Morning Call For Wednesday, April 12

OVERNIGHT MARKETS AND NEWS

Jun E-mini S&Ps (ESM17 -0.16%) this morning are down -0.07% as geopolitical developments pressure stocks. North Korea warned of a nuclear strike if provoked and President Trump tweeted Tuesday that the U.S. was prepared to "solve the problem" of North Korea with or without China's help. U.S. Secretary of State Tillerson is meeting Russian Foreign Minister Lavrov in Moscow after the Trump administration accused Russia of trying to cover up a chemical-weapons attack by Syria. Heightened geopolitical concerns have led to safe-haven buying of gold with Jun COMEX gold (GCM17 +0.16%) up +0.15% at a 5-month high. European stocks are up +0.08% at a 1-week high, led by strength in auto makers, after Daimler AG reported Q1 earnings before interest and taxes climbed to 4 billion euros from 2.15 billion euros a year earlier. Another positive for stocks is the +0.60% rally in May WTI crude oil (CLK17 +0.32%) to a 5-week high that boosted energy producing stocks after API data late Tuesday showed U.S. crude inventories fell -1.3 million bbl last week. Asian stocks settled mixed: Japan -1.04%, Hong Kong +0.93%, China -0.46%, Taiwan -0.15%, Australia +0.08%, Singapore +0.35%, South Korea +0.26%, India -0.49%. A sell-off in exporter stocks pushed Japan's Nikkei Stock Index down to a 4-month low as USD/JPY fell to a 4-3/4 month low, which reduces the earnings prospects of exporters.

The dollar index (DXY00 +0.01%) is up +0.01%. EUR/USD (^EURUSD) is down -0.02%. USD/JPY (^USDJPY) is unchanged.

Jun 10-year T-note prices (ZNM17 +0.01%) are unchanged.

China Mar CPI rose +0.9% y/y, weaker than expectations of +1.0% y/y. Mar PPI rose +7.6% y/y, stronger than expectations of +7.5% y/y.

U.S. STOCK PREVIEW

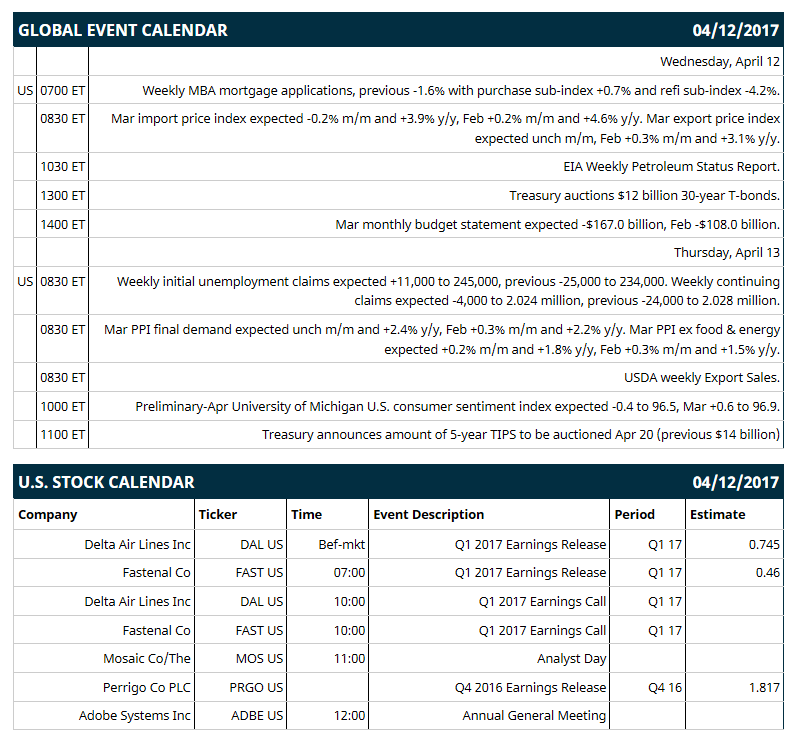

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -1.6% with purchase sub-index +0.7% and refi sub-index -4.2%), (2) Mar import price index (expected -0.2% m/m and +3.9% y/y, Feb +0.2% m/m and +4.6% y/y), (3) Treasury auctions $12 billion 30-year T-bonds, (4) Mar monthly budget statement (expected -$167.0 billion, Feb -$108.0 billion), (5) EIA Weekly Petroleum Status Report.

Notable Russell 1000 earnings reports today include: Delta Airlines (consensus $0.75), Fastenal (0.46), Perrigo (1.82).

U.S. IPO's scheduled to price today: Warrior Met Coal (HCC), Cadence BanCorp (CADE), Yext (YEXT), Tocagen (TOCA).

Equity conferences: Bank of America Merrill Lynch Auto Summit on Wed, Next Generation Pharmaceutical Samples Conference on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

PayPay Holdings (PYPL -0.84%) was downgraded to 'Sell' from 'Buy' at National Bank AG.

Delta Air Lines (DAL +0.71%) climbed nearly 3% in pre-market trading after it reported Q1 adjusted EPS of 77 cents, higher than consensus of 75 cents

Whole Foods Markets (WFM -1.81%) rose 4% in pre-market trading after a person with knowledge of the situation said that Amazon.com pursued a possible purchase of Whole Foods last fall.

Adobe Systems (ADBE -0.16%) was initiated at Stifel with a recommendation of 'Buy' with a price target of $150.

Tractor Supply (TSCO +0.09%) fell 3% in after-hours trading after it said it sees preliminary Q1 EPS of 35 cents-46 cents, below consensus of 53 cents.

NuStar Energy (NS +0.10%) dropped nearly 7% in after-hours trading after it said it will offer 10.5 million common units to fund its $1.475 billion purchase of Navigator Energy Services LLC.

Healthcare Services Group (HCSG +1.93%) rose almost 5% in after-hours trading after it reported Q1 EPS of 30 cents, higher than consensus of 29 cents.

Talend (TLND +0.35%) was initiated at Pacific Crest Securities with a recommendation of 'Overweight' with a 12-month target price of $38.

Great Western Banc (GWB +2.04%) was initiated at D.A. Davidson with recommendation of 'Buy' with a 12-month target price of $50.

AllianceBernstein (AB -1.54%) was upgraded to 'Outperform' from 'Market Perform' at Keefe, Bruyette & Woods with a price target of $26.

Tonix Pharmaceuticals (TNXP +7.21%) added another 4% gain in after-hours trading on top of Tuesday's 7% gain after the FDA said that a single study NDA approval of its TNX-102 SL for treatment of post-traumatic stress disorder could be possible, bases on statistically persuasive data from its ongoing study.

Organovo Holdings (ONVO +0.66%) slid 6% in after-hours trading after CEO Keith Murphy stepped down and Taylor Crouch was named new CEO effective April 21.

MARKET COMMENTS

Jun E-mini S&Ps (ESM17 -0.16%) this morning are down -1.75 points (-0.07%). Tuesday's closes: S&P 500 -0.14%, Dow Jones -0.03%, Nasdaq -0.43%. The S&P 500 on Tuesday dropped to a 2-week low and closed lower on geopolitical concerns that sent the VIX volatility index to 5-month high after the White House press secretary warned Syria to stop using barrel bombs against civilians, which fueled concern the Trump administration may ramp up military actions against Syria. In addition, President Trump said North Korea "is looking for trouble" and that the U.S. would "solve the problem" with or without China, which heightened concern the U.S. may take military action against North Korea. A bullish factor was the +118,000 increase in U.S. Feb JOLTS job openings to 5.743 million, stronger than expectations of +24,000 to 5.650 million and the most in 7 months.

Jun 10-year T-notes (ZNM17 +0.01%) this morning are unch. Tuesday's closes: TYM7 +18.50, FVM7 +11.50. Jun 10-year T-notes on Tuesday closed higher on reduced inflation expectations after the 10-year T-note breakeven inflation rate plunged to a 3-1/2 month low and on increased safe-haven demand for T-notes after the S&P 500 declined to a 2-week low.

The dollar index (DXY00 +0.01%) this morning is up +0.01 (+0.01%). EUR/USD (^EURUSD) is down -0.0002 (-0.02%) and USD/JPY (^USDJPY) is unch. Tuesday's closes: Dollar index -0.31 (-0.31%), EUR/USD +0.0009 (+0.08%), USD/JPY -1.32 (-1.19%). The dollar index on Tuesday closed lower on the decline in T-note yields, which reduces the dollar's interest rate differentials. In addition, USD/JPY fell to a 4-3/4 month low as weakness in stocks boosted the safe-haven demand for the yen.

May WTI crude oil prices (CLK17 +0.32%) this morning are up +32 cents (+0.60%) at a 5-week high and May gasoline (RBK17 +0.24%) is up +0.0089 (+0.51%) at a 1-1/2 year nearest-futures high. Tuesday's closes: May crude +0.32 (+0.60%), May gasoline -0.0004 (-0.02%). May crude oil and gasoline on Tuesday settled mixed with May crude at a 1-month high on a report that Saudi Arabia will agree to a 6-month extension of OPEC crude output cuts when the cartel meets next month. Crude oil prices were also boosted by expectations that Wednesday's EIA data will show U.S. crude inventories fell -1.75 million bbl. Gasoline closed lower after the crack spread fell to a 1-week low, which may curtail refinery demand for crude to refine into gasoline.

(Click on image to enlarge)

Disclosure: None.