Morning Call For Tuesday, Dec. 5

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 +0.08%) this morning are up +0.08% as U.S. House and Senate lawmakers begin work on a compromise to tax-overhaul legislation. European stocks are down -0.36% as a slump in copper prices fuels a decline in mining stocks and commodity producers. Mar COMEX copper (HGH18 -2.04%) is down -2.10% at a 2-month low on concern a slowdown in China's economy will weaken its demand for industrial metals. European stocks also fell back after Eurozone Oct retail sales fell a more than expected -1.1% m/m, the largest monthly decline in 3-3/4 years. Asian stocks settled mostly lower: Japan -0.37%, Hong Kong -1.01%, China -0.18%, Taiwan -0.79%, Australia -0.23%, Singapore -0.01%, South Korea +0.26%, India -0.20%. Losses in technology stocks led Asian markets lower with China's Shanghai Composite falling to a 3-1/4 month low.

The dollar index (DXY00 -0.06%) is down -0.08%. EUR/USD (^EURUSD) is down -0.01%. USD/JPY (^USDJPY) is up +0.07%.

Mar 10-year T-note prices (ZNH18 unch) are unchanged.

The German Nov Markit services PMI was revised downward to 54.3 from the originally reported 54.9.

Eurozone Oct retail sales fell -1.1% m/m, weaker than expectations of -0.7% m/m and the biggest decline in 3-3/4 years.

The UK Nov Markit/CIPS services PMI fell -1.8 to 53.8, weaker than expectations of -0.6 to 55.0.

UK Nov new car registrations fell -11.2% to 163,541 and year-to-date are down -5.0% at 2,388,144.

U.S. STOCK PREVIEW

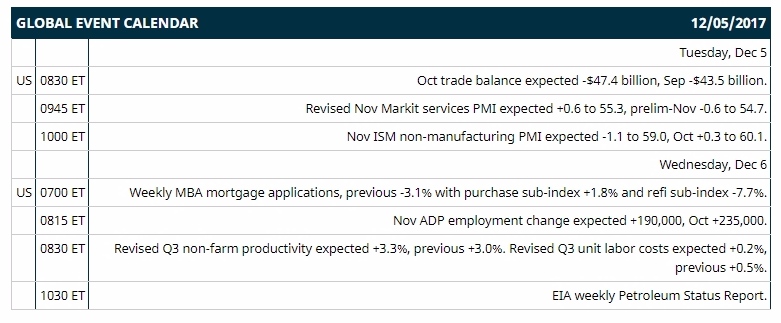

Key U.S. news today includes: (1) Oct trade deficit (expected -$47.4 billion, Sep -$43.5 billion), (2) revised-Nov Markit services US PMI (expected +0.6 to 55.3, prelim-Nov -0.6 to 54.7), (3) Nov ISM non-manufacturing (expected -1.1 to 59.0, Oct +0.3 to 60.1).

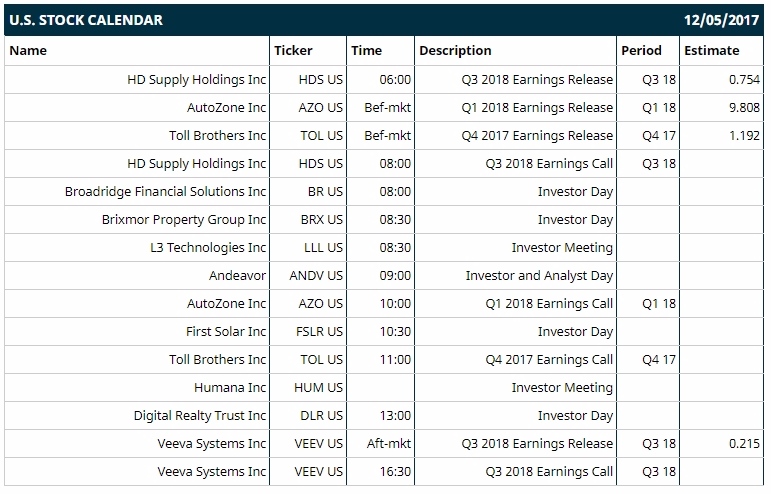

Notable Russell 1000 earnings reports today include: Toll Brothers (consensus $1.19), AutoZone (9.81), HD Supply (0.75), Veeva Systems (0.22).

U.S. IPO's scheduled to price today: none.

Equity conferences this week: Cowen Energy & Natural Resources Conference on Mon-Tue, Mizuho Americas Global Investor Conference on Mon-Tue, Raymond James Technology Conference on Mon-Wed, UBS Global Media and Communications Conference on Mon-Wed, Wells Fargo Event Information & Logistics Tech Summit on Mon-Wed, Global Mizuho Investor Conference on Tue, Goldman Sachs U.S. Financial Services Conference on Tue-Wed, Barclays Eat, Sleep, Play Conference on Tue-Wed, Nasdaq Investor Conference on Tue-Wed, NASDAQ Conference on Tue-Wed, Capital One Securities Energy Conference on Tue-Thu, Barclays Technology Conference on Wed, Berenberg Bank European Healthcare Conference on Wed, BIOMEDevice Conference on Wed, Barclays Global Technology, Media and Telecommunications Conference on Wed-Thu, Wells Fargo Pipeline MLP and Energy Symposium on Wed-Thu, Citi Global Health Care Conference on Wed-Thu, th Capital Utah Corporate Access Event Conference on Wed-Thu, Bank of America Merrill Lynch Emerging Technology Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Allegiant Travel (ALGT +2.92%) was downgraded to 'Neutral' from 'Buy' at Buckingham Research Group.

United Technologies (UTX -0.07%) was upgraded to 'Overweight' from 'Neutral' at Atlantic Equities LLP with a target price of $145.

McDonald's (MCD -1.28%) was upgraded to 'Buy' from 'Hold' at Jeffries with a price target of $200.

Stephens initiated coverage of DowDuPont (DWDP +1.58%) with a recommendation of 'Overweight.'

Marathon Oil (MRO -1.19%) was upgraded to 'Overweight' from 'Neutral' at Atlantic Equities LLP with a price target of $17.50.

Robert W. Baird initiated coverage of Curtiss-Wright (CW -2.16%) with a recommendation of 'Outperform' with a 12-month target price of $149.

Kinder Morgan (KMI -0.92%) may move higher initially this morning after it said it sees 2018 preliminary adjusted Ebitda of $7.5 billion, above consensus of $7.4 billion.

Performance Food Group (PFGC +5.41%) slipped 3% in after-hours trading after it announced a secondary offering of 6.272 million shares of its common stock on the behalf of an affiliate of Wellspring Capital Management.

Collegium Pharmaceutical (COLL -0.35%) rose 6% in after-hours trading after it entered into a commercialization pact with Depomed for the Nucynta drug.

Heron Therapeutics (HRTX -0.58%) slumped 9% in after-hours trading after it was said to have offered $150 million in shares via Cantor Fitzgerald priced between $1550-$16.25.

Cleveland-Cliffs (CLF -1.03%) tumbled over 6% in after-hours trading after it announced a proposed offering of $400 million of senior secured notes due 2014.

Ascena Retail Group (ASNA +5.67%) plunged 20% in after-hours trading after it reported Q1 comparable sells fell -5%, wider than consensus of -4.1%, and said it sees Q2 adjusted EPS loss per share of -7 cents to -12 cents, the mid-point wider than consensus for a loss of -7.5 cents a share.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 +0.08%) this morning are up +2.00 points (+0.08%). Monday's closes: S&P 500 -0.11%, Dow Jones +0.24%, Nasdaq -1.17%. The S&P 500 on Monday rallied to a new record high early but then drifted lower into the close and settled lower. Stocks were undercut by a slide technology stocks led by a -3.7% decline in Microsoft and by weakness in energy stocks after crude oil prices fell -1.53%. The S&P 500 showed some strength early after the Senate passed a corporate tax-cut plan late last Friday night.

Mar 10-year T-note prices (ZNH18 unch) this morning are unch. Monday's closes: TYH8 -5.50, FVH8 -5.25. Mar 10-year T-notes on Monday closed lower on the stronger-than-expected U.S. Oct factory orders report and on the early rally in the S&P 500 to a new record high, which curbed the safe-haven demand for T-notes. T-notes were also undercut by increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 2-1/2 week high.

The dollar index (DXY00 -0.06%) this morning is down -0.076 (-0.08%). EUR/USD (^EURUSD) is down -0.0001 (-0.01%) and USD/JPY (^USDJPY) is up +0.08 (+0.07%). Monday's closes: Dollar Index +0.303 (+0.33%), EUR/USD -0.0030 (-0.25%), USD/JPY +0.07 (+0.06%). The dollar index on Monday closed higher on optimism about U.S. tax reform after the Senate passed corporate tax-cut legislation late last Friday night. In addition, USD/JPY rallied to a 2-week high as the rally in the S&P 500 to a 2-week high reduced the safe-haven demand for the yen.

Jan crude oil (CLF18 -0.64%) this morning is down -32 cents (-0.56%) and Jan gasoline (RBF18 +0.20%) is +0.0045 9+0.27%). Monday's closes: Jan WTI crude -0.89 (-1.53%), Jan gasoline -0.0494 (-2.84%). Jan crude oil and gasoline on Monday closed lower with Jan gasoline at a 1-month low. Crude oil prices were undercut by a stronger dollar and by concern that the recent rise in crude prices will provide incentive to U.S. shale oil producers to increase production after Friday's data from Baker Hughes showed U.S. active oil rigs in the week ended Dec 1 rose by 2 rigs to a 2-month high of 749 rigs.

Metals prices this morning are mixed with Feb gold (GCG18 +0.02%) +0.8 (+0.06%), Mar silver -(SIH18 -0.42%) 0.053 (-0.32%) and Mar copper (HGH18 -2.04%) -0.065 (-2.10%) at a 2-month low. Monday's closes: Feb gold -4.6 (-0.36%), Mar silver -0.015 (-0.09%), Mar copper -0.0025 (-0.08%). Metals on Monday closed lower on a stronger dollar and the rally in the S&P 500 to a new record high, which reduced the safe-haven demand for precious metals. Copper found some underlying support on signs of tighter copper supplies after LME copper inventories fell -1,100 MT to a 1-1/2 year low of 182,425 MT.

Disclosure: None.