Morning Call For Thursday, Feb. 16

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 -0.16%) are down -0.17% and European stocks are down -0.40% as prices consolidate following seven consecutive days the S&P 500 has rallied and posted new record highs. A 2% decline in Nestle SA is dragging European stocks lower after its new CEO, Mark Schneider, said it will take years for the company to return to the growth rates targeted by his predecessors. Losses in the overall market were contained by strength in technology stocks with Cisco Systems up almost 2% in pre-market trading after it reported better-than-expected Q2 EPS. The strength in Cisco has boosted Europe's Ericsson AB which is up over 3%. Asian stocks settled mixed: Japan -0.47%, Hong Kong +0.47%, China +0.52%, Taiwan -0.29%, Australia +0.12%, Singapore +0.27%, South Korea +0.04%, India +0.52%.

The dollar index (DXY00 -0.49%) is down -0.43%. EUR/USD (^EURUSD) is up +0.32%. USD/JPY (^USDJPY) is down -0.47%.

Mar 10-year T-note prices (ZNH17 +0.21%) are up +8 ticks.

New York Fed President Dudley (voter) said the U.S. economy is going to grow a little above trend and inflation is going to move back toward the Fed's 2% objective and "we would expect to gradually remove further monetary policy accommodation and snug up interest rates a little further in the months ahead."

U.S. STOCK PREVIEW

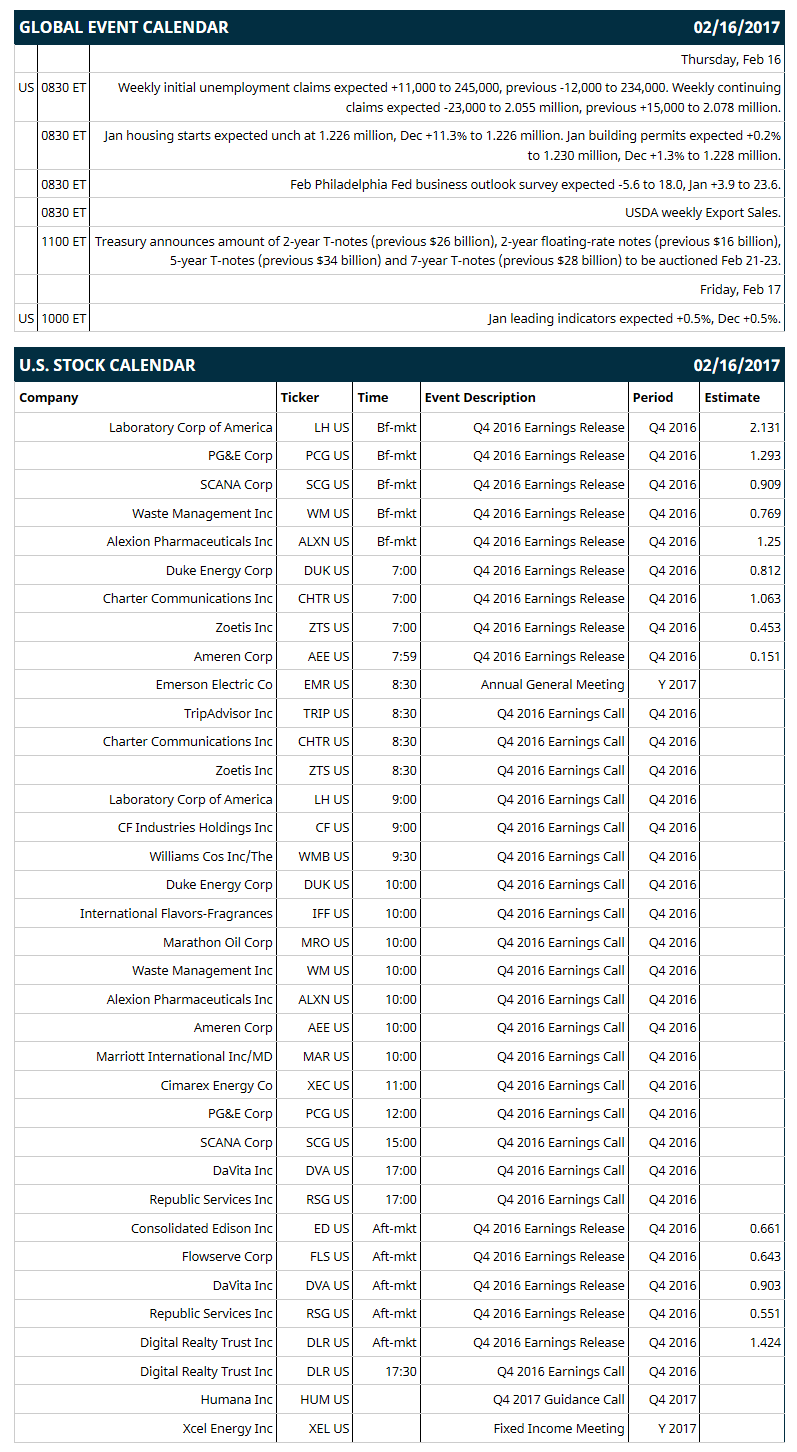

Key U.S. news today includes: (1) weekly initial unemployment claims (expected +11,000 to 245,000, previous -12,000 to 234,000) and continuing claims (expected -23,000 to 2.055 million, previous +15,000 to 2.078 million), (2) Jan housing starts (expected unch at 1.226 million, Dec +11.3% to 1.226 million), (3) Feb Philadelphia Fed business outlook survey (expected -5.6 to 18.0, Jan +3.9 to 23.6), (4) USDA weekly Export Sales.

Notable S&P 500 earnings reports today include: Duke Energy (consensus $0.81), PG&E (1.29), Lab Corp of America (2.13), Waste Management (0.77), Alexion Pharm (1.25), Charter Communications (1.07), Zoetis (0.45), Ameren (0.15), Consolidated Edison (0.66), Flowserve (0.64), DaVita (0.90), Republic Services (0.55), Digital Realty Trust (1.41).

U.S. IPO's scheduled to price today: none.

Equity conferences: RSA Security Conference on Mon-Thu, Goldman Sachs Technology and Internet Conference on Tue-Thu, Bank of America Merrill Lynch Insurance Conference on Wed-Thu, Leerink Partners Global Health Care Conference on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

GNC Holdings (GNC +1.46%) tumbled 9% in pre-market trading after it reported Q4 adjusted EPS of 7 cents, well below consensus of 36 cents.

Cisco Systems (CSCO +1.58%) gained almost 2% in after-hours trading after it reported Q2 adjusted EPS of 57 cents, better than consensus of 56 cents.

TripAdvisor (TRIP +0.98%) fell 5% in after-hours trading after it reported Q4 adjusted EPS of 16 cents, well below consensus of 31 cents.

NetApp (NTAP -1.49%) rallied 5% in after-hours trading after it reported Q3 adjusted EPS of 82 cents, higher than consensus of 74 cents, and said it sees Q4 adjusted EPS of 79 cents-84 cents, better than consensus of 77 cents.

Avis Budget Group (CAR +5.83%) dropped 6% in after-hours trading after it reported Q4 adjusted EPS of 15 cents, below consensus of 17 cents, and then said it sees full-year revenue of $8.8 billion-$8.95 billion, less than consensus of $9.01 billion.

Shutterfly (SFLY +2.19%) gained nearly 4% in after-hours trading when it was announced that it will replace Vascular Solutions in the S&P SmallCap 600 at the open of trade on Tuesday, Feb 21.

Progenics Pharmaceuticals (PGNX -0.52%) rose 5% in after-hours trading when it was announced that it will replace Calamos Asset Management in the S&P SmallCap 600 at the open of trade on Tuesday, Feb 21.

GoDaddy (GDDY +3.08%) declined 4% in after-hours trading after it reported an unexpected Q4 loss of -2 cents per share, weaker than consensus of 21 cents EPS.

CF Industries Holdings (CF -5.04%) fell 4% in after-hours trading after it reported Q4 net sales of $867 million, below consensus of $908.6 million.

Synopsys (SNPS +0.64%) climbed 6% in after-hours trading after it reported Q1 adjusted EPS of 94 cents, higher than consensus of 78 cents, and then said it sees 2017 adjusted EPS of $3.21 to $3.26, better than consensus of $3.20.

Omnicell (OMCL -0.26%) dropped over 8% in after-hours trading after it reported Q4 adjusted revenue of $174.6 million, weaker than consensus of $180.5 million.

TiVo (TIVO +0.53%) jumped 12% in after-hours trading after it reported Q4 revenue of $252.3 million, better than consensus of $227.5 million.

Chemours (CC +1.90%) slid 3% in after-hours trading after it reported Q4 adjusted EPS of 8 cents, including a $50 million tax allowance, weaker than consensus of 29 cents.

Molina Healthcare (MOH +0.84%) slumped 13% in after-hours trading after it reported Q4 revenue of $4.46 billion, below consensus of $4.56 billion, and said it sees 2017 adjusted EPS of $2.09, weaker than consensus of $3.69.

TransUnion (TRU -0.21%) lost over 1% in after-hours trading after it announced a secondary offering of 19.88 million shares of common stock.

NMI Holdings (NMIH +0.43%) rose 3% in after-hours trading after it reported Q4 EPS of $1.01, well above consensus of 13 cents.

Agnico Eagle Mines Ltd (AEM -0.06%) lost nearly 2% in after-hours trading after it reported Q3 adjusted EPS of 2 cents, well below consensus of 8 cents.

Cloud Peak Energy (CLD -4.07%) dropped 7% in after-hours trading after it said it sees 2017 adjusted Ebitda of $80 million to $120 million, less than consensus of $129.4 million.

SS&C Technologies Holdings (SSNC +0.52%) climbed 6% in after-hours trading after it reported Q4 adjusted EPS of 46 cents, better than consensus of 44 cents.

Martin Midstream Partners LP (MMLP -0.79%) slid nearly 3% in after-hours trading after it announced an underwritten public offering of 2.6 million common units (plus up to an additional 390,000 units pursuant to an option to be granted to the underwriters).

ConforMIS (CFMS -0.58%) plunged over 35% in after-hours trading after it said it sees 2017 total revenue of $80 million-$84 million, much lower than consensus of $100.9 million.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 -0.16%) this morning are down -4.00 points (-0.17%). Wednesday's closes: S&P 500 +0.50%, Dow Jones +0.52%, Nasdaq +0.59%. The S&P 500 on Wednesday rose to a fresh record high and closed higher on the strong U.S. Jan retail sales report of +0.4% and +0.8% ex autos (vs expectations of +0.1% and +0.4% ex autos) and the strong U.S. Feb Empire manufacturing index report of +12.2 to 18.7 (stronger than expectations of +0.5 to 7.0). Stocks were undercut by mounting prices pressures after U.S. Jan CPI ex food & Energy rose +0.3% m/m and +2.3% y/y, stronger than expectations of +0.2% m/m and +2.1% y/y.

Mar 10-year T-notes (ZNH17 +0.21%) this morning are up +8 ticks. Wednesday's closes: TYH7 -8.50, FVH7 -5.75. Mar 10-year T-notes on Wednesday fell to a 2-1/2 week low and closed lower on the stronger-than-expected U.S. Jan CPI, Jan retail sales, and Feb Empire manufacturing index reports, which bolstered the case for additional Fed rate hikes. There were also increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 2-week high. T-notes rebounded from their worst levels after the U.S. Feb NAHB housing market index unexpectedly declined.

The dollar index (DXY00 -0.49%) this morning is down -0.44 (-0.43%). EUR/USD (^EURUSD) is +0.0034 (+0.32%). USD/JPY (^USDJPY) is -0.54 (-0.47%). Wednesday's closes: Dollar index -0.07 (-0.07%), EUR/USD +0.0023 (+0.22%), USD/JPY -0.10 (-0.09%). The dollar index on Wednesday climbed to a 1-month high, but shed its gains and closed lower. The dollar was undercut by the weaker-than-expected U.S. Feb NAHB housing index report (-2 to 65, weaker than expectations of unchanged) and comments from Fed Chair Yellen suggesting she is no hurry to remove balance sheet accommodation when she said the Fed is committed to shrinking its balance sheet in a "gradual, orderly way." The dollar index was boosted by the stronger-than-expected U.S. Jan retail sales and Jan CPI reports, which bolster the case for the Fed to raise interest rates sooner rather than later.

Mar WTI crude oil prices (CLH17 +0.49%) this morning are up +33 cents (+0.62%) and Mar gasoline (RBH17 +0.21%) is +0.0057 (+0.37%). Wednesday's closes: Mar crude -0.09 (-0.17%), Mar gasoline +0.0021 (+0.14%). Mar crude oil and gasoline on Wednesday settled mixed. Crude oil prices were undercut by the +9.527 million bbl increase in EIA crude inventories to a record 518.1 million bbl, more than expectations for a +3.5 million bbl increase, and by the +2.846 million bbl increase in EIA gasoline supplies to a record 259 million bbl, higher than expectations of +500,000 bbl. Crude oil prices were supported by a weaker dollar and the -701,999 bbl decline in crude stockpiles at Cushing.

(Click on image to enlarge)

Disclosure: None.