Morning Call For Tuesday, Dec. 6

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 +0.03%) are little changed, up +0.05%, as a -0.85% decline in Jan WTI crude oil (CLF17 -1.08%) weighs on energy producing stocks. Crude oil is under pressure on concern over whether OPEC will be able to adhere to its recently announced production cuts. European stocks are up +0.70% on signs of economic strength after German Oct factory orders rose more than expected by the most in 2-1/4 years. European stocks also garnered support and EUR/USD fell on expectations that ECB President Draghi will extend the central banks QE program beyond March of next year at this Thursday's policy meeting. Asian stocks settled mostly higher: Japan +0.47%, Hong Kong +0.75%, China -0.16%, Taiwan +0.98%, Australia +0.52%, Singapore +0.21%, South Korea +1.38%, India +0.17%.

The dollar index (DXY00 +0.19%) is up +0.19%. EUR/USD (^EURUSD) is down -0.24%. USD/JPY (^USDJPY) is up +0.11%.

Mar 10-year T-note prices (ZNH17 unch) are down -1 tick.

German Oct factory orders surged +4.9% m/m, stronger than expectations of +0.6% m/m and the largest monthly increase in 2-1/4 years.

U.S. STOCK PREVIEW

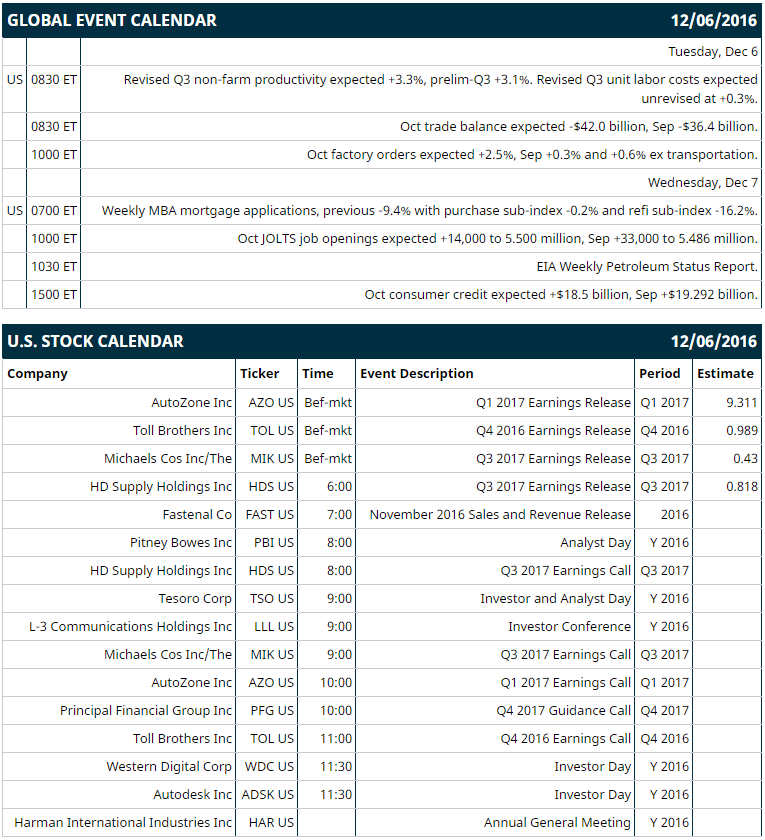

Key U.S. news today includes: (1) revised Q3 non-farm productivity (expected +3.3%, prelim-Q3 +3.1%) and revised Q3 unit labor costs (expected unrevised at +0.3%), (2) Oct trade balance (expected -$42.0 billion, Sep -$36.4 billion), (3) Oct factory orders (expected +2.5%, Sep +0.3% and +0.6% ex transportation).

Russell 1000 earnings reports today include: Toll Brothers (consensus $0.99), AutoZone (9.31), Michaels Cos (0.43), HD Supply Holdings (0.82).

U.S. IPO's scheduled to price today: Polar Power (POLA),

Equity conferences during the remainder of this week include: Raymond James Technology Investors Conference on Mon-Tue, UBS Global Media and Communications Conference on Mon-Wed, Barclays Gaming, Lodging, Leisure, Restaurant & Food Retail Conference on Tue, Cowen & Co Ultimate Energy Conference on Tue, Wells Fargo Securities Energy Symposium on Tue, Goldman Sachs U.S. Financial Services Conference on Tue-Wed, Wells Fargo Pipeline, MLP and Utility Symposium on Wed, Citi Global Health Care Conference on Wed-Thu, Barclays Global Technology, Media and Telecommunications Conference on Wed-Thu, Bernstein Consumer Summit on Wed-Thu, Capital One Southcoast Energy Conference on Wed-Thu, ACI European Biopolymer Summit on Thu.

OVERNIGHT U.S. STOCK MOVERS

Roper Technologies (ROP -0.37%) will buy Deltek for about $2.8 billion.

Nike (NKE +2.75%) was downgraded to 'Market Perform' from 'Outperform' at Cowen.

Pandora Media (P +0.30%) was upgraded to 'Outperform' from 'Market Perform' at Oppenheimer with an 18-month target price of $18.

McCormick (MKC +0.61%) was rated a 'Buy' at Vertical Group with a price target of $1.09.

Tyson Foods (TSN +0.39%) was rated a 'Buy' at Vertical Group with a price target of $67.

Bob Evans Farms (BOBE +2.30%) jumped over 5% in after-hours trading after it reported Q2 adjusted EPS of 56 cents, above consensus of 45 cents, and then raised guidance on 2017 adjusted EPS to $2.15-$2.30 from an August 31 view of $2.05-$2.20.

Kinder Morgan (KMI +0.47%) gained over 1% in after-hours trading after it said it sees a 50 cent a share dividend in 2017 and "delivering additional value to its shareholders in 2018."

Coupa Software (COUP -1.03%) climbed 6% in after-hours trading after it reported a Q3 adjusted loss of -22 cents a share, narrower than consensus of -47 cents, and said it sees a Q4 adjusted EPS loss of -16 cents to -19 cents, smaller than consensus of-23 cents.

Rent-A-Center (RCII +3.30%) slid 3% in after-hours trading after it said CFO Guy J. Constant resigned his position effective last Friday.

Lexicon Pharmaceuticals (LXRX +4.41%) tumbled over 12% in after-hours trading after a Phase 2 study of sotagliflozin did not reach statistical significance in young adults with Type 1 Diabetes.

Forum Energy Technologies (FET +5.22%) fell 5% in after-hours trading after it announced a public offering of 7 million shares of common stock.

TherapeuticsMD (TXMD +0.65%) surged almost 20% in after-hours trading after a Phase 3 trial of its TX-001HR drug met co-primary goals at multiple doses in postmenopausal women with moderate to severe vasomotor symptoms.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 +0.03%) this morning are up +1.00 point (+0.05%). Monday's closes: S&P 500 +0.58%, Dow Jones +0.24%, Nasdaq +0.82%. The S&P 500 on Monday closed higher on carry-over support from a rally in European stocks to a 3-week high on reduced concern about contagion of political risks from Italy to Europe. U.S. stocks were also boosted by signs of U.S. economic strength after the Nov ISM non-manufacturing index rose +2.4 to 57.2, stronger than expectations of +0.7 to 55.5 and the fastest pace of expansion in 13 months. Energy producer stocks received a boost as the price of crude oil rose to a 16-1/2 month high.

Mar 10-year T-notes (ZNH17 unch) this morning are down -1 tick. Monday's closes: TYH7 unch, FVH7 -3.00. Mar 10-year T-note futures on Monday closed little changed. T-note prices were undercut by reduced safe-haven demand after the failure of the Italian constitutional reform referendum didn't cause much consternation and after U.S. stocks rallied. T-note prices were also undercut by the larger-than-expected increase in the Nov ISM non-manufacturing index to its fastest pace of expansion in 13 months (+2.4 to 57.2). T-notes found some support after St. Louis Fed President Bullard said a single 25 bp increase in the fed funds rate "will get us very close" to the interest rate path recommended by the St. Louis Fed through 2019.

The dollar index (DXY00 +0.19%) this morning is up +0.190 (+0.19%). EUR/USD (^EURUSD) is down -0.0026 (-0.24%). USD/JPY (^USDJPY) is up +0.12 (+0.11%). Monday's closes: Dollar index -0.680 (-0.67%), EUR/USD +0.0100 (+0.94%), USD/JPY +0.34 (+0.30%). The dollar index on Monday closed lower on reduced safe-haven demand for the dollar after stocks recovered losses and moved higher as a 'No' vote for Italy's constitutional reforms was already factored into the market. EUR/USD rebounded from a 1-1/2 year low and rallied to a 2-week high on signs of economic strength in the Eurozone that may keep the ECB from expanding stimulus after Eurozone Oct retail sales rose +1.1% m/m, the biggest monthly increase in 2 years.

Jan WTI crude oil prices (CLF17 -1.08%) this morning are down -44 cents (-0.85%) and Jan gasoline (RBF17 -0.25%) is +0.0008 (+0.05%) . Monday's closes: Jan crude +0.11 (+0.20%), Jan gasoline -0.0101 (-0.65%). Jan crude oil and gasoline on Monday settled mixed with Jan crude at a 16-1/2 month high. Crude oil prices were boosted by the slide in the dollar index to a 2-week low and by continued support from last Wednesday's OPEC production cut agreement. Crude oil prices were undercut by news of a +200,000 bpd increase in OPEC Nov crude production to a record 34.160 million bpd.

Disclosure: None.