Morning Call For Thursday, Nov. 10

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 +0.32%) are up +0.58% at a 2-month high as drug makers and bank stocks rallied in pre-market trading on speculation the Trump administration will mean less regulatory oversight in those sectors than had Mrs. Clinton won. Allergan Plc, Pfizer, Goldman Sachs and JPMorgan Chase are all up over 1% in pre-market trading. Mining stocks and raw-material producers are also higher with the price of copper (HGZ16 +3.88%) up +4.07% at a 1-1/3 year high on optimism that a Trump presidency and a Republican-controlled Congress will lower taxes, ease corporate regulation and ramp up infrastructure spending to spur economic growth. European stocks are up +1.09% at a 2-week high as bank stocks rallied on speculation the Trump administration will review the strict capital rules applied during the Obama administration, while mining stocks gained with the rally in copper to a 1-1/3 year high. Asian stocks settled higher: Japan +6.82%, Hong Kong +1.89%, China +1.37%, Taiwan +2.34%, Australia +3.34%, Singapore +1.58%, South Korea +2.26%, India +0.97%. Asian stocks reversed course from Wednesday's plunge and rallied sharply as China's Shanghai Composite climbed to a 10-month high after the rally in copper prices boosted raw-material producers, although the Chinese yuan tumbled to a 6-year low of 6.7992 per dollar on concern over President-elect Trump's trade policies. Japanese stocks jumped as exporters rallied sharply after USD/JPY climbed to a 3-1/2 month high, which improves the earnings prospects of exporting companies.

The dollar index (DXY00 +0.54%) is up +0.31% at a 1-1/2 week high. EUR/USD (^EURUSD) is down -0.23% at a 1-1/2 week low. USD/JPY (^USDJPY) is up +1.16% at a 3-1/2 month high.

Dec 10-year T-note prices (ZNZ16 -0.29%) are down -9.5 ticks at a 9-3/4 month nearest-futures low on speculation the Trump administrations economic policies will boost inflation.

San Francisco Fed President Williams (non-voter) said there's "always" going to be "some" uncertainty or volatility; don't see that as fundamentally different post-election, and that the argument for gradual rate increases "still makes sense to me."

U.S. STOCK PREVIEW

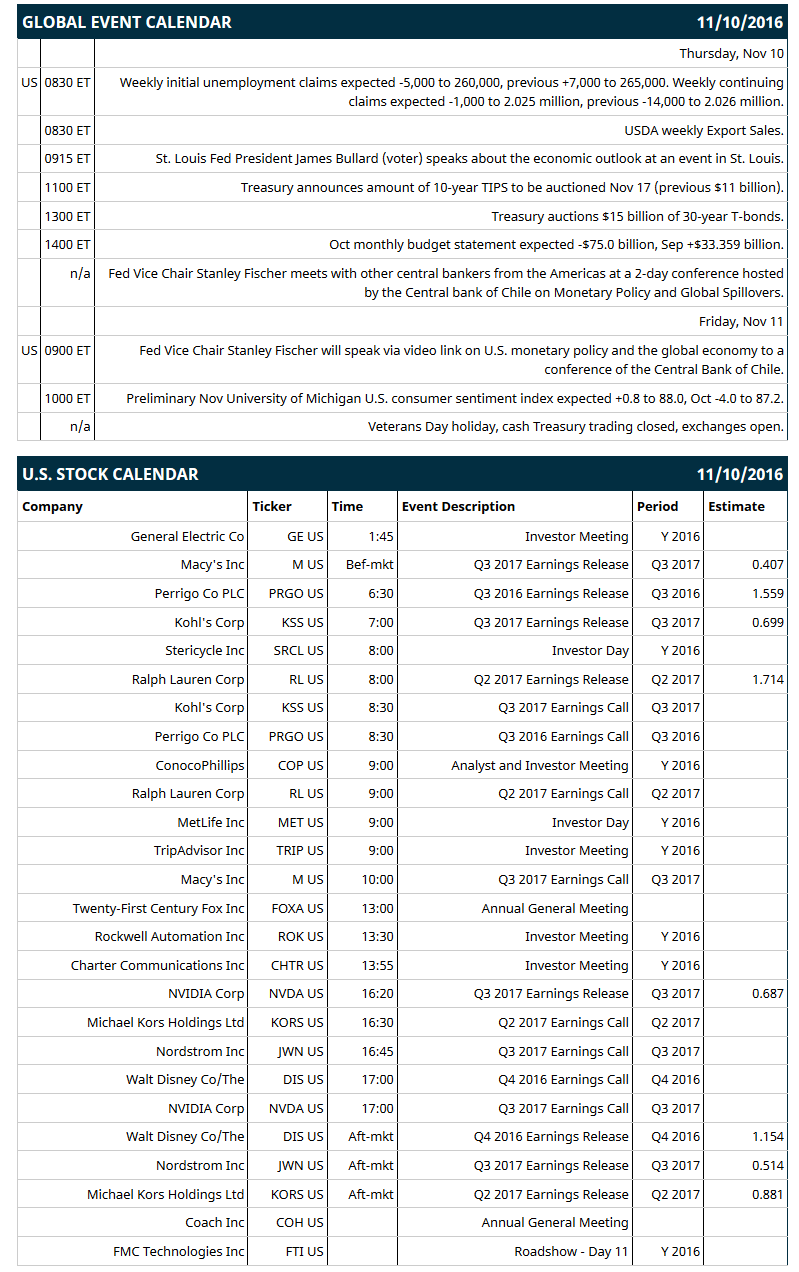

Key U.S. news today includes: (1) weekly initial unemployment claims (expected -5,000 to 260,000, previous +7,000 to 265,000) and continuing claims (expected -1,000 to 2.025 million, previous -14,000 to 2.026 million), (2) St. Louis Fed President James Bullard (voter) speaks about the economic outlook at an event in St. Louis, (3) the Treasury's auction of $15 billion of 30-year T-bonds, (4) Oct monthly budget statement (expected -$75.0 billion, Sep +$33.359 billion), (5) Fed Vice Chair Stanley Fischer meets with other central bankers from the Americas at a 2-day conference hosted by the Central bank of Chile on “Monetary Policy and Global Spillovers," and (6) USDA weekly Export Sales.

Notable S&P 500 earnings reports today include: Macy's (consensus $0.41), Kohl's (0.70), Perrigo (1.56), Ralph Lauren (1.71), NVIDIA (0.69), Disney (1.15), Nordstrom (0.51), Michael Kors (0.88).

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week include: Robert W. Baird Global Industrial Conference on Mon-Thu, RBC Technology Internet Media and Telecommunications Conference on Wed-Thu, Wells Fargo Technology, Media & Telecom Conference on Wed-Fri, Citi Financial Technology Conference on Thu, SunTrust Robinson Humphrey Financial Technology, Business & Government Services on Thu.

OVERNIGHT U.S. STOCK MOVERS

Urban Outfitters (URBN +4.49%) was upgraded to 'Buy' from 'Hold' at Wunderlich Securities with an 18-month target price of $40.

Shake Shack (SHAK +2.15%) jumped 8% in after-hours trading after it raised its full-year sales forecast to $264 million-$265 million from a previous estimate of $256 million.

Mylan (MYL +4.88%) lost almost 1% in after-hours trading after it reported Q3 adjusted EPS of $1.38, below consensus of $1.45.

TASER International (TASR +5.25%) rallied 9% in after-hours trading after it reported Q3 net sales of $71.9 million, well above consensus of $59 million.

Alexion Pharmaceuticals (ALXN +6.54%) slid 2% in after-hours trading after it filed to delay its 10-Q and said it is investigating whether personnel engaged in sales practices that were inconsistent with company policies.

Rapid7 (RPD +1.43%) sank 10% in after-hours trading after it said it sees a Q4 adjusted loss of -26 cents to -28 cents, a wider loss than consensus of -24 cents.

Zeltiq Aesthetics (ZLTQ -1.49%) rallied nearly 8% in after-hours trading after it reported Q3 EPS of 12 cents, higher than consensus of 9 cents, and then raised its full-year revenue estimate to $350 million-$352 million from an August 8 view of $240 million-$350 million.

SolarEdge Technologies (SEDG -5.41%) fell 5% in after-hours trading after it reported Q1 revenue of $128.5 million, below consensus of $132.4 million.

Tabula Rasa Healthcare (TRHC +3.46%) rose nearly 5% in after-hours trading after it reported Q3 adjusted EPS of 6 cents, better than consensus of 4 cents, and said it sees Q4 revenue of $25 million-$26 million, above consensus of $22.9 million.

Avid Technology (AVID +4.46%) dropped over 10% in after-hours trading after it lowered guidance on full-year GAAP revenue to $502 million-$517 million from a prior view of $535 million-$565 million.

Merrimack Pharmaceuticals (MACK +13.87%) lost nearly 8% in after-hours trading after it reported Q3 total revenue of $28.1 million, well below estimates of $41 million.

Bovie Medical (BVX -0.64%) slid nearly 6% in after-hours trading after it announced primary and secondary offerings of common stocks.

Harmonic (HLIT +8.08%) slumped over 20% in after-hours trading after it reported an unexpected Q3 adjusted loss of -1 cent, weaker than consensus of a 2 cent profit, and then said it sees Q4 adjusted EPS of 5 cents-7 cents, below consensus of 13 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 +0.32%) this morning are up +12.50 points (+0.58%) at a 2-month high. Wednesday's closes: S&P 500 +1.11%, Dow Jones +1.40%, Nasdaq +0.42%. The S&P 500 on Wednesday recovered from sharp overnight losses and rallied to a 4-week high to close with moderately large gains. Stocks were boosted by Mr. Trump's conciliatory acceptance speech and by hopes that president-elect Trump and the Republican-controlled Congress will pursue business-friendly policies that boost economic growth. Global stock prices initially plunged on fears that Mr. Trump may start trade wars that lead to reduced global trade.

Dec 10-year T-notes (ZNZ16 -0.29%) this morning are down -9.5 ticks at a 9-3/4 month nearest-futures low. Wednesday's closes: TYZ6 -1-15.00, FVZ6 -22.00. Dec 10-year T-notes on Wednesday spiked up to a 1-month high in overnight trade after global stocks plunged, but then gave up their gains and dropped to a contract low to finally close sharply lower. T-notes were hurt by expectations that Mr. Trump will pursue aggressive fiscal stimulus plans that boost the budget deficit and that potentially cause the economy to run hot, thus boosting inflation. The 10-year T-note breakeven inflation rate yesterday jumped to a 1-1/4 year high. T-notes were also hurt by talk that Mr. Trump will pressure the Fed for rate hikes.

The dollar index (DXY00 +0.54%) this morning is up +0.305 (+0.31%) at a 1-1/2 week high. EUR/USD (^EURUSD) is down -0.0025 (-0.23%) at 1-1/2 week low. USD/JPY (^USDJPY) is up +1.23 (+1.16%) at a 3-1/2 month high. Wednesday's closes: Dollar index +0.643 (+0.66%), EUR/USD -0.0116 (-1.05%), USD/JPY +0.51 (+0.48%). The dollar index on Wednesday slumped to a 1-month low in overnight trade but then rebounded to a 1-week high and closed higher. The dollar was boosted by expectations for more aggressive Fed tightening on pressure from Mr. Trump. There was also weakness in EUR/USD which fell back from a 2-month high and posted a 1-week low on concern the ECB may need to maintain its stimulus measures after the European Commission cut its Eurozone 2017 GDP forecast to 1.5% from a 1.8% estimate in May.

Dec crude oil prices (CLZ16 -0.91%) are down -19 cents (-0.42%) and Dec gasoline (RBZ16 +0.38%) is up +0.0101 (+0.74%). Wednesday's closes: Dec crude +0.29 (+0.64%), Dec gasoline -0.0114 (-0.83%). Dec crude and gasoline on Wednesday settled mixed with Dec gasoline at a 2-month low. Crude oil prices were boosted by hopes that Mr. Trump's pro-business policies will boost economic growth and energy demand and by the -2.84 million bbl drop in EIA gasoline supplies to a 10-1/2 month low (more than expectations of -1.5 million bbl). Crude oil prices were undercut by the higher close in the dollar index, the +2.43 million bbl increase in EIA crude inventories (more than expectations of +2.0 million bbl), and the +2.0% increase in U.S. crude production in the week of Nov 4 to 8.692 million bpd, a 4-3/4 month high.

(Click on image to enlarge)

Disclosure: None.