Morning Call For September 7, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 -0.10%) are down -0.03% and European stocks are up +0.49% ahead of Thursday's ECB meeting. The odds of a Fed rate hike this year were further reduced after the U.S. Aug ISM non-manufacturing index fell to a 6-1/2 year low on Tuesday. The markets will look ahead to today's Fed Beige book to gauge the health of the U.S. economy. Gains in energy producers and mining stocks are supporting the market with crude oil up +1.23% and copper (HGZ16 +0.65%) up +0.84% at a 2-week high. Gains in European stocks were limited after German Jul industrial production unexpectedly fell by the most in nearly 2 years. Asian stocks settled mixed: Japan -0.41%, Hong Kong -0.19%, Chia +0.04%, Taiwan +0.84%, Australia +0.20%, Singapore -0.10%, South Korea -0.24%, India -0.18%. China's Shanghai Composite posted a 2-week high, although Japan's Nikkei Stock Index fell as exporter stocks weakened after USD/JPY slid to a 1-week low, which undercuts the earnings prospects of exporters.

The dollar index (DXY00 +0.01%) is up +0.02%. EUR/USD (^EURUSD) is down -0.07%. USD/JPY (^USDJPY) is down -0.42% at a 1-week low.

Dec T-note prices (ZNZ16 +0.05%) are up +0.5 of a tick on positive carryover from a rally in German bund prices to a 3-week high.

San Francisco Fed President Williams (non-voter) said if Fed officials wait too long to remove monetary accommodation, they "hazard allowing imbalances to grow, requiring us to play catch-up, and not leaving much room to maneuver."

German Jul industrial production unexpectedly fell -1.5% m/m, weaker than expectations of +0.1% m/m and the largest decline in 23 months.

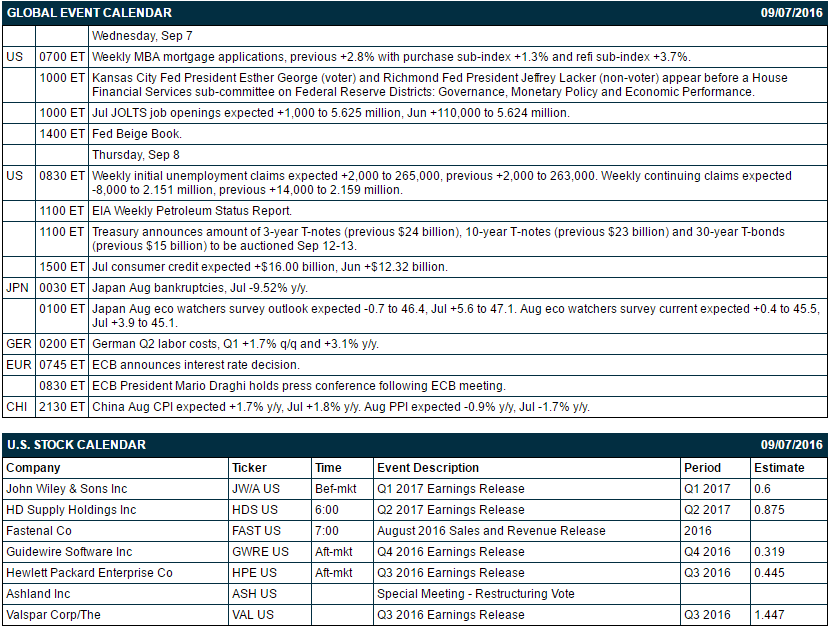

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +2.8% with purchase sub-index +1.3% and refi sub-index +3.7%), (2) Kansas City Fed President Esther George (voter) and Richmond Fed President Jeffrey Lacker (non-voter) appear before a House Financial Services sub-committee on “Federal Reserve Districts: Governance, Monetary Policy and Economic Performance,” (3) Jul JOLTS job openings (expected +1,000 to 5.625 million, Jun +110,000 to 5.624 million), and (4) Fed Beige Book.

Russell 1000 companies that report earnings today: HP Enterprise (consensus $0.45), John Wiley (0.60), HD Supply (0.88), Guidewire Software (0.32), Valspar (1.45).

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week include: Citi Global Technology Conference on Tue-Thu, Barclays CEO Energy Power Conference on Tue-Thu, Barclays Global Consumer Staples Conference on Tue-Thu, Barclays Back-to-School Conference on Tue-Thu, Cowen and Company Global Transportation Conference on Wed, Citi Biotech Conference on Wed, Avondale Partners Tech Services Conference on Wed, Goldman Sachs Global Retailing Conference on Wed-Thu, Drexel Hamilton Technology, Media and Telecom Conference on Wed-Thu, Keefe, Bruyette, & Woods Insurance Conference on Wed-Thu, Goldman Sachs Financial Technology Conference on Thu, Evercore ISI Real Estate Conference on Thu, Gabelli & Company Aircraft Supplier & Connectivity Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Royal Caribbean Cruises Ltd. (RCL -1.33%) was downgraded to 'Hold' from 'Buy' at Argus

Casey's General Stores (CASY +0.02%) dropped nearly 9% in after-hours trading after it reported Q1 EPS of $1.70, below consensus of $1.81.

Valeant Pharmaceuticals (VRX +2.47%) climbed 2% and Progenics (PGNX +3.36%) jumped nearly 4% in after-hours trading after the companies said the drug Relistor for treatment of opioid-induced constipation is now available for prescribing in the U.S.

Intersil (ISIL -2.23%) was downgraded to 'Hold' from 'Buy' at Stifel with a 12-month price target of $21.

Catalent (CTLT +0.16%) lost over 7% in after-hours trading after it announced a 19-million share secondary offering.

Advanced Micro Devices (AMD -2.26%) dropped 4% in after-hours trading after it filed to sell $600 million in stock and $450 million of convertible notes to repay debt.

Sigma Designs (SIGM +8.07%) gained 3% in after-hours trading after it reported Q2 adjusted EPS of 7 cents, well above consensus of 2 cents.

Ollie's Bargain Outlet Holdings (OLLI -0.98%) fell nearly 3% in after-hours trading after it started a secondary offering of 13.7 million shares.

HealthEquity (HQY +0.92%) rose nearly 3% in after-hours trading after it reported Q2 adjusted EPS of 16 cents, higher than consensus of 13 cents, and then raised its full-year revenue estimate to $174 million-$178 million from a prior view of $173 million-$177 million

Dave & Buster's Entertainment (PLAY -0.71%) slid 7% in after-hours trading after it cut its full-year comparable sales estimate to 2.25%-3.25% from a June 7 estimate of 3.25%-4.25%.

Momenta Pharmaceuticals (MNTA -0.57%) ws downgraded to 'Sell' from 'Hold' at Maxim Group.

Applied Optoelectronics (AAOI -0.57%) surged 23% in after-hours trading after it raised its Q3 revenue forecast to $63 million-$65 million from an Aug 5 estimate of $56 million-$59 million,

MARKET COMMENTS

Sep E-mini S&Ps (ESU16 -0.10%) this morning are down -0.75 of a point (-0.03%). Tuesday's closes: S&P 500 +0.30%, Dow Jones +0.25%, Nasdaq +0.31%. The S&P 500 on Tuesday rallied to a 1-week high and closed higher on increased M&A activity after Danaher bought Cepheid for about $4 billion and Enbridge agreed to buy Spectra Energy for $28 billion in stock. The -4.1 point decline in the Aug ISM non-manufacturing index to a 6-1/2 year low of 51.4 was a negative factor for the economy, although it also produced a delay in expectations for a Fed rate hike.

Dec 10-year T-notes (ZNZ16 +0.05%) this morning are up +0.5 of a tick. Tuesday's closes: TYZ6 +18.50, FVZ6 +11.50. Dec T-notes on Tuesday closed higher on positive carryover from a rally in German bunds to a 3-week high and on the decline in Aug ISM non-manufacturing index to a 6-1/2 years, which may further delay a Fed rate hike.

The dollar index (DXY00 +0.01%) this morning is up +0.020 (+0.02%). EUR/USD (^EURUSD) is down -0.0008 (-0.07%). USD/JPY (^USDJPY) is down-0.43 (-0.42%). Tuesday's closes: Dollar index -1.021 (-1.07%), EUR/USD +0.0108 (+0.97%), USD/JPY -1.41 (-1.36%). The dollar index on Tuesday fell to a 1-week low and closed lower on the weaker-than-expected Aug ISM non-manufacturing index, which bolsters the case for the Fed to delay raising interest rates. There was also strength in the yen against the dollar on speculation the BOJ may delay additional easing measures after an economic advisor to Prime Minister Abe said the BOJ should wait until after the Fed decides on interest rates before the BOJ acts.

Oct crude oil (CLV16 +0.80%) this morning is up +55 cents (+1.23%) and Oct gasoline (RBV16 +1.41%) is up +0.0225 (+1.71%). Tuesday's closes: CLV6 +0.39 (+0.88%), RBV6 +0.0148 (+1.14%). Oct crude oil and gasoline on Tuesday closed higher on the slide in the dollar index to a 1-week low and on comments from Iraqi Prime Minister Al-Abadi who said current oil prices aren't acceptable and he supports an oil-output freeze to increase prices. Oil prices were undercut by a lack of any concrete proposals from Russia or Saudi Arabia to stabilize oil prices after Russian Energy Minister Novak and Saudi Oil Minister Khalid Al-Falih on Monday pledged to cooperate to stabilize oil markets.

Disclosure: None.