Morning Call For Wednesday, April 19

OVERNIGHT MARKETS AND NEWS

Jun E-mini S&Ps (ESM17 +0.27%) this morning are up +0.27% and European stocks are up +0.37%. A 4% rally in Morgan Stanley in pre-market trading is giving banking stocks a boost after it reported Q1 revenue of $9.75 billion, higher than expectations of $9.29 billion. Energy producing stocks are higher as well with May WTI crude oil (CLK17 +0.13%) up +0.29% after the API reported Tuesday afternoon that U.S. crude stockpiles fell -840,000 bbl last week. Strength in automakers is giving European stocks a lift after Eurozone Mar new car registrations rose +11.2% y/y. The U.S. markets await the Fed's Beige Book, to be released this afternoon, as to clues for the future direction of monetary policy. Asian stocks settled mostly lower: Japan +0.07%, Hong Kong -0.41%, China -0.81%, Taiwan -1.09%, Australia -0.56%, Singapore -0.36%, South Korea -0.63%, India +0.06%. China's Shanghai Composite fell to a 2-1/4 month low on concern that China's securities regulators will impose stricter regulations on the market after the president of the China Securities Regulatory Commission called on China's bourses to "show swords" and crack down on behavior that disrupts the market order "without mercy."

The dollar index (DXY00 +0.13%) is up +0.12%. EUR/USD (^EURUSD) is down -0.02%. USD/JPY (^USDJPY) is up +0.43%.

Jun 10-year T-note prices (ZNM17 -0.23%) are down -7 ticks.

ECB Governing Council member Hansson said growth rates in the Eurozone are "probably higher than potential" and the "output gap is closing" but at the same time, it's too early for the ECB to rush with concrete actions and claim victory over weak inflation, which remains volatile.

Eurozone Mar new car registrations rose +11.2% y/y to 1,891,583 million and are up +8.4% year-to-date at 4,141,269.

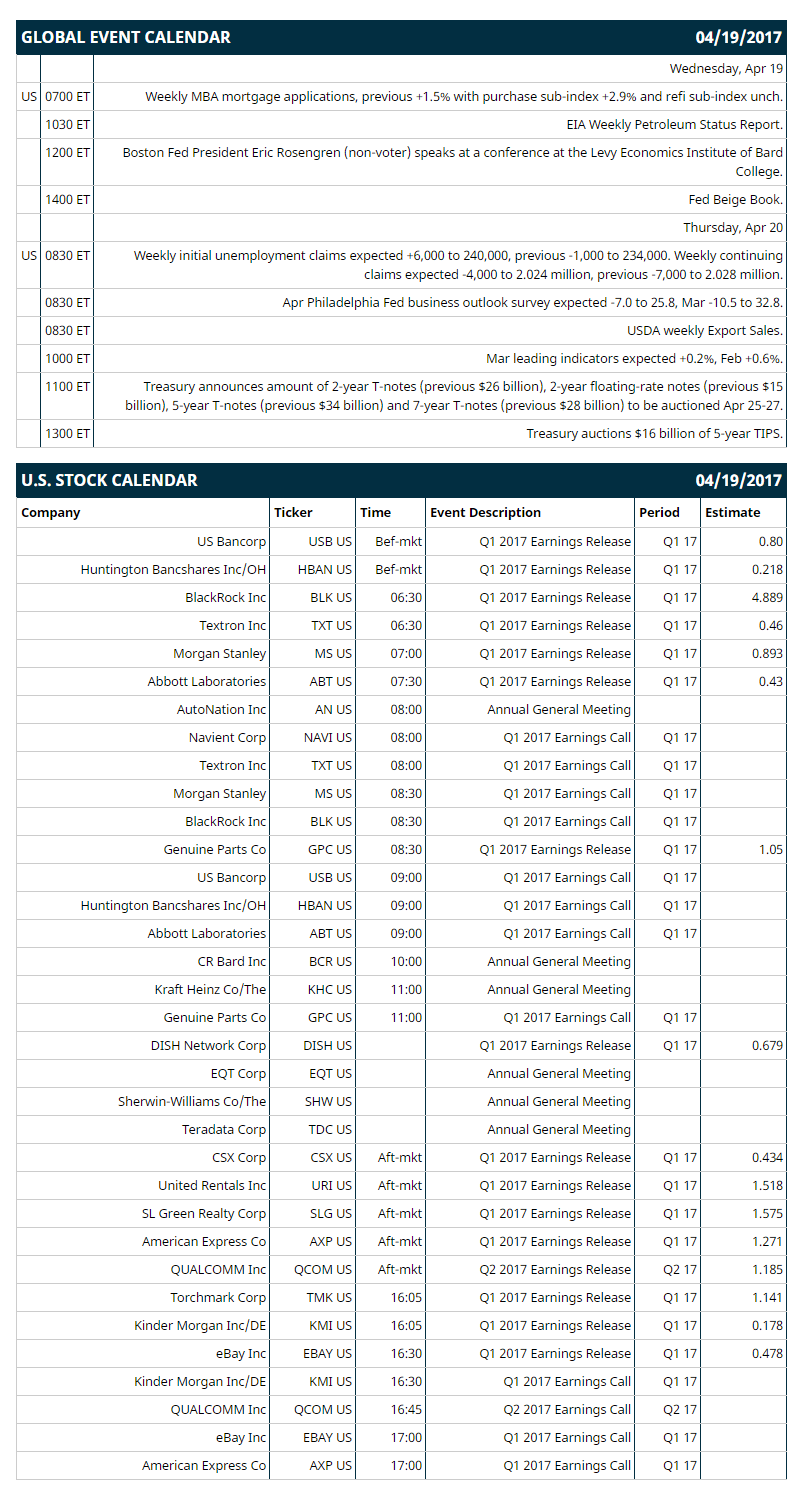

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +1.5% with purchase sub-index +2.9% and refi sub-index unch), (2) Boston Fed President Eric Rosengren (non-voter) speaks at a conference at the Levy Economics Institute of Bard College, (3) Fed Beige Book, (4) EIA Weekly Petroleum Status Report.

Notable Russell 1000 earnings reports today include: Morgan Stanley (consensus $0.89), US Bancorp (0.80), Blackrock (4.89), Abbott Labs (0.43), AMEX (1.27), Kinder Morgan (0.18), eBay (0.48).

U.S. IPO's scheduled to price today: none.

Equity conferences: none.

OVERNIGHT U.S. STOCK MOVERS

Morgan Stanley (MS -0.67%) jumped 4% in pre-market trading after it reported Q1 revenue of $9.75 billion, higher than consensus of $9.29 billion.

Fastenal (FAST -3.36%) was upgraded to 'Outperform' from 'Neutral' at Credit Suisse with a target price of $52.

Lam Research (LRCX +0.08%) gained almost 4% in after-hours trading after it reported Q3 adjusted EPS of $2.80, higher than consensus of $2.57.

Intuitive Surgical (ISRG -1.16%) rallied over 3% in after-hours trading after it reported Q1 adjusted EPS of $5.09, better than consensus of $4.95.

Bank of America (BAC -0.44%) was upgraded to 'Strong Buy' from 'Market Outperform' at Vining Sparks with a price target of $28.

Eli Lilly (LLY -1.43%) was downgraded to 'Underperform' from 'Market Perform' at BMO Capital Markets.

International Business Machines (IBM -0.61%) dropped 4% in after-hours trading after it reported Q1 revenue of $18.2 billion, below consensus of $18.4 billion and the 20th straight quarterly revenue decline.

Allstate (ALL -1.46%) was downgraded to 'Neutral' from 'Outperform' at Macquarie Research.

ICU Medical (ICUI -0.68%) fell over 2% in after-hours trading after it received a grand jury subpoena in connection with the Hospira Infusion Systems business it acquired from Pfizer in February.

LegacyTexas Financial Group (LTXB -0.13%) sold-off nearly 7% in after-hours trading after it reported Q1 core EPS of 37 cents, well below consensus of 58 cents.

Ultragenyx Pharmaceutical (RARE -2.23%) surged nearly 20% in after-hours trading after its Burosumab drug met the primary endpoint and demonstrated a statistically significant improvement is serum phosphorous levels in a Phase 3 study in adults with X-linked hypophosphatemia.

Interactive Brokers Group (IBKR +0.84%) lost nearly 3% in after-hours trading after it reported Q1 net revenue of $374 million, below consensus of $393.4 million.

CalAmp (CAMP -0.93%) climbed nearly 3% in after-hours trading after it reported Q4 adjusted EPS of 28 cents, above consensus of 27 cents.

Diana Shipping (DSX -8.59%) dropped 7% in after-hours trading after it announced that it had commenced an underwritten public offering of $70 million of common shares.

Nivalis Therapeutics (NVLS -4.69%) surged over 25% in after-hours trading after it announced a merger agreement with Alpine Immune Sciences with Alpine becoming a wholly-owned subsidiary of Nivalis.

MARKET COMMENTS

Jun E-mini S&Ps (ESM17 +0.27%) this morning are up +6.25 points (+0.27%). Tuesday's closes: S&P 500 -0.29%, Dow Jones -0.55%, Nasdaq -0.14%. The S&P 500 on Tuesday closed lower on the unexpected -0.4% drop in U.S. Mar manufacturing production, weaker than expectations of unchanged and the biggest decline in 7 months. Other weak economic data included the -6.8% drop in U.S. Mar housing starts to 1.215 million, weaker than expectations of -3.0% to 1.25 million. There was weakness in bank stocks led by a -4.7% fall in Goldman Sachs after it reported Q1 net revenue of $8.03 billion, weaker than consensus of $8.33 billion, as bond trading revenue declined.

Jun 10-year T-notes (ZNM17 -0.23%) this morning are down -7 ticks. Tuesday's closes: TYM7 +19.50, FVM7 +10.75. Jun T-notes on Tuesday rallied to a new 5-1/4 month high and closed higher on reduced inflation expectations after the 10-year T-note breakeven inflation rate fell to a 5-month low. T-notes were also boosted by increased safe-haven demand with the sell-off in stocks.

The dollar index (DXY00 +0.13%) this morning is up +0.123 (+0.12%). EUR/USD (^EURUSD) is -0.0002 (-0.02%) and USD/JPY (^USDJPY) is up +0.47 (+0.43%). Tuesday's closes: Dollar index -0.791 (-0.79%), EUR/USD +0.0087 (+0.82%), USD/JPY -0.48 (-0.44%). The dollar index on Tuesday dropped to a 2-1/2 week low and closed lower on the weaker-than-expected U.S. Mar housing starts report and U.S. Mar manufacturing production report. The dollar was also undercut by a surge in GBP/USD to a 6-1/4 month high after U.K. Prime Minister May called for early elections in June, which bolstered speculation that Prime Minister May's Conservative party will strengthen her hand on negotiating Brexit.

May WTI crude oil prices (CLK17 +0.13%) this morning are up +15 cents (+0.29%) and May gasoline (RBK17 -0.42%) is -0.0065 (-0.38%). Tuesday's closes: May crude -0.24 (-0.46%), May gasoline -0.0086 (-0.50%). May crude oil and gasoline on Tuesday fell to 1-week lows and closed lower. Oil prices were undercut by concern about increasing U.S. crude production after last Friday's data from Baker Hughes showed U.S. active oil rigs in the week ended Apr 14 rose +11 to 683, the most in 1-3/4 years. In addition, the crack spread fell to a 3-week low, which may curb refinery demand for crude to refine into gasoline. Oil prices were supported by the slide in the dollar index to a 2-1/2 week low, reduced global supplies after Saudi Arabia Feb oil exports fell to a 21-month low of 6.95 million bpd, and expectations for Wednesday's weekly EIA crude inventories to fall -1.4 million bbl.

Disclosure: None.