Morning Call For Wednesday, Dec. 14

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 +0.01%) are little changed, down -0.01%, and European stocks are down -0.50% ahead of the results of today's FOMC meeting where the Fed is expected to raise its fed funds target range by 25 bp. Another negative for stocks is weakness in energy producing companies with Jan WTI crude oil (CLF17 -1.49%) down -1.30%. Crude prices retreated after the API reported late yesterday afternoon that U.S. crude supplies rose by +4.68 million bbl last week. Also undercutting European stocks was the unexpected decline in Eurozone Oct industrial production for a second month. Asian stocks settled mixed: Japan +0.02%, Hong Kong +0.04%, China -0.46%, Taiwan -0.15%, Australia +0.71%, Singapore -0.04%, South Korea +0.14%, India -0.36%. Japan's Nikkei Stock Index rose to a new 11-3/4 month high as exporter stocks rallied with USD/JPY holding just below Monday's 10-month high. Losses in Chinese stocks were limited after China Nov aggregate financing, the broadest measure of credit, expanded by the most in 8 months.

The dollar index (DXY00 -0.20%) is down -0.20%. EUR/USD (^EURUSD) is up +0.19%. USD/JPY (^USDJPY) is down 0.22%.

Mar 10-year T-note prices (ZNH17 +0.24%) are up +9.5 ticks.

Eurozone Oct industrial production of -0.1% m/m and +0.6% y/y was weaker than expectations of +0.1% m/m and +0.8% y/y.

China Nov new yuan loans rose +794.6 billion yuan, stronger than expectations of +720.0 billion yuan. Nov aggregate financing rose +1.74 trillion yuan, stronger than expectations of +1.1 trillion yuan and the most in 8 months.

U.S. STOCK PREVIEW

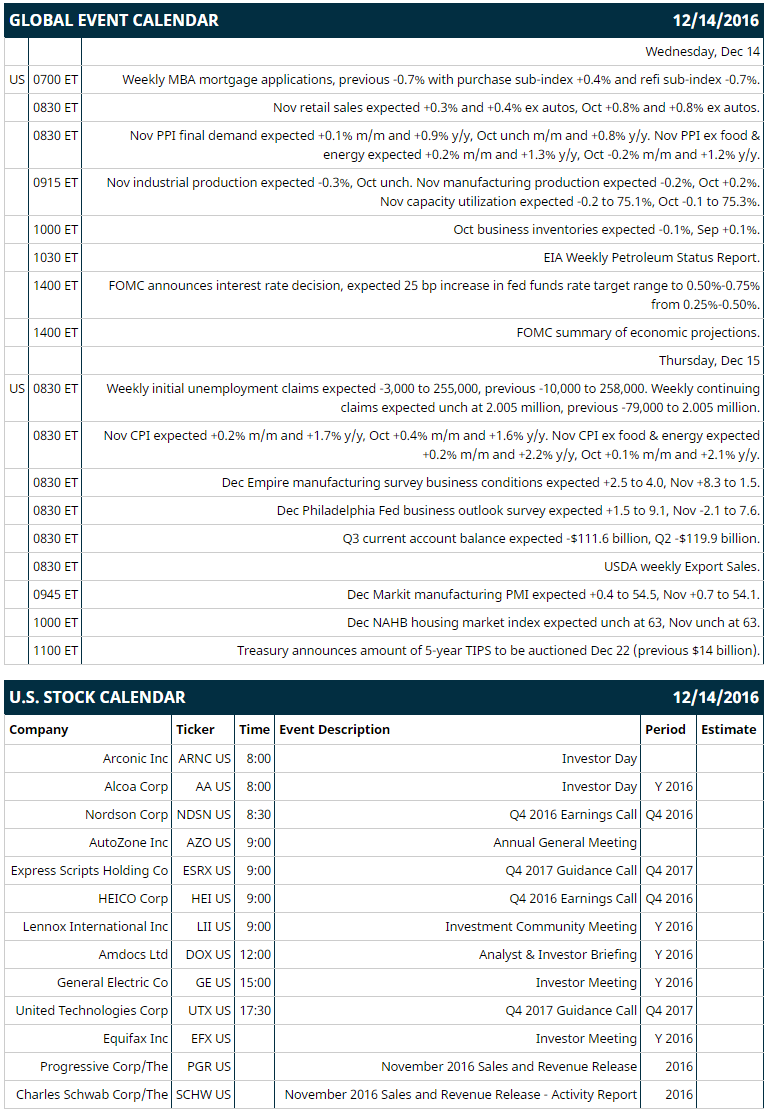

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -0.7% with purchase sub-index +0.4% and refi sub-index -0.7%), (2) Nov retail sales (expected +0.3% and +0.4% ex autos, Oct +0.8% and +0.8% ex autos), (3) Nov PPI final demand (expected +0.1% m/m and +0.9% y/y, Oct unch m/m and +0.8% y/y) and Nov PPI ex food & energy (expected +0.2% m/m and +1.3% y/y, Oct -0.2% m/m and +1.2% y/y), (4) Nov industrial production (expected -0.3%, Oct unch), (5) Oct business inventories (expected -0.1%, Sep +0.1%), (6) FOMC meeting concludes with expected 25 bp increase in fed funds rate target range to 0.50%-0.75% from 0.25%-0.50%, and (7) EIA Weekly Petroleum Status Report.

Russell 1000 earnings reports today include: none.

U.S. IPO's scheduled to price today: TiGenix NV (TIG).

Equity conferences this week include: Bank of America Merrill Lynch SMID Cap Technology Conference on Wed, BMO Capital Markets Prescriptions for Success Healthcare Conference on Wed, RBC Capital Markets' Healthcare Investor Day on Thu.

OVERNIGHT U.S. STOCK MOVERS

Qualcomm (QCOM +1.27%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase with a price target of $70.

Pridential Financial (PRU +0.30%) was downgraded to 'Equal-Weight' from 'Overweight' at Morgan Stanley.

Nordson (NDSN -0.38%) rallied 7% in after-hours trading after it reported Q4 adjusted EPS of $1.39, better than consensus of $1.24, and said it sees Q1 EPS of 74 cents-84 cents, above consensus of 70 cents.

Hertz Global Holdings (HTZ +10.56%) declined 4% in after-hours trading after CEO John Tague said he will retire January 2 and Kathryn Marinello will become the new CEO.

PBF Energy (PBF -0.56%) dropped 2% in after-hours trading after it announced a public offering of 10 million shares of common stock.

Wells Fargo (WFC +0.11%) lost 1% in after-hours trading after U.S. regulators said the bank could not unwind its business in the event of a failure and rejected its living will for a second time.

Callon Petroleum (CPE +4.00%) fell almost 3% in after-hours trading after it announced a public offering of 34 million shares of common stock.

RCI Hospitality Holdings (RICK +3.09%) climbed nearly 4% in after-hours trading after it reported Q4 adjusted EPS of 31 cents, better than consensus of 21 cents.

HEICO (HEI -0.68%) slid 1% in after-hours trading after it reported Q4 net sales of $363.3 million, below consensus of $372.5 million.

Wabash National (WNC -1.14%) gained almost 2% in after-hours trading after it reinstated its quarterly dividend of 6 cents per share, its first dividend in 8 years.

Peak Resorts (SKIS -0.98%) jumped 15% in after-hours trading after the U.S. CIS gave approval needed for funds raised in Mount Snow's EB-5 offering to be released from escrow immediately.

Global Eagle Entertainment (ENT +1.74%) surged nearly 20% in after-hours trading after Southwest Airlines extended the use of Global Eagle's Airconnect connectivity system and services.

Eagle Bulk Shipping (EGLE -1.92%) slumped 9% in after-hours trading after it announced a $100 million private placement of approximately 22 million shares of common stock.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 +0.01%) this morning are down -0.25 of a point (-0.01%). Tuesday's closes: S&P 500 +0.65%, Dow Jones +0.58%, Nasdaq +1.26%. The S&P 500 on Tuesday rallied to a new record high and closed higher on carry-over support from strength in European stocks on reduced banking concerns in Italy after UniCredit SpA, Italy's biggest bank, rallied sharply after it laid out plans to cut bad loans and boost profits. Stocks were also boosted by signs of economic strength in China after China Nov retail sales rose at the fastest pace in 11 months and after Chinese Nov industrial production rose more than expected. U.S. technology stocks showed strength as the Nasdaq Composite rose to a record high.

Mar 10-year T-notes (ZNH17 +0.24%) this morning are up +9.5 ticks. Tuesday's closes: TYH7 -2.50, FVH7 -4.25. Mar 10-year T-notes on Tuesday closed lower on the rally in the S&P 500 to a new record high and on supply pressures as the Treasury auctioned $12 billion in 30-year T-bonds.

The dollar index (DXY00 -0.20%) this morning is down -0.200 (-0.20%). EUR/USD (^EURUSD) is up +0.0020 (+0.19%). USD/JPY (^USDJPY) is down -0.25 (-0.22%). Tuesday's closes: Dollar index +0.040 (+0.04%), EUR/USD -0.0009 (-0.08%), USD/JPY +0.17 (+0.15%). The dollar index on Tuesday closed slightly higher on the rally in the S&P 500 to a new all-time high, which pushed USD/JPY higher on reduced safe-haven demand for the yen. The dollar was also boosted by short-covering ahead of the results of Wednesday's FOMC meeting where the Fed is expected to raise the fed funds target range by 25 bp.

Jan WTI crude oil prices (CLF17 -1.49%) this morning are down -69 cents (-1.30%) and Jan gasoline (RBF17 -1.77%) is -0.0275 (-1.77%). Tuesday's closes: Jan crude -0.37 (-0.70%), Jan gasoline -0.0101 (-0.65%). Jan crude oil and gasoline on Tuesday closed lower on a stronger dollar and on concern that the recent rise in oil prices to a 17-month high will spur increased U.S. shale-oil production. Oil prices were boosted by the prediction from the IEA that the global energy market will move from surplus into deficit in the first half of 2017, sooner than an earlier prediction of a deficit at the end of 2017.

Disclosure: None.