Morning Call For Tuesday, June 20

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU17 unch) this morning are up +0.01% and European stocks are up +0.18% at a 2-week high. European stocks moved higher Tuesday on the heels of Monday's rally in U.S. markets where the S&P 500 climbed to a new all-time high. Gains were limited as energy stocks moved lower with Aug WTI crude oil (CLQ17 -1.85%) down -1.78% at a 7-month low on concern that rising Libyan oil production will increase the global oil surplus. According to people with knowledge of the matter, Libyan oil output is now at 900,000 bpd, the most in 4-years, after a deal with Wintershall AG enabled at least two more Libyan oil fields to resume production. Asian stocks settled mixed: Japan +0.81%, Hong Kong-0.31%, China -0.14%, Taiwan +0.72%, Australia -0.83%, Singapore -0.52%, South Korea +0.23%, India -0.04%. Chinese stocks closed slightly lower ahead of tomorrow’s decision by MSCI on whether it will include Chinese stocks in its benchmark share indexes. Japan's Nikkei Stock Index climbed to a 1-3/4 year high and garnered support from Monday's rally in the S&P 500 to a new record high spurred on by comments from New York Fed President Dudley who said the U.S. economic expansion "has a long way to go." Japanese exporters also rallied on improved earnings prospects after USD/JPY rose to a 3-week high.

The dollar index (DXY00 +0.10%) is up +0.06% at a 3-week high. EUR/USD (^EURUSD) is up +0.03%. USD/JPY (^USDJPY) is up +0.03% at a 3-week high.

Sep 10-year T-note prices (ZNU17 unch) are up +1.5 ticks.

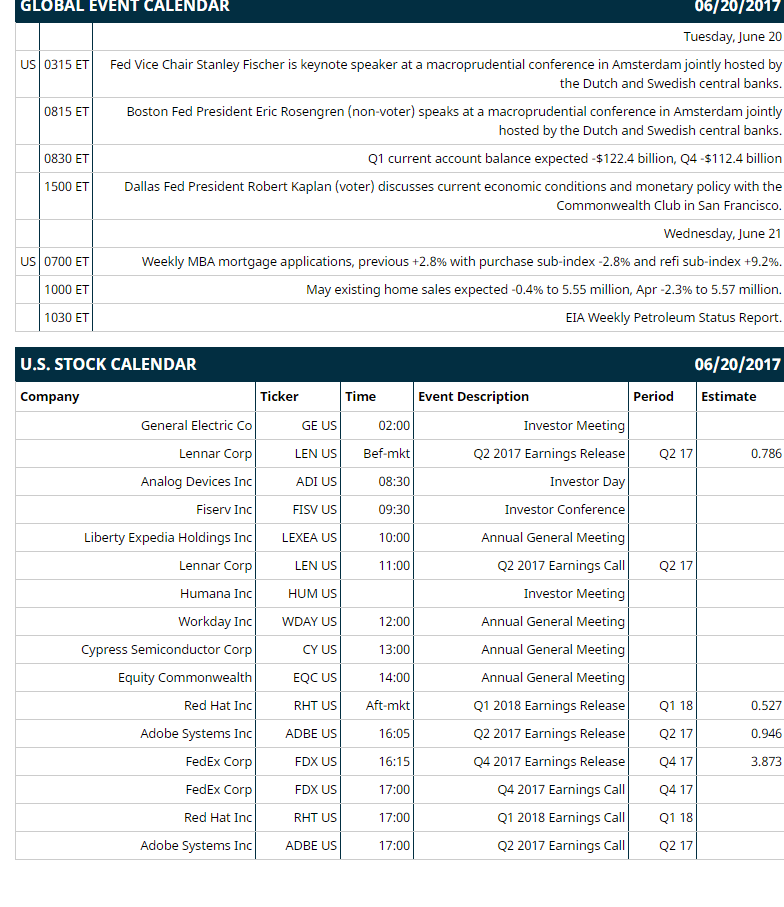

Fed Vice Chair Fischer said a long period of low interest rates may have contributed to "high and rising" home prices in several countries. He added that the social benefits of home-ownership "come at a cost" through tax treatment and government assumption of risk and that "the world as we know it cannot afford another pair of crisis of the magnitude of the Great Recession and the Global Financial Crisis."

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Fed Vice Chair Stanley Fischer is keynote speaker at a macroprudential conference in Amsterdam jointly hosted by the Dutch and Swedish central banks, (2) Boston Fed President Eric Rosengren (non-voter) speaks at a macroprudential conference in Amsterdam jointly hosted by the Dutch and Swedish central banks, (3) Q1 current account balance (expected -$122.4 billion, Q4 -$112.4 billion), (4) Dallas Fed President Robert Kaplan (voter) discusses current economic conditions and monetary policy with the Commonwealth Club in San Francisco.

Notable Russell 2000 earnings reports today include: FedEx (consensus $3.87), Adobe (0.95), Red Hat (0.53), Lennar (0.79).

U.S. IPO's scheduled to price today: none.

Equity conferences this week: Goldman Sachs Leveraged Finance Conference on Tue, JMP Group Securities Life Sciences Conference on Tue, Macquarie Group Ltd Global Quantitative Research Conference on Tue, Jefferies Global Consumer Conference on Tue-Wed, Oppenheimer Consumer Conference on Tue-Wed, Tudor Picker & Holt Hotter N Hell Energy Conference on Tue-Thu, Wells Fargo Securities West Coast Energy Conference on Tue-Wed, SunTrust Robinson Utilities & Power Summit on Thu, Wells Fargo Securities 5G Forum on Thu.

OVERNIGHT U.S. STOCK MOVERS

Tesla (TSLA -0.43%) gained over 2% in pre-market trading after it said it is close to an agreement to produce its electric cars in China.

Costco Wholesale (COST -1.66%) was upgraded to 'Buy' from 'Neutral' at Northcoast with a price target of $190.

Goodyear (GT +0.36%) was upgraded to 'Buy' from 'Hold' at Jeffries with a 12-month target price of $39.

O'Reilly Automotive (ORLY -0.44%) was downgraded to 'Neutral' from 'Positive' at Susquehanna.

Galapagos NV (GLPG +3.69%) was initiated with a 'Buy' rating at BTIG LLC with a 12-month target price of $98.

Owens Corning (OC +2.60%) was upgraded to 'Neutral' from 'Underperform' at Macquarie Research.

Clovis Oncology (CLVS +46.54%) lost 1% in after-hours trading after it proposed an underwritten public offering of $250 million of its common stock.

Reliance Steel & Aluminum (RS +0.10%) dropped over 6% in after-hours trading after it lowered guidance on Q2 EPS to $1.30-$1.40 from an April 27 estimate of $1.50-$1.60, citing "challenging" conditions.

Chipotle Mexican Grill (CMG +1.73%) fell 2% in after-hours trading after it said it expects expenses to r1se as much as 0.3% this quarter as it spends more on marketing and promotions to bounce back from a food-safety crisis.

Fidus Investment (FDUS +1.00%) lost 1% in after-hours trading after it announced the commencement of a registered underwritten public offering of 1.5 million shares of its common stock.

AveXis (AVXS +1.62%) slid 2% in after-hours trading after it said it intends to offer up to $200 million of its shares of its common stock in an underwritten public offering.

Lipocine (LPCN +3.88%) surged over 30% in after-hours trading after it said its LPCN 1021 testosterone drug met the FDA primary efficacy guidelines in a dosing valuation study where 81% of the subjects achieved average testosterone levels.

MARKET COMMENTS

Sep E-mini S&Ps (ESU17 unch) this morning are up +0.25 of a point (+0.01%). Monday's closes: S&P 500 +0.83%, Dow Jones +0.68%, Nasdaq +1.60%. The S&P 500 on Monday rallied to a fresh all-time high and closed higher on carry-over support from a rally in European stocks after Sunday's second-round of French elections showed French President Macron's pro-European party won about 350 seats in France's 577-member National Assembly, the largest majority in 15 years. Stocks were also boosted by a rally in technology stocks and by upbeat comments from New York Fed President Dudley who said the U.S. expansion "still has quite a long way to go."

Sep 10-year T-notes (ZNU17 unch) this morning are up +1.5 ticks. Monday's closes: TYU7 -9.50, FVU7 -6.75. Sep 10-year T-notes on Monday closed lower on comments from New York Fed President Dudley who said the U.S. economic expansion has "a long way to go," which bolsters the case for additional Fed tightening. There was also reduced safe-haven demand with the rally in the S&P 500 to a new record high.

The dollar index (DXY00 +0.10%) this morning is up +0.058 (+0.06%) at a 3-week high. EUR/USD (^EURUSD) is up +0.0003 (+0.03%) and USD/JPY (^USDJPY) is up +0.03% at a 3-week high. Monday's closes: Dollar index +0.37 (+0.3%), EUR/USD -0.0049 (-0.44%), USD/JPY +0.65 (+0.59%). The dollar index on Monday closed higher on comments from New York Fed President Dudley who said the U.S. economic expansion has "quite a long way to go." There was also weakness in the yen against the dollar as a rally in the S&P 500 to new all-time high reduced the safe-haven demand for the yen.

Aug WTI crude oil prices (CLQ17 -1.85%) this morning are down -79 cents (-1.78%) at a 7-month low and Aug gasoline (RBQ17 -1.43%) is -0.0192 (-1.33%). Monday's closes: Aug crude -0.54 (-1.20%), Aug gasoline -0.0055 (-0.38%). Aug crude oil and gasoline on Monday closed lower on a stronger dollar and Friday afternoon's data from Baker Hughes that showed U.S. active oil rigs in the week ended Jun 16 rose +6 to 747, the most in over 2 years.

Disclosure: None.