Morning Call For Tuesday, April 18

OVERNIGHT MARKETS AND NEWS

Jun E-mini S&Ps (ESM17 -0.22%) this morning are down -0.30% and European stocks are down -0.98% at a 3-week low as weakness in energy producing stocks and mining companies drags the overall market lower. May WTI crude oil (CLK17-0.85%) is down -0.78% at a 1-week low on concern that U.S. shale oil production is ramping up after the latest data showed active U.S. oil rigs last week increased to their highest in 1-1/2 years. Freeport McMoRan and U.S. Steel are both down more than 1% in pre-market trading as iron ore prices tumbled to a 4-3/4 month low after Citigroup said it was bearish in the outlook for the metal. GBP/USD jumped +0.79% to a 2-1/2 month high after British Prime Minister May announced as early general election set for June 8 as she seeks approval from voters as she heads into negotiations with the EU over Brexit. Also weighing on European stocks is political risks from this Sunday's presidential election in France that is still too close to call. Asian stocks settled mostly lower: Japan +0.35%, Hong Kong -1.39%, China -0.79%, Taiwan +0.31%, Australia -0.90%, Singapore -0.02%, South Korea +0.05%, India -0.32%. China's Shanghai Composite fell to a 2-week low as tensions on the Korean peninsula along with tougher regulatory scrutiny on stock trading led to selling of Chinese stocks.

The dollar index (DXY00 -0.27%) is down -0.17%. EUR/USD (^EURUSD) is up +0.24%. USD/JPY (^USDJPY) is down -0.03%.

Jun 10-year T-note prices (ZNM17 +0.11%) are up +7 ticks.

China Mar new home prices rose in 62 out of the 70 cities tracked by the government, the most in 5 months.

U.S. STOCK PREVIEW

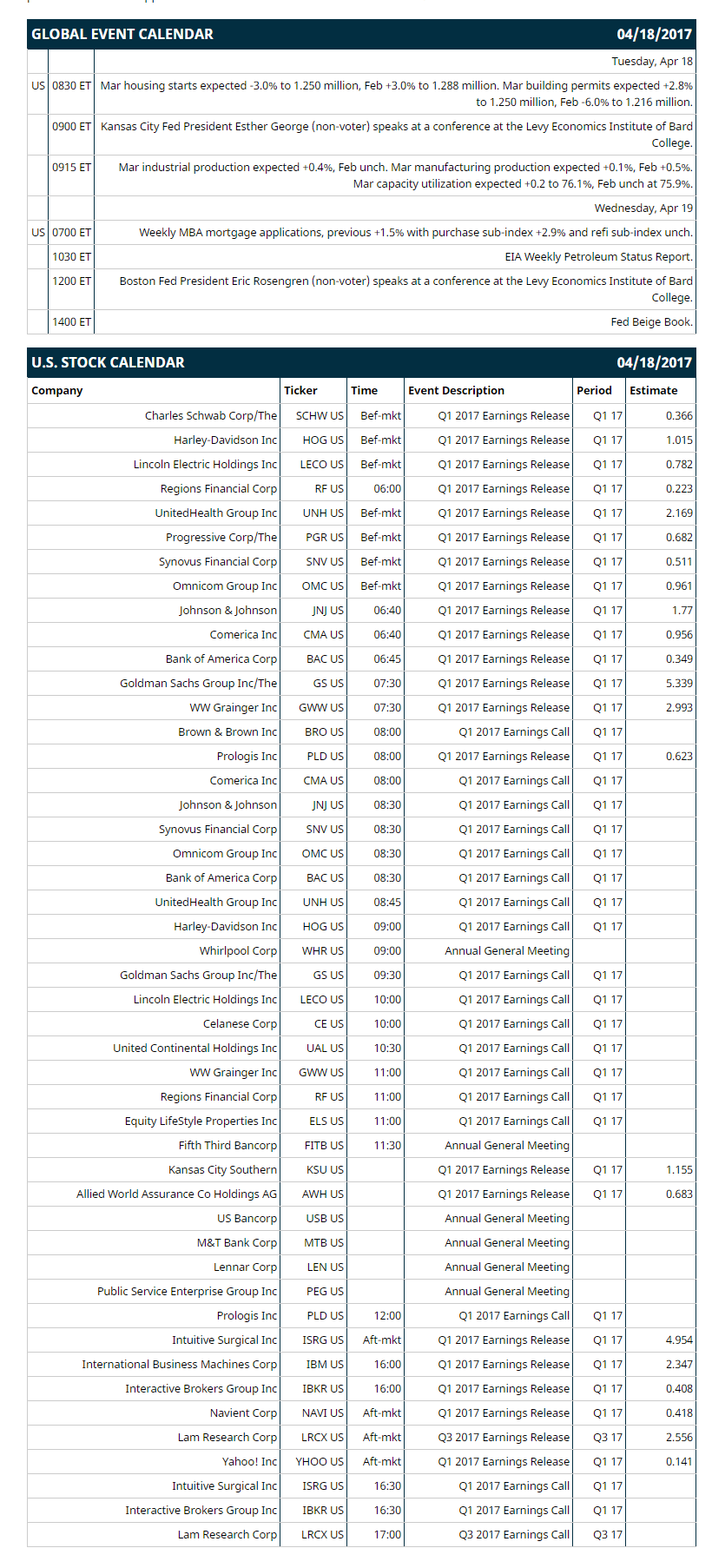

Key U.S. news today includes: (1) Mar housing starts (expected -3.0% to 1.250 million, Feb +3.0% to 1.288 million), (2) Kansas City Fed President Esther George (non-voter) speaks at a conference at the Levy Economics Institute of Bard College, (3) Mar industrial production (expected +0.4%, Feb unch).

Notable Russell 1000 earnings reports today include: Goldman Sachs (consensus $5.34), Bank of America (0.35), IBM (2.35), Charles Schwab (0.37), Yahoo (0.14), Navient (0.42), Harley-Davidson (1.02), Kansas City Southern (1.16), Johnson & Johnson (1.77), UnitedHealth Group (2.17).

U.S. IPO's scheduled to price today: none.

Equity conferences: none.

OVERNIGHT U.S. STOCK MOVERS

Goldman Sachs (GS +1.32%) dropped over 2% in pre-market trading after it reported Q1 net revenue of $8.03 billion, weaker than consensus of $8.33 billion.

Harley-Davidson (HOG -0.50%) slumped 5% in pre-market trading after it reported Q1 total motorcycles and related products revenue of $1.33 billion, below consensus of $1.35 billion.

Netflix (NFLX +3.03%) rose over 1% in after-hours trading after it reported 3.2 million new subscribers in Q2, higher than consensus of 2.5 million.

First Horizon National (FHN +1.93%) was upgraded to 'Outperform' from 'Market Perform' at Vining Sparks with a 12-month target price of $21.

United Continental Holdings (UAL +2.46%) gained over 1% in after-hours trading after it reported Q1 adjusted EPS of 41 cents, above consensus of 38 cents.

Synovus (SNV +2.05%) reported Q1 adjusted EPS of 57 cents, higher than consensus of 51 cents.

Celanese (CE +1.50%) reported Q1 adjusted EPS of $1.81, better than consensus of $1.72.

Galapagos NV (GLPG +2.71%) slipped over 2% in after-hours trading after it announced that it will share $275 million in American Depository Shares (ADS) via Morgan Stanley.

Barracuda Networks (CUDA +1.08%) dropped nearly 3% in after-hours trading after it said it expects fiscal 2018 revenue of $370 million-$380 million, the midpoint which trails consensus of $378.1 million.

Agios Pharmaceuticals (AGIO +0.33%) lost 3% in after-hours trading after it proposed selling up to 4.5 million shares of its common stock in an underwritten public offering.

Cabela's (CAB +0.56%) rallied 6% in after-hours trading after it announced an amended deal with Bass Pro Shops who will buy Cabela's for $61.50 a share versus an October 2016 offer of $65.50 a share.

Rigel Pharmaceuticals (RIGL +0.32%) gained almost 2% in after-hours trading after it submitted to the FDA an NDA for its fostamatinib drug for patients with chronic and persistent immune thrombocytopenia.

Wi-LAN (WILN +1.01%) jumped 10% in after-hours trading after it announced a pact to buy International Road Dynamics for $47.4 million.

MARKET COMMENTS

Jun E-mini S&Ps (ESM17 -0.22%) this morning are down -7.00 points (-0.30%). Monday's closes: S&P 500 +0.86%, Dow Jones +0.90%, Nasdaq +0.85%. The S&P 500 on Monday closed higher on optimism about the global growth prospects after China Q1 GDP rose +6.9% y/y, stronger than expectations of +6.8% y/y and the fastest pace of growth since Q3 of 2015. Stocks also received a boost from optimism about S&P 500 Q1 corporate quarterly earnings results that are expected to increase +10.4% y/y. Stocks were undercut by the -11.2 point decline in the U.S. Apr Empire manufacturing index to a 5-month low of 5.2, weaker than expectations of -1.4 to 15.0.

Jun 10-year T-notes (ZNM17 +0.11%) this morning are up +7 ticks. Monday's closes: TYM7 -5.50, FVM7 -2.00. Jun 10-year T-notes on Monday fell back from a 5-month nearest-futures high and closed lower. T-note prices were undercut by the stronger-than-expected Chinese Q1 GDP report and by reduced safe-haven demand for T-notes after stocks rallied and the North Korean situation calmed down a little.

The dollar index (DXY00 -0.27%) this morning is down -0,17 (-0.17%). EUR/USD (^EURUSD) is up +0.0026 (+0.24%) and USD/JPY (^USDJPY) is down -0.03 (-0.03%). Monday's closes: Dollar index -0.22 (-0.22%), EUR/USD +0.0025 (+0.24%), USD/JPY +0.27 (+0.25%). The dollar index on Monday fell to a 2-week low and closed lower on last Friday's U.S. Mar CPI data, which was dovish for Fed policy since it showed Mar core CPI fell -0.1% m/m, the first monthly decline in 7 years. The dollar was also undercut by the weaker than expected U.S. Mar Empire manufacturing index of -11.2 to a 5-month low of 5.2.

May WTI crude oil prices (CLK17 -0.85%) this morning are down -41 cents (-0.78%) and May gasoline (RBK17 -0.96%) is down -0.0150 (-0.87%, both at 1-week lows. Monday's closes: May crude -0.53 (-1.00%), May gasoline -0.0153 (-0.88%). May WTI crude oil and gasoline on Monday closed lower on concern about increasing U.S. crude production after last Friday's data from Baker Hughes showed U.S. active oil rigs in the week ended Apr 14 rose +11 to 683, the most in 1-3/4 years. In addition, the crack spread fell to a 3-week low, which may curb refinery demand for crude to refine into gasoline. Crude oil prices found some support on the fall in the dollar index to a 2-week low.

Disclosure: None.