Morning Call For Thursday, March 16

OVERNIGHT MARKETS AND NEWS

Jun E-mini S&Ps (ESM17 +0.25%) this morning are up +0.25% at a 2-week high and European stocks are up +1.16% at a 1-1/4 year high on a less hawkish Fed and after pro-Europe parties won elections in the Netherlands. The FOMC did not signal a faster pace of tightening as they kept their projections for two more 25 bp rate hikes this year and Fed Chair Yellen said that the "simple message is the economy is doing well." Reduced European political risks gave European stocks an added boost after the pro-EU Liberal party beat the anti-EU Freedom Party in the Netherlands elections. Asian stocks settled higher: Japan +0.07%, Hong Kong +2.08%, China +0.84%, Taiwan +1.00%, Australia +0.20%, Singapore +0.83%, South Korea +0.80%, India +0.64%. China's Shanghai Composite rallied to a 3-1/2 month high after the PBOC followed the Fed's rate hike by raising rates on its open-market operations and on its medium-term lending facility and said that raising open-market rates don't necessarily equate to interest rate hikes. The PBOC's move to follow the Fed may be an attempt to limit capital outflows as the yuan jumped to a 1-week high against the dollar after the move. The BOJ as expected kept its benchmark rate unchanged at -0.1% and said that Japan's economy was on a "moderate recovery trend."

The dollar index (ZNM17 -0.16%) is down -0.12% at a 1-month low. EUR/USD (^EURUSD) is down -0.06%. USD/JPY (^USDJPY) is up +0.11%.

Jun 10-year T-note prices (ZNM17 -0.16%) are down -8 ticks.

The Bank of Japan (BOJ) kept its benchmark policy rate unchanged at -0.1% as expected, and said that Japan's economy was on a "moderate recovery trend." BOJ Governor Kuroda said the momentum for getting to its 2% price target is not strong enough and the BOJ will continue increasing the monetary base until that target is reached.

The People's Bank of China (PBOC) raised interest rates on its open market operations and hiked the 7, 14 and 28-day reverse-repurchase agreements by 10 bp and said that higher open market operations don't mean benchmark interest rates are increasing. The PBOC added that market participants already had relatively strong expectations on higher open market operation rates based on China's economy rebound and Fed rate hikes.

U.S. STOCK PREVIEW

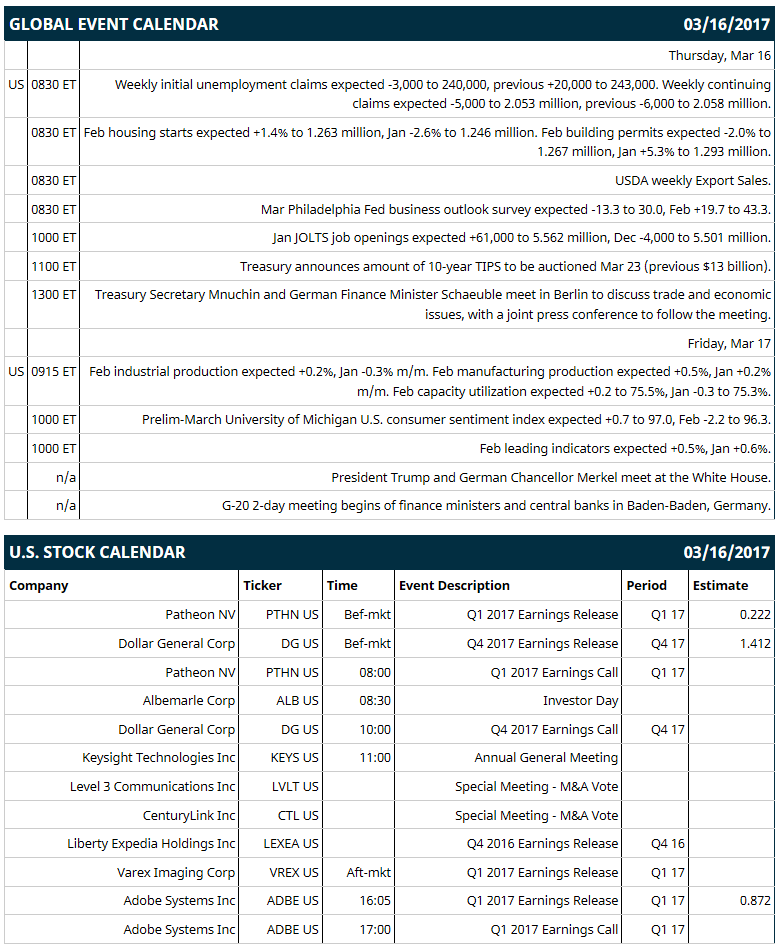

Key U.S. news today includes: (1) weekly initial unemployment claims (expected -3,000 to 240,000, previous +20,000 to 243,000) and continuing claims (expected -5,000 to 2.053 million, previous -6,000 to 2.058 million), (2) Feb housing starts (expected +1.4% to 1.263 million, Jan -2.6% to 1.246 million), (3) Mar Philadelphia Fed business outlook index (expected -13.3 to 30.0, Feb +19.7 to 43.3), (4) Jan JOLTS job openings (expected +61,000 to 5.562 million, Dec -4,000 to 5.501 million), (5) USDA weekly Export Sales.

Notable Russell 1000 earnings reports today include: Adobe (consensus $0.87), Dollar General (1.41), Patheon (0.22).

U.S. IPO's scheduled to price today: MuleSoft (MULE), ProPetro Holding Corp (PUMP).

Equity conferences: Barclays Global Health Care Conference on Tue-Thu, Gabelli & Co. Waste & Environmental Services Symposium on Thu, American College of Cardiology Meeting on Fri.

OVERNIGHT U.S. STOCK MOVERS

Jabil Circuit (JBL +1.05%) was upgraded to 'Buy' from 'Hold' at Needham & Co with a 12-month target price of $30.

Oracle (ORCL +0.61%) rose over 2% in after-hours trading after it reported Q3 adjusted EPS of 69 cents, better than consensus of 62 cents.

Zoetis (ZTS +1.61%) was rated a new 'Buy' at Craig Hallum with a 12-month target price of $65.

Guess? (GES +1.07%) tumbled 12% in after-hours trading after it reported Q4 adjusted EPS of 41 cents, weaker than consensus of 44 cents, and said it sees full year EPS of 28 cents-40 cents, well below consensus of 64 cents.

Williams-Sonoma (WSM +1.26%) gained almost 2% in after-hours trading after it reported Q4 adjusted EPS of $1.55, better than consensus of $1.51.

Engaged Capital said it increased its stake in Rent-A-Center (RCII +2.29%) to 13.7% from 9.9%.

GoPro (GPRO +1.52%) rallied 7% in after-hours trading after it said it cut an additional 270 jobs as part of its restructuring plan and said it sees Q1 revenue at the upper end of a Feb 2 forecast of $190 million-$210 million.

Editas Medicine (EDIT -5.38%) lost nearly 2% in after-hours trading after it announced that it intends to offer 4 million shares of its common stock in an underwritten public offering.

Alarm.com Holdings (ALRM +1.12%) jumped 8% in after-hours trading after it forecast 2017 total revenue of $322 million-$325.5 million, above consensus of $300.6 million.

Penumbra (PEN +0.06%) dropped 4% in after-hours trading after it announced it launched an offering of 1.3 million shares of its common stock.

Global Blood Therapeutics (GBT +4.26%) rose nearly 3% in after-hours trading after it was rated new 'Overweight' at Cantor Fitzgerald with a price target of $61.

magicJack VocalTec Ltd (CALL +10.20%) gained 1% in after-hours trading after it said it was "exploring options" for the company.

Conatus Pharmaceuticals (CNAT +6.05%) dropped over 6% in after-hours trading after it reported a Q4 loss of -35 cents a share, wider than consensus of -32 cents.

Arotech (ARTX +3.80%) plunged 17% in after-hours trading after it said it sees 2017 adjusted EPS of 20 cents-24 cents, weaker than consensus of 28 cents.

MARKET COMMENTS

Jun E-mini S&Ps (ESM17 +0.25%) this morning are up +6.00 points (+0.25%) at a 2-week high. Wednesday's closes: S&P 500 +0.84%, Dow Jones +0.54%, Nasdaq +0.63%. The S&P 500 on Wednesday rallied to a 1-1/2 week high and closed higher on relief that the Fed did not signal a faster pace of tightening as they kept their projections for two more 25 bp rate hikes this year. There was also a rally in homebuilder stocks after the unexpected +6-point increase in the U.S. Mar NAHB housing market index to 71, stronger than expectations of unchanged at 65 and the highest in 11-3/4 years. Energy producer stocks rose after crude oil recovered by +2.39%.

Jun 10-year T-notes (ZNM17 -0.16%) this morning are down -8 ticks. Wednesday's closes: TYM7 +27.50, FVM7 +17.25. Jun 10-year T-notes Wednesday climbed to a 1-week high and closed higher on relief that the Fed did not tighten up its Fed dot projections for three rate hikes per year in 2017-2019 and the post-FOMC meeting statement that said the Fed expects inflation to stabilize around 2% in the medium-term.

The dollar index (DXY00 -0.14%) this morning is down -0.12 (-0.12%) at a 1-month low. EUR/USD (^EURUSD) is down -0.0006 (-0.06%) and USD/JPY (^USDJPY) is up +0.12 (+0.11%). Wednesday's closes: Dollar index -0.96 (-0.94%), EUR/USD +0.0130 (+1.23%), USD/JPY -1.37 (-1.19%). The dollar index on Wednesday fell to a 2-week low and closed lower on the failure of the Fed to tighten up its Fed dot projections as some market participants had expected. There was also strength in EUR/USD on reduced European political risks after the anti-EU Freedom party did poorly in Wednesday's Dutch election.

Apr WTI crude oil prices (CLJ17 +0.72%) this morning are up +32 cents (+0.65%) and Apr gasoline (RBJ17 +1.15%) is +0.0177 (+1.12%). Wednesday's closes: Apr crude +1.14 (+2.39%), Apr gasoline -0.0001 (-0.01%). Apr crude oil and gasoline on Wednesday settled mixed. Crude oil prices were boosted by the unexpected -237,000 bbl decline in EIA crude inventories versus expectations of +3.0 million bbl, and by the -3.06 million bbl drop in EIA gasoline stockpiles versus expectations of -2.0 million bbl. Crude oil prices were undercut by the +0.2% increase in U.S. crude production in the week of Mar 10 to 9.109 million bpd, a 13-month high.

(Click on image to enlarge)

Disclosure: None.