Morning Call For Thursday, Oct. 12

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 -0.21%) this morning are down -0.15% and European stocks are down -0.19% as weakness in crude oil prices drags energy stocks lower. Nov WTI crude oil (CLX17 -1.54%) is down -1.54% after API data late Wednesday showed that U.S. crude stockpiles rose +3.1 million bbl last week. Also, a -0.6% decline in JPMorgan Chase in pre-market trading is undercutting stock indexes after it reported Q3 FICC sales and trading revenue of $3.16 billion, below consensus of $3.18 billion. A rally in mining stocks is limiting the downside in equity markets as metals prices moved higher. Dec COMEX gold (GCZ17 +0.71%) is up +0.64% and Dec silver (SIZ17 +0.71%) climbed +0.60% to 2-week highs and Dec copper (HGZ17 +0.57%) is up +0.44% and posted a 1-month high after the minutes of the Sep 19-20 FOMC meeting on Wednesday afternoon showed policy makers were concerned about low inflation, which may keep the Fed from additional rate hikes. Losses in European stocks were contained after Eurozone Aug industrial production rose a more-than-expected +1.4% m/m, the biggest increase in 9-months. Asian stocks settled mostly higher: Japan +0.35%, Hong Kong +0.24%, China -0.06%, Taiwan +0.66%, Australia +0.39%, Singapore +0.70%, South Korea +0.61%, India +1.09%. Japan's Nikkei Stock Index rose to a fresh 2-year high on optimism that Prime Minister Abe's party will retain its dominant position in Japan's parliament when voters go to the polls on Oct 22.

The dollar index (DXY00 +0.03%) is up +0.05%. EUR/USD (^EURUSD) is down -0.01% and fell back from a 2-week high after ECB Executive Board member Praet said "a very substantial degree of monetary accommodation is still needed" to bolster Eurozone inflation. USD/JPY (^USDJPY) is down -0.18%.

Dec 10-year T-note prices (ZNZ17 +0.12%) are up +3 ticks.

ECB Executive Board member Praet said "a very substantial degree of monetary accommodation is still needed" to bolster Eurozone inflation. "Deflationary risks have disappeared and some measures of underlying inflation have ticked up over recent months, but overall inflation developments, despite the solid growth, have remained subdued."

Eurozone Aug industrial production rose +1.4% m/m, stronger than expectations of +0.6% m/m and the largest increase in 9-months.

Japan Sep PPI rose +0.2% m/m and +3.0% y/y, right on expectations with the +3.0% y/y gain the largest year-on-year increase in 3-years.

U.S. STOCK PREVIEW

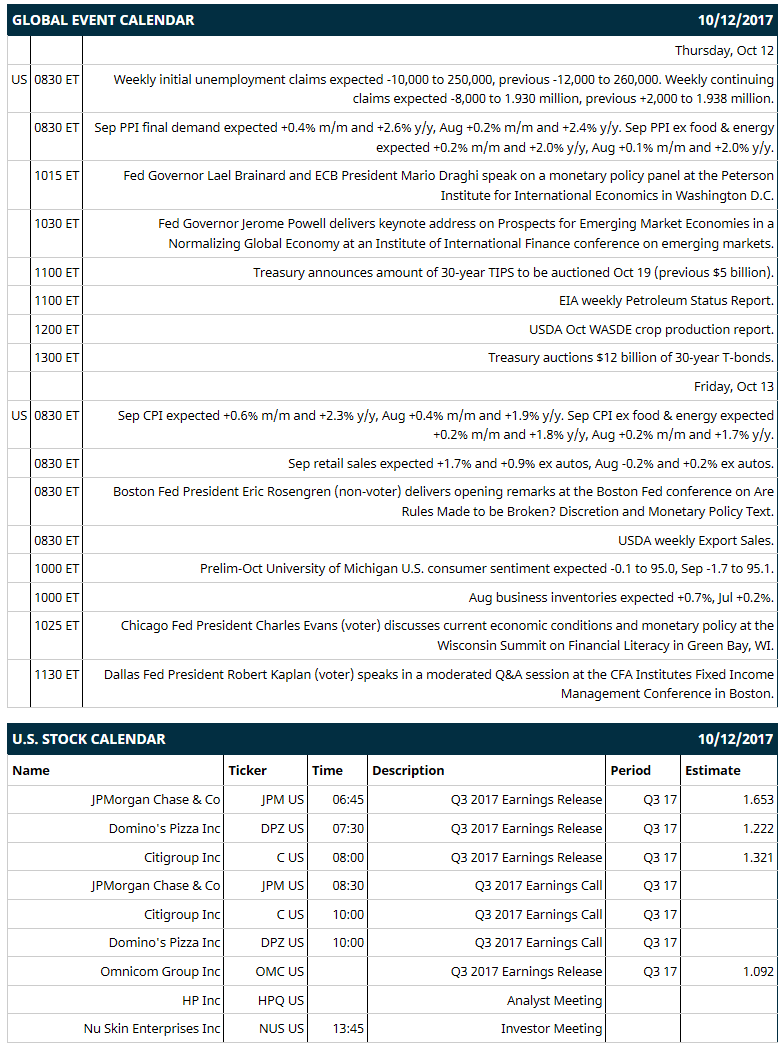

Key U.S. news today includes: (1) weekly initial unemployment claims (expected -10,000 to 250,000, previous -12,000 to 260,000) and continuing claims (expected -8,000 to 1.930 million, previous +2,000 to 1.938 million), (2) Sep PPI final demand (expected +0.4% m/m and +2.6% y/y, Aug +0.2% m/m and +2.4% y/y) and Sep PPI ex food & energy (expected +0.2% m/m and +2.0% y/y, Aug +0.1% m/m and +2.0% y/y), (3) Fed Governor Lael Brainard and ECB President Mario Draghi speak on a monetary policy panel at the Peterson Institute for International Economics in Washington D.C., (4) Fed Governor Jerome Powell delivers keynote address on “Prospects for Emerging Market Economies in a Normalizing Global Economy” at an Institute of International Finance conference on emerging markets, (5) Treasury auctions $12 billion of 30-year T-bonds, (6) EIA weekly Petroleum Status Report, (7) USDA Oct WASDE crop production report.

Notable Russell 1000 earnings reports today include: JPMorgan Chase (consensus $1.65), Citigroup (1.32), Omincom Group (1.09), Domino's Pizza (1.22).

U.S. IPO's scheduled to price today: Optinose (OPTN).

Equity conferences this week: HR Technology Conference on Tue-Fri, National HUBZone Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM -0.30%) is down -0.6% in pre-market trading after it reported Q3 FICC sales and trading revenue of $3.16 billion, below consensus of $3.18 billion.

Disney (DIS -1.03%) was downgraded to 'Neutral' from 'Buy' at Guggenheim Securities.

Williams-Sonoma (WSM -1.38%) was downgraded to 'Underperform' from 'Neutral' at Credit Suisse with a price target of $44.

Host Hotels (HST +0.65%) was upgraded to 'Buy' from 'Hold' at Deutsche Bank with a price target of $21.

Square (SQ +2.17%) was initiated as a new 'Outperform' at Oppenheimer with a price target of $35.

Juniper Networks (JNPR -1.65%) slid nearly 3% in after-hours trading after it reported preliminary Q3 revenue of $1.25 billion-$1.26 billion, below a prior estimate of $1.29 billion-$1.35 billion and below consensus of $1.33 billion.

NanoString Technologies (NSTG +0.13%) dropped nearly 10% in after-hours trading after it reported preliminary Q3 revenue of $25.9 million-$26.9 million, below consensus of $27.7 million.

Blackhawk Network Holdings (HAWK -0.90%) fell almost 7% in after-hours trading after it said it sees full-year adjusted EPS of $1.56 to $1.70, the midpoint below consensus of $1.68.

Protagonist Therapeutics (PTGX +0.71%) slumped over 10% in after-hours trading after it proposed an underwritten public offering of $50 million of its common stock.

Kandi Technologies Group (KNDI -7.82%) dropped over 5% in after-hours trading after it filed a $300 million shelf of mixed securities.

Babcock & Wilcox Enterprises (BW +4.22%) rose almost 6% in after-hours trading after Viex Capital reported a 6.4% stake in the company.

J. Jill (JILL -2.17%) plunged 35% in after-hours trading after it cut its Q3 adjusted EPS estimate to 8 cents-10 cents from an Aug 29 estimate of 18 cents-20 cents, citing lower than expected sales trends across retail and direct channels.

Ardelyx (ARDX unch) surged 45% in after-hour trading after it said its tenapanor drug for treatment of irritable bowel syndrome with constipation met statistical significance for the primary endpoint and all secondary endpoints in the second Phase 3 study.

Sigma Designs (SIGM +0.77%) rose almost 4% in after-hours trading after it said it will cut between 200 to 250 positions worldwide under its restructuring plan.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 -0.21%) this morning are down -3.75 points (-0.15%). Wednesday's closes: S&P 500 +0.18%, Dow Jones +0.18%, Nasdaq +0.29%. The S&P 500 on Wednesday climbed to a new record high and settled higher on carry-over support from a rally in European stocks on reduced Spanish political concerns after Catalan President Puigdemont said he would seek talks with the Spanish government over the future of Catalonia rather than seek immediate independence. US stocks also received a boost from the minutes of the Sep 19-20 FOMC meeting that said some policy makers did not want to raise interest rates until they were confident inflation would rise to their 2% target.

Dec 10-year T-note prices (ZNZ17 +0.12%) this morning are up +3 ticks. Wednesday's closes: TYZ7 -1.00, FVZ7 -1.75. Dec 10-year T-notes on Wednesday closed slightly lower on increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 5-month high. Losses were limited by dovish comments from Dallas Fed President Kaplan who said that he is "really nervous" that inflation expectations are low, which suggests that he may not support a Fed rate hike in Dec.

The dollar index (DXY00 +0.03%) this morning is up +0.044 (+0.05%). EUR/USD (^EURUSD) is down -0.0001 (-0.01%) and USD/JPY (^USDJPY) is down -0.20 (-0.18%). Wednesday's closes: Dollar Index -0.275 (-0.29%), EUR/USD +0.0051 (+0.43%), USD/JPY +0.05 (+0.04%). The dollar index on Wednesday fell to a 1-week low and closed lower on strength in EUR/USD which climbed to a 2-week high as Spanish political concerns eased after Catalan President Puigdemont said he is looking to negotiate with the Spanish government rather than seeking immediate independence. The dollar was also undercut by the Sep 19-20 FOMC meeting minutes that showed policy makers were concerned about persistently low inflation.

Nov crude oil (CLX17 -1.54%) this morning is down -79 cents (-1.54%) and Nov gasoline (RBX17 -0.80%) is -0.0127 (-0.79%). Wednesday's closes: Nov WTI crude +0.38 (+0.75%), Nov gasoline +0.0177 (+1.11%). Nov crude oil and gasoline on Wednesday closed higher with Nov crude at a 1-week high. Crude oil prices were boosted by the fall in the dollar index to a 1-week low and by expectations for EIA crude inventories on Thursday to fall -750,000 bbl. Crude oil prices were undercut by the EIA's hike in its 2018 U.S. crude output estimate to 9.92 million bpd from 9.84 million bpd.

Metals prices this morning are higher with Dec gold (GCZ17 +0.71%) +8.3 (+0.64%) at a 2-week high, Dec silver (SIZ17 +0.71%) +0.102 (+0.60%) at a 2-week high and Dec copper (HGZ17 +0.57%) +0.014 (+0.44%) at a 1-month high. Wednesday's closes: Dec gold -4.9 (-0.38%), Dec silver -0.074 (-0.43%), Dec copper +0.0350 (+1.14%). Metals on Wednesday settled mixed with Dec copper at a 1-month high. Metals prices were supported by the fall in the dollar index to a 1-week low and by tighter copper supplies after LME copper inventories fell -2,955 MT to a 3-1/2 week low of 286,925 MT. Precious metals prices were undercut by reduced safe-haven demand as Spanish political risks eased.

(Click on image to enlarge)

Disclosure: None.