Morning Call For September 9, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 -0.30%) are down -0.25% and European stocks are down -0.33% on concern that global central banks may have lost their desire for further stimulus measures after the ECB on Thursday refrained from expanding QE. European stocks were also under pressure on growth concerns in Germany, Europe's largest economy, after German Jul exports unexpectedly fell by the most in 11 months and Jul imports unexpectedly declined. Asian stocks settled mostly lower: Japan +0.04%, Hong Kong +0.75%, China -0.55%, Taiwan -1.06%, Australia -0.86%, Singapore -0.73%, South Korea -1.36%, India -0.85%. South Korea's Kospi Index fell closed down over 1% after North Korea conducted a nuclear test that South Korean President Park Geun Hye called an act of "maniacal recklessness."

The dollar index (DXY00 -0.04%) is up +0.02%. EUR/USD (^EURUSD) is up +0.03%. USD/JPY (^USDJPY) is up +0.19%.

Dec T-note prices (ZNZ16 -0.10%) are down -3 ticks.

The German Jul trade balance shrank to a surplus of +19.5 billion euros, narrower than expectations of +23.7 billion euros and the smallest surplus in 6 months. Jul exports unexpectedly fell -2.6% m/m, weaker than of +0.4% m/m and the biggest decline in 11 months. Jul imports unexpectedly fell -0.7%m/m, weaker than expectations of +0.5% m/m.

China Aug CPI rose +1.3% y/y, weaker than expectations of +1.7% y/y and the smallest pace of increase 10 months. Aug PPI fell -0.8% y/y, stronger than expectations of -0.9% y/y and the smallest pace of decline in 4-1/3 years.

U.S. STOCK PREVIEW

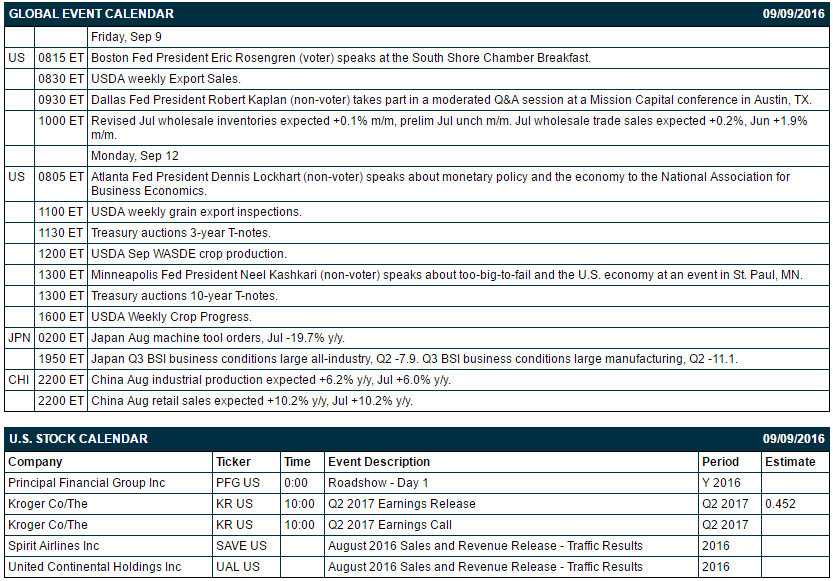

Key U.S. news today includes: (1) Boston Fed President Eric Rosengren (voter) speaks at the South Shore Chamber Breakfast, (2) Dallas Fed President Robert Kaplan (non-voter) takes part in a moderated Q&A session at a Mission Capital conference in Austin, TX, (3) revised Jul wholesale inventories (expected +0.1% m/m, prelim Jul unch m/m) and Jul wholesale trade sales (expected +0.2%, Jun +1.9% m/m), and (4) USDA weekly Export Sales.

Russell 1000 companies that report earnings today: Kroger (consensus $0.45).

U.S. IPO's scheduled to price today: none.

Equity conferences today include: none.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM +0.13%) was downgraded to 'Neutral' from 'Outperform' at Macquarie.

Advanced Micro Devices (AMD -9.06%) lost almost 2% in pre-market trading after pricing a public offering of $600 million worth of common stock.

Harley-Davidson (HOG -0.63%) was rated a new 'Outperform' at Bernstein with a 12-month target price of $64.

Chesapeake Energy (CHK +13.66%) was upgraded to 'Buy' from 'Hold' at Wunderlich Securities.

El Pollo Loco Holdings (LOCO -1.74%) climbed 6% in after-hours trading after it was announced that it will replace American Science & Engineering in the SmallCap 600 Index after the close of trading Monday, September 12.

Finisar (FNSR -1.78%) jumped over 12% in after-hours trading after it reported Q1 adjusted EPS of 38 cents, higher than consensus of 30 cents, and then said it sees Q2 adjusted EPS of 44 cents-50 cents, above consensus of 32 cents.

Oclaro (OCLR -1.30%) rose nearly 5% in after-hours trading after Finisar's Q2 EPS view was well above expectations.

Restoration Hardware Holdings (RH +1.18%) gained 13% in pre-market trading after it reported Q2 adjusted EPS of 44 cents, well above consensus of 29 cents.

Zumiez (ZUMZ unch) rallied 5% in after-hours trading after it reported a Q2 loss of -3 cents a share, better than consensus for an -8 cent loss, and said it sees Q3 sales of $209 million-$213 million, above consensus of $206.6 million.

Swift Transportation (SWFT +0.61%) jumped over 6% in after-hours trading after CEO Jerry Moyes said he will retire effective Dec 31 and current COO and President Richard Stocking will replace him as CEO.

Williams Cos. (WMB +2.67%) slid 3% in after-hours trading after Enterprise Products said it is withdrawing interest in a takeover of Williams. Enterprise Products (EPD +0.52%) rose nearly 2% in after-hours trading after the statement.

MGM Holdings (MGMB +2.94%) rose nearly 3% in after-hours trading after it said it still sees adjusted Ebitda margin of 30% this year, above the 25% from 2015.

Vince Holding (VNCE -3.28%) dropped over 7% in after-hours trading after it reported Q2 revenue of $60.7 million, below consensus of $64.1 million.

Xactly (XTLY +0.95%) fell over 3% in after-hours trading after it said it sees Q3 revenue of $23.3 million-$24.1 billion, at the low end of expectations of $24.0 million.

Lantheus Holdings (LNTH -0.94%) tumbled over 11% in after-hours trading after it announced a public offering of 5.2 million shares of common stock.

MARKET COMMENTS

Sep E-mini S&Ps (ESU16 -0.30%) this morning are down -5.50 points (-0.25%). Thursday's closes: S&P 500 -0.22%, Dow Jones -0.25%, Nasdaq-0.58%. The S&P 500 on Thursday closed lower on disappointment that the ECB did not expand stimulus measures at its policy meeting. Stocks recovered from their worst levels as energy producer stocks rallied after crude oil surged +4.66% to a 1-week high.

Dec 10-year T-notes (ZNZ16 -0.10%) this morning are down -3 ticks. Thursday's closes: TYZ6 -20.50, FVZ6 -11.50. Dec T-notes on Thursday closed lower on the unexpected drop in U.S. weekly jobless claims to a 7-week low and on disappointment that the ECB did not expand QE. There were also increased inflation expectations after the 10-year T-note breakeven inflation rate rose to a 2-1/2 month high.

The dollar index (DXY00 -0.04%) this morning is up +0.020 (+0.02%). EUR/USD (^EURUSD) is up +0.0003 (+0.03%). USD/JPY (^USDJPY) is up +0.19 (+0.19%). Thursday's closes: Dollar index +0.071 (+0.07%), EUR/USD +0.0021 (+0.19%), USD/JPY +0.75 (+0.74%). The dollar index on Thursday recovered from a 2-week low and closed higher on signs of U.S. labor market strength that may prompt the Fed to raise interest rates after U.S. weekly jobless claims unexpectedly fell to a 7-week low. Another hawkish factor for Fed policy was the increase in the 10-year inflation breakeven rate to a 2-1/2 month high due to the sharp +4.66% rally in oil prices. The dollar was undercut by the rally in EUR/USD to a 2-week high after the ECB refrained from addtional stimulus measures at its policy meeting.

Oct crude oil (CLV16 -1.24%) this morning is down -66 cents (-1.39%) and Oct gasoline (RBV16 -1.98%) is down -0.0324 (-2.29%). Thursday's closes: CLV6 +2.12 (+4.66%), RBV6 +0.0701 (+5.21%). Oct crude oil and gasoline on Thursday rallied to 1-week highs and closed sharply higher. Crude oil prices were boosted by the -14.51 million bbl plunge in EIA crude inventories to a 6-1/2 month low (the biggest decline since Jan 1999) and the -4.21million bbl decline in EIA gasoline stockpiles to an 8-1/4 month low, more than expectations of -750,000 bbl.

Disclosure: None.