Morning Call For Tuesday, March 7

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 -0.18%) this morning are down -0.15% and European stocks are down -0.14% as weakness in metals prices undercuts mining stocks and raw-material producers. Apr gold (GCJ17 -0.09%) is down -0.15% at a 2-1/2 week low as expectations mount for a Fed rate hike at next week's FOMC meeting, and May copper (HGK17 -0.57%) is down -0.60% at a 1-month low on signs of increased supplies amid weak demand after LME copper inventories jumped +26,725 MT to 261,975 MT, a 5-week high, and German factory orders plunged by the most in 8 years. Losses in stocks were contained after the OECD projected global growth will climb to 3.3% this year, up from 3.0% in 2016. Asian stocks settled mostly higher: Japan -0.18%, Hong Kong +0.36%, China +0.26%, Taiwan +0.57%, Australia +0.26%, Singapore +0.29%, South Korea +0.54%, India -0.17%. Chinese stocks rose on signs the government is taking steps to support the stock market as people familiar with the matter said China has banned net share sales by some large mutual funds to avoid net selling during the 2-week long meeting of the National People's Congress in Beijing. China's government has been known to intervene in markets during events of political importance.

The dollar index (DXY00 +0.13%) is up +0.13%. EUR/USD (^EURUSD) is down -0.08%. USD/JPY (^USDJPY) is up +0.03%.

Jun 10-year T-note prices (ZNM17 unch) are down -1 tick.

The Organization for Economic Cooperation and Development (OECD) projects global GDP to increase to 3.3% this year, up from +3.0% in 2016, but warned that "although risks may not materialize immediately, they remain a real possibility and a set of large shocks, possibly interacting with each other, would disrupt the recovery."

German Jan factory orders slumped -7.4% m/m, weaker than expectations of -2.5% m/m and the biggest decline in 8 years.

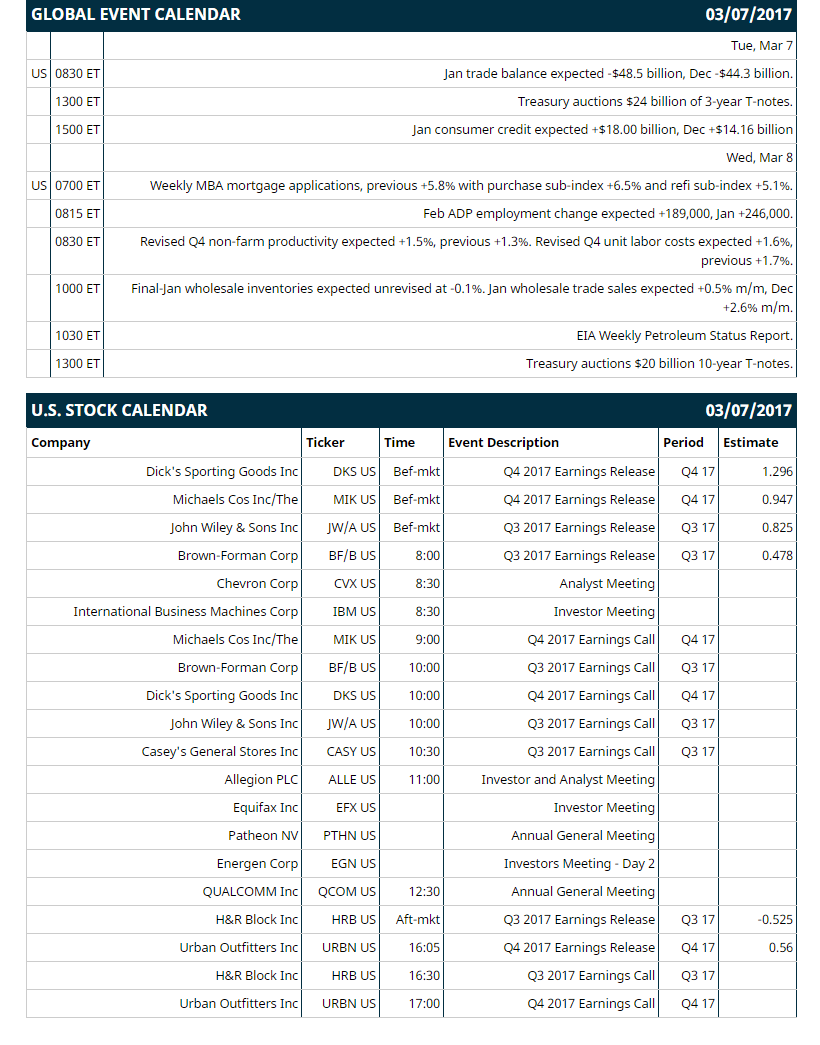

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Jan trade balance (expected -$48.5 billion, Dec -$44.3 billion), (2) Treasury auctions $24 billion of 3-year T-notes, (3) Jan consumer credit (expected +$17.75 billion, Dec +$14.16 billion).

Notable Russell 1000 earnings reports today include: Dicks Sporting Goods (1.30), Michaels Cos (0.95), John Wiley (0.83), Brown-Forman (0.48), H&R Block (-0.53), Urban Outfitters (0.56).

U.S. IPO's scheduled to price today: none.

Equity conferences: Citi Global Property CEO Conference on Mon-Tue, Cowen and Company Health Care Conference on Mon-Wed, Deutsche Bank Media, Internet & Telecom Conference on Mon-Wed, Raymond James and Associates Institutional Investors Conference on Mon-Wed, RBC Capital Markets Financial Institutions Conference on Tue-Wed, Raymond James and Associates Institutional Investors Conference on Wed, Susquehanna Financial Group LLLP Semi Storage & Technology Conference on Thu, UBS Global Consumer & Retail Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Casey's General Stores (CASY +0.25%) dropped 4% in after-hours trading after it reported Q3 EPS of 58 cents, well below consensus of 88 cents.

Hyatt Hotels (H -0.66%) was upgraded to "Equalweight' from 'Underweight' at Morgan Stanley with a price target of $53.

Weatherford International PLC (WFT +1.90%) jumped 14% in pre-market trading after it tapped Halliburton CFO Mark McCollum to be CEO at Weatherford.

DISH Network (DISH +0.08%) rallied nearly 5% in after-hours trading after it was announced that it will replace Linear Technology in the S&P 500 before the open on Monday, March 13.

salesforce.com (CRM +0.34%) gained 2% in after-hours trading after it announced an artificial intelligence software pact with IBM.

Extended Stay America (STAY -0.46%) fell over 2% in after-hours trading after it announced a secondary offering of 25 million paired shares.

Hannon Armstrong Sustainable Infrastructure Capital (HASI +0.55%) slipped nearly 4% in after-hours trading after it announced a public offering of 3.0 million shares of common stock.

First Republic Bank/CA (FRC +0.10%) lost nearly 2% in after-hours trading after it announced a 2.0 million share common stock offering.

La Jolla Pharmaceutical Co. (LJPC -4.05%) climbed nearly 4% in after-hours trading on signs of insider buying by Tang Capital Management.

Pacira Pharmaceuticals (PCRX -3.96%) fell 5% in after-hours trading after it announced a $300 million offering of convertible senior notes due in 2022.

MeetMe (MEET +5.41%) surged 20% in after-hours trading after it reported Q4 adjusted EPS of 19 cents, better than consensus of 17 cents, and then acquired If(we) for $60 million in cash.

Pier 1 Imports (PIR -3.62%) jumped 5% in after-hours trading after it reported preliminary Q4 adjusted EPS of 32 cents-34 cents, above consensus of 31 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 -0.18%) this morning are down -3.50 points (-0.15%). Monday's closes: S&P 500 -0.33%, Dow Jones -0.24%, Nasdaq -0.25%. The S&P 500 on Monday closed lower on geopolitical concerns after North Korea fired four ballistic missiles into waters near Japan and on weakness in commodity producing stocks as copper prices tumbled to a 1-week low on Chinese demand concerns after Chinese Premier Li Keqiang warned that profound changes in the international political and economic landscape threaten global growth. Stocks found some support from the +1.2% increase in U.S. Jan factory orders, stronger than expectations of +1.0%.

Jun 10-year T-notes (ZNM17 unch) this morning are down -1 tick. Monday's closes: TYM7 +0.50, FVM7 +0.75. Jun 10-year T-notes on Monday closed little changed. T-note prices were undercut by the larger-than-expected increase in U.S. Jan factors orders (+1.2% versus expectations of +1.0%) and by supply pressures with the Treasury set to auction $56 billion of T-notes and T-bonds this week. Losses were limited as a slide in stocks boosted the safe-haven demand for T-notes.

The dollar index (DXY00 +0.13%) this morning is up +0.13 (+0.13%). EUR/USD (^EURUSD) is down -0.0008 (-0.08%). USD/JPY (^USDJPY) is up +0.03 (+0.03%). Monday's closes: Dollar index +0.10 (+0.10%), EUR/USD -0.0040 (-0.38%), USD/JPY -0.15 (-0.13%). The dollar index on Monday closed higher on the stronger than expected U.S. Jan factory orders report and on weakness in EUR/USD on expectations for the ECB at Thursday's policy meeting to indicate that they will not taper asset purchases and will continue with their QE program through the end of the year.

Apr WTI crude oil (CLJ17 +0.30%) prices this morning are up +20 cents (+0.38%) and Apr gasoline (RBJ17 +1.17%) is +0.0206 (+1.23%). Monday's closes: Apr crude -0.13 (-0.24%), Apr gasoline +0.0192 (+1.16%). Apr crude oil and gasoline on Monday settled mixed. Crude oil prices were boosted by a comment by Iraq's oil minister that OPEC will probably have to extend its output curbs for more than six months and by concerns about supply disruptions after rebels seized Libya's Es Sider terminal, the country's biggest oil port, which may reduce Libya's oil output of 700,000 bpd. Crude oil prices were undercut by a stronger dollar and by concern about increased U.S. crude output after Baker Hughes reported Friday that U.S. active oil rigs in the week ended Mar 3 rose 7 to 609, the most in 17 months.

Disclosure: None.