said it sees Q1 adjusted EPS of $1.30-$1.34, weaker than consensus of $1.36.

Southwest Airlines (LUV -0.75%) rose over 1% in after-hours trading after Berkshire Hathaway said it added the company to its investments in Q4.

American Airlines Group (AAL -1.77%) gained 2% in after-hours trading after Berkshire Hathaway boosted its stake in the company to 8.79% from 4.2%.

Diamondback Energy (FANG +3.24%) gained almost 1% in after-hours trading after it reported Q4 adjusted EPS of 90 cents, well above consensus of 53 cents.

Fossil Group (FOSL -0.48%) sank 12% in after-hours trading after it reported Q4 EPS of $1.03, below consensus of $1.17, and said it sees a Q1 adjusted loss of -10 cents to -25 cents a share, well below consensus of a 7-cent gain.

SolarEdge Technologies (SEDG +7.43%) jumped nearly 6% in after-hours trading after it said it sees Q3 revenue of $110 million-$120 million, better than consensus of $108.4 million.

Potbelly (PBPB -2.64%) rose almost 3% in after-hours trading after it reported Q4 adjusted EPS of 15 cents, over double consensus of 7 cents.

LendingClub (LC -1.20%) slid over 6% in after-hours trading after it said it sees Q1 net revenue of $117 million-$122 million, less than consensus of $133.2 million.

NetScout Systems (NTCT -0.27%) gained 1% in after-hours trading after ValueAct Holdings LP said it added the stock to its investments.

Seacoast Banking (SBCF -0.87%) dropped 4% in after-hours trading after it announced an underwritten public offering of its common stock, although no amount was given.

Trupanion (TRUP +0.18%) slumped 15% in after-hours trading after it reported Q4 adjusted Ebitda of $302,000, well below consensus of $458,800.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 -0.03%) this morning are down -1.50 points (-0.06%). The S&P 500 on Tuesday rallied to a new all-time high and closed higher: S&P 500 +0.40%, Dow Jones +0.45%, Nasdaq +0.27%. Bullish factors included (1) upbeat comments from Fed Chair Yellen who said the economy has continued to make progress toward the Fed's goals, and (2) strength in energy producers as the price of crude oil rose %. Bearish factors included (1) the statement from Fed Chair Yellen who said "waiting too long to remove accommodation would be unwise," and (2) increased price pressures on the wholesale level after U.S. Jan PPI ex food and energy rose +0.4% m/m and +1.2% y/y, stronger than expectations of +0.2% m/m and +1.1% y/y.

Mar 10-year T-notes (ZNH17 -0.04%) this morning are down -2.5 ticks. Mar 10-year T-notes in Tuesday tumbled to a 1-1/2 week low and closed lower: TYH7 -11.50, FVH7 -8.00. Bearish factors included (1) hawkish commentary from Fed Chair Yellen who said waiting too long to raise interest rates "would be unwise," and (2) the larger-than-expected increase in U.S. Jan PPI ex food & energy, which bolsters the case for the Fed to increase interest rates sooner rather than later.

The dollar index (DXY00 +0.16%) this morning is up +0.16 (+0.16%) at a 3-1/2 week high. EUR/USD (^EURUSD) is down -0.0022 (-0.21%) at a 1-month low. USD/JPY (^USDJPY) is up +0.24 (+0.21%) at a 2-week high. The dollar index on Tuesday rallied to a 3-week high and closed higher: Dollar index +0.18 (+0.18%), EUR/USD -0.0020 (-0.19%), USD/JPY +0.52 (+0.46%). Bullish factors included (1) comments from Fed Chair Yellen who said it would be "unwise" to wait too long to remove accommodation, which increased the chances of a Fed rate hike at the Mar FOMC meeting, and (2) weakness in EUR/USD, which fell to a 1-month low after Eurozone Q4 GDP expanded at a +1.7% y/y pace, slower than expectations of +1.8% y/y, and after Eurozone Dec industrial production fell -1.6% m/m, the biggest decline in 10 months.

Mar WTI crude oil prices (CLH17 -0.60%) this morning are down -36 cents (-0.68%) and Mar gasoline (RBH17 -0.14%) is -0.0027 (-0.17%). Mar crude oil and gasoline on Tuesday closed higher: Mar crude +0.27 (+0.51%), Mar gasoline +0.0021 (+0.14%). The main bullish factor is optimism that OPEC is adhering to its supply cuts after Saudi Arabia said it reduced its Jan crude production by -717,600 bpd, the most in 8 years. Bearish factors included (1) the rally in the dollar index rose to a 3-week high, and (2) expectations for Wednesday's weekly EIA crude inventories to increase by +3.5 million bbl.

(Click on image to enlarge)

Disclosure: None.